<p>Photo by dszc/Getty Images.</p>

Access to mortgage credit remains overly tight in part because we are not measuring the credit risk of renters appropriately. For many renters, the most significant financial commitment is paying monthly rent, yet traditional credit scoring does not account for borrowers who meet their commitment month after month.

Missed rent payments are picked up by the credit bureaus, but on-time payments generally are not reported. Adding rental pay history, via bank statements, to the qualification process would make assessing renters’ credit risk easier and expand access to homeownership among a significant portion of the nation’s population.

To better understand how rental payment history might impact mortgage credit risk, we have analyzed how past mortgage payment history can predict future loan performance and have compared the monthly payments of renters and mortgage holders. Our analysis, which was encouraged and funded by the National Fair Housing Alliance, shows that rental payment history is highly likely to be predictive of mortgage loan performance.

Borrowers who miss no mortgage payments for two years rarely miss a payment for the next three years.

To look at the importance of mortgage payment history, we use Fannie Mae and Freddie Mac loan-level credit data from their credit risk transfer transactions. These data include the payment history of all fixed-rate, full-documentation, fully amortizing mortgages issued from 1999 through 2016, with the payment history through the third quarter (Q3) of 2017. To do this analysis, we first sort the loans by the payment history over two years from Q4 2012 to Q3 2014, tallying up the number of missed payments. We then look at the share of these mortgages that went 90 days delinquent over the subsequent three years, from Q4 2014 to Q3 2017.

As you can see in the table below, a loan that has been paid on time for 24 months has a 0.25 percent probability of going 90+ days delinquent in the subsequent three years. At one missed payment, the probability rises to 4.36 percent, at two it jumps to 28.2 percent, and at three it jumps again to 47.8 percent.

Renters are, on average, less affluent than homeowners, have lower credit scores and put down less toward the purchase of their first home. So, to ensure an apples-to-apples comparison, we sort our results by FICO scores and loan-to-value (LTV) categories.

For borrowers with FICO scores below 700, the probability that a loan with no missed payments ever goes 90+ days delinquent is 1.03 percent; for borrowers with scores above 750, it is 0.13 percent. The results are similar for LTVs: only 0.53 percent of loans with LTVs above 95 percent and no missed payments ever go seriously delinquent, and only 0.22 percent of loans with LTVs below 80 percent and no missed payments go seriously delinquent.

Thus, as a rule of thumb, borrowers who had no missed payments in the 24-month period performed extraordinarily well over the next three years, even if they had both low FICO and high LTV loans. For example, those who had FICO scores below 700 and an 80–95 LTV had a default rate of 1.14 percent. This is dramatically lower than similar borrowers with one missed payment (10.27 percent), two missed payments (34.83 percent), and three or more missed payments (60 percent).

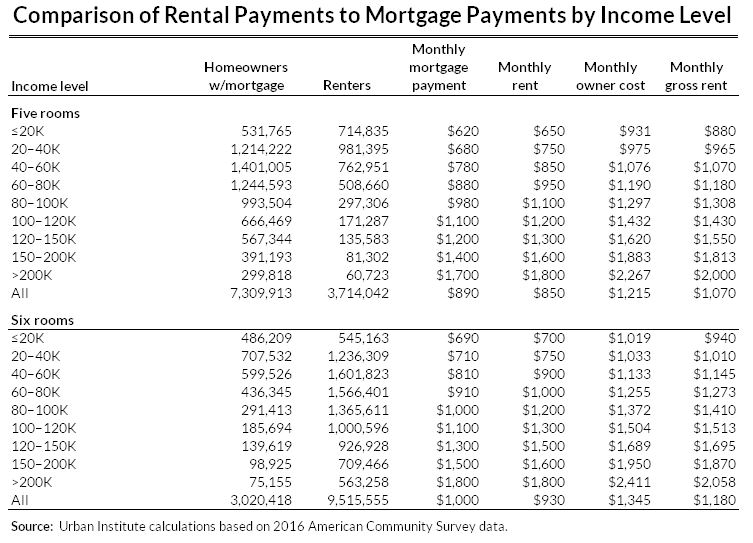

Renters and homeowners of similar income levels in similar homes have similar monthly housing expenses.

What can this analysis tell us about renters? To draw a comparison, we use the 2016 American Community Survey (ACS) and sort homeowners with mortgages and renters by different income categories. We restricted our sample to one-unit structures with either five rooms (roughly two to three bedrooms) or six rooms (roughly three to four bedrooms). Five- and six-room homes are the most common structures in this dataset.

The table below shows median rental payments versus mortgage payments and median total owner costs versus gross rent, by income buckets. For every income group, rental payments are lower than mortgage payments. However, the owners must pay for maintenance and repairs as well as utilities; some renters pay separately for utilities, others don’t. To put owners and renters on an equal footing, we also show monthly owner costs versus monthly gross rents.

As shown in the table above, for most income buckets these numbers are comparable, with exceptions in the under $20,000 and over $120,000 groups, where homeownership is generally more expensive.

Considering the comparability of monthly expenses paid by renters and homeowners and the predictability of future loan performance based on mortgage payment history, rental payment history is likely a strong predictor of mortgage default, and thus a powerful indication for credit risk purposes.

The evidence is clear that rental pay history should be included in assessing the creditworthiness of a renter attempting to qualify for a mortgage.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.