<p>GabrielPevide/Getty Images</p>

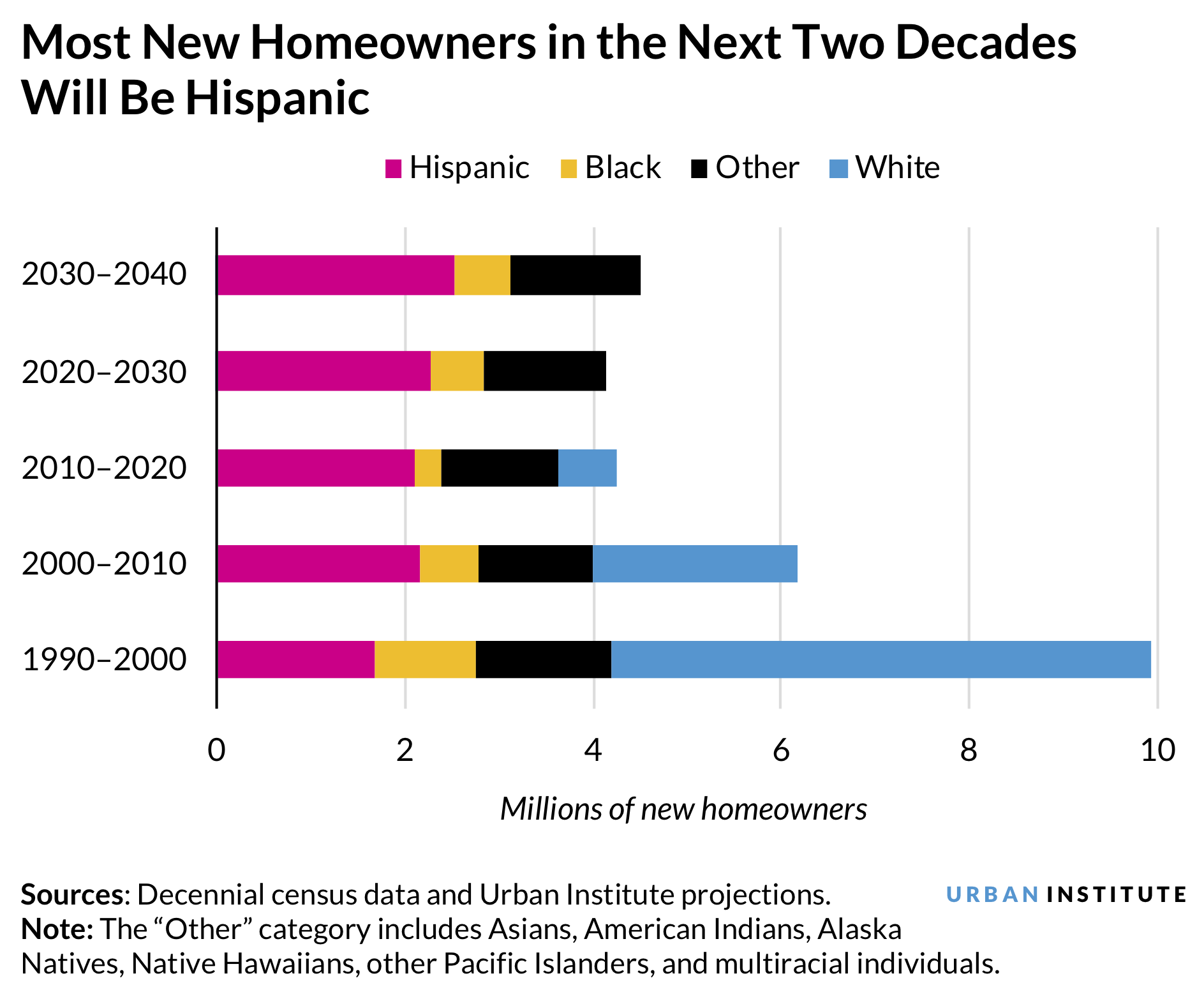

Hispanic households face substantial structural barriers to homeownership, including inequitable access to credit, down payments, and opportunities to build wealth. Despite this, our recent study projects that between 2020 and 2040, no net new homeowners will be white, and 70 percent of new homeowners will be Hispanic. To maintain a high level of homeownership, the mortgage and homebuilding ecosystem will need to evolve in a way that breaks down barriers and meets the needs of Hispanic homebuyers.

