The Federal Housing Administration (FHA) has signaled that it may tighten credit to reduce future defaults on FHA-insured mortgages, noting with concern that the average debt-to-income (DTI) ratio for FHA-insured loans has been consistently increasing for six years.

But how important are DTI ratios in predicting a borrower’s ability to make on-time mortgage payments? Based on our analysis, the data show that DTI ratios are much less significant predictors of loan performance than FICO scores and that many high-DTI loans have strong FICO scores.

Based on this analysis, we believe that the FHA adequately assesses the importance of DTI ratios in its current process and shouldn’t place new restrictions on them, which could negatively affect two groups who need broader access to mortgage credit: millennials with student loan debt and communities of color, who generally have lower incomes.

The current DTI measure, referred to as the “back-end DTI,” totals all household debt payments, including auto, credit card, student loan, and mortgage debt, and compares it with income.

The FHA’s 2018 Annual Report to Congress (PDF) noted that the FHA is vigilantly monitoring persistent latent credit risks. In the report, the FHA notes that “the average borrower debt-to-income ratio continued to increase for the sixth straight year.... The share of FHA-insured mortgages with DTIs exceeding 50 percent increased again.”

Although those trends have abated slightly in fiscal year 2019 with declining interest rates, figures 1a and 1b below show that the average DTI ratio and the percentage of DTI ratios greater than 50 remains high.

Should the FHA be concerned about this increase in DTI ratios? To answer this question, we looked at the performance characteristics of loans with varying debt-to-income ratios. Figures 2a, 2b, and 2c below show the percentage of FHA loans that have experienced a serious delinquency, by months since origination.

We define serious delinquency as a loan that has been delinquent at least once for three or more months (i.e., D90+). Our dataset, the monthly Ginnie Mae loan level disclosure data, includes only loans that were still active in 2013, which distorts the results for earlier origination years. To accommodate this distortion, we looked only at purchase mortgages originated between the beginning of 2013 and July 2019.

Our analysis shows that higher-DTI loans do not always have higher serious delinquency rates.

For example, 5.6 percent of loans with DTI ratios ranging from 0 to 35 percent have been seriously delinquent at 60 months of age, compared with 7.6 percent of loans with DTI ratios of 35–45. But for loans with DTI ratios greater than 50, the D90+ rate at 60 months is 6.9 percent, lower than those with DTI ratios of 35–45.

The magnitude of the effect for DTI ratios is small, with a range of 5.6 to 7.6 percent for seriously delinquent loans, and the upper end is only about 1.4 times that of the lower end.

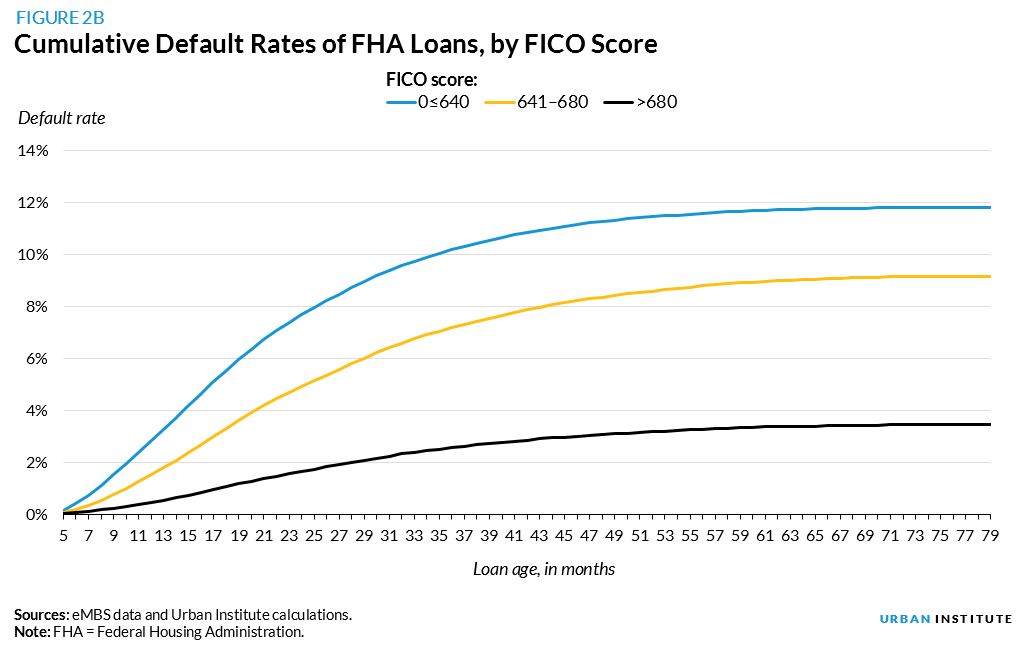

By contrast, loans with lower FICO scores—and loans with higher loan-to-value (LTV) ratios, for that matter—always have higher serious delinquency rates. The magnitude of impact on delinquency rates is much larger than on DTI ratios, ranging from 3.3 to 12 percent.

For FICO scores, the proportion of loans that was ever D90+ delinquent at 60 months ranged from 3.3 percent for loans with FICO scores greater than 780 to 12 percent for loans with FICO scores less than 620, or a factor of 3.5.

The LTV ratios of most FHA loans are high and in a narrow range. Even so, the LTV ratio effect is smaller than for FICO scores and about the same as that of DTI ratios.

At 60 months, serious delinquency rates range from 5.2 percent for loans with LTV ratios of less than 90 percent to 7.3 percent for loans with an LTV ratio of greater than 95 percent, or a factor of 1.4.

In addition, as shown in the table below, the high-DTI loans actually have a lower percentage of low-FICO loans, as one would expect from an underwriting system that takes into account compensating factors.

For example, for 2019 production with DTI ratios of 45 or greater, 51 percent of those loans have FICO scores of 660 or less. But for loans with DTI ratios greater than 45, only 45 percent of the loans have FICO scores of 660 or less.

Figure 3 shows how, at 60 months, high-DTI, high-FICO borrowers default at a much lower rate (5 percent) than low-DTI, low-FICO borrowers (11 percent). On the other hand, for low-FICO borrowers, both high-DTI borrowers and low-DTI borrowers have similar default rates after 60 months.

We used a simple ordinary least squares regression, capturing the default effects from different loan characteristics, to confirm these results. Our regression analysis shows that DTI ratio is a predictor of default, but it is a less important predictor than FICO score.

A small change in the DTI ratio (one standard deviation, or 9.1 percent) from the average (41.7 percent) would increase the likelihood of default by about 1.3 percentage points, all else being equal. But a small change in the FICO score (one standard deviation, or 47 points) from the average (680) would increase the likelihood of default by about 3.9 percentage points, triple the default effect from DTI ratio.

There is no question that higher-DTI loans, all else being constant, default at higher rates than low-DTI loans. However, even in the FHA market, the relationship is weak. FICO scores are much stronger predictors of default than DTI ratios.

Also, it appears that the current FHA scorecard adequately captures DTI ratios, requiring compensating factors for high-DTI ratios. If the FHA were to place further restrictions on DTI ratios, it would not benefit the FHA and would make obtaining mortgage credit more difficult for two important groups: millennials with student loan debt and communities of color, who generally have lower incomes.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.