Young Hispanic households will account for the largest household growth

In 1990, just 7.3 percent of young households (headed by someone younger than 65) were Hispanic. By 2020, that had more than doubled to 16.4 percent. We project that this share will continue to increase in the next two decades, and that by 2040, more than 20 percent of young households will be Hispanic—triple the share in 1990.

The Hispanic household share will likely explode because the Hispanic population today is much younger than other racial and ethnic groups—meaning they are aging into the prime years for household formation.

The Hispanic population is the only racial or ethnic group that will experience an increased homeownership rate

We project that, with no change in policies, the overall homeownership rate will drop from 65 percent to 62 percent between 2020 and 2040, with the non-Hispanic white homeownership rate dropping from 73 percent to 71 percent, the Black homeownership rate dropping from 42 percent to 41 percent, and the homeownership rate for “other” households dropping from 58 percent to 57 percent. “Other” households are mostly Asian households but includes other groups, such as Pacific Islander households. These groups were combined into the “other” category because of a small sample size. The Hispanic community will see the only increase in the homeownership rate, from 49 percent to 51 percent.

Two facts explain the increase. First, Hispanic households are much younger than their Black and white counterparts; a much higher proportion are in their twenties, thirties, and forties, when households tend to buy their first home. Second, as discussed in our report, Hispanic households are the only group holding the homebuying ground. At any given age, Hispanic households are buying at rates similar to past generations.

These trends will significantly increase the number of Hispanic homeowners. Over the next two decades, we project that of the 8.7 million additional nonwhite homeowners, most (5.0 million) will be Hispanic families, 2.7 million will be Asian and other families, and 1.2 million will be Black families. The net number of white homeowners will decrease by 1.8 million.

How can the housing industry prepare for the wave of Hispanic homeowners?

Hispanic homebuyers are younger and have less income and wealth, lower credit scores, larger families, and more multigenerational families than the white homebuyers, necessitating changes in both the mortgage process and in the types of available housing.

In addition, we based these forecasts on prepandemic data, but the pandemic has made supporting Hispanic families—who have been harder hit by the pandemic than white families—even more urgent. Hispanic households have suffered disproportionate job and income loss and eroding savings, making it difficult to pay credit card and auto payments, and putting down payment requirements even further out of reach.

Three changes could reduce the barriers to homeownership for Hispanic households.

- Expand the use of down payment assistance. Hispanic homebuyers’ lower incomes, lower net worth, and lower parental wealth (and potential gifts or inheritance) makes affording a down payment challenging. But programs in every state offer assistance. There is also significant misinformation about the size of the down payment needed to buy a home. Accordingly, increasing the visibility of and opportunities for housing counseling and financial education about down payment assistance and the basic facts about down payments could support the growth in Hispanic homeownership.

- Expand access to mortgage credit. The COVID-19 pandemic has rolled back the progress made from 2013 to 2019 by Fannie Mae and Freddie Mac—and to some extent, the Federal Housing Administration—in expanding the credit box to include additional creditworthy borrowers. To truly capture the creditworthiness of future Hispanic borrowers, the housing industry must rethink how it qualifies borrowers for mortgages, update current credit scoring models, take into account additional data such as on-time rental payments, reexamine how it takes a borrower’s debt-to-income ratio into account, and more fully count the income of those who are self-employed or have gig-economy income. Given that Hispanic families are twice as likely to live in multigenerational households as families in the general population, underwriting should also account for supplemental income sources from family members who are not a party to the mortgage but contribute to the household income.

- Support an increased supply of affordable housing and allow for more multigenerational living at the local level. Greater access to mortgages and down payments will do little to alleviate the barriers to homeownership if the industry fails to address the low supply of affordable housing. Lack of affordable housing units is making housing more expensive for both renters and homeowners. To bring down the costs of housing production, including land costs, zoning and land-use regulations must be revised to increase density and promote more inclusionary zoning and land-use regulation; the permitting process must be expedited; and new cost-saving technologies must be embraced.

The industry needs to not only build more housing but build to fit the lifestyles of the coming wave of homeowners who are more likely to be a part of multigenerational families. Builders will likely experience considerable demand for multigenerational housing from both the nearly 5 million new Hispanic homebuyers and from the 2.7 million new Asian and other homeowners.

Our analysis shows steep increases in Hispanic homeownership over the coming decades, but these households face significant barriers—including putting together a down payment with less income, tight credit standards, and an affordable housing supply crisis. If federal, state, and local policymakers act now, they can significantly reduce these barriers and ensure continued robust growth in Hispanic homeownership.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.