<p>US Federal Reserve Bank Chairman Jerome Powell speaks at a press conference in Washington, DC, on December 11, 2019. The Federal Reserve kept its key lending rate unchanged on Wednesday but said it will turn its sights to low inflation and developments in the world economy. (Photo by ERIC BARADAT/AFP via Getty Images)</p>

In the wake of the 2007–09 Great Recession, it was hard for people with less-than-perfect credit to secure a mortgage. This stood in stark contrast to the years leading up to the financial crisis, when it was too easy to secure a mortgage. But in response to the Great Recession and the resulting restrictions and risks imposed through lawsuits and regulations, lenders became wary of lending to borrowers with anything less than pristine credit, and the mortgage credit box (or the availability of mortgages) contracted dramatically.

For the past six years, the government-sponsored enterprises (GSEs), Fannie Mae and Freddie Mac, and to some extent the Federal Housing Administration, have made small strides in expanding the credit box to additional creditworthy borrowers.

Then, the COVID-19 crisis hit. Not surprisingly, this public-health-turned-economic crisis is beginning to constrict the mortgage credit box again, threatening to return us to the 2010–13 period when only borrowers with nearly pristine credit could obtain a mortgage.

Because our data only go through March, they do not yet show tightening conditions on borrower characteristics (e.g., loan-to-value ratios, debt-to-income ratios, and credit scores). Most loans delivered into the GSEs were likely first submitted in late January or early February, before the pandemic’s effects were clear. But we do find notable trends in mortgage rates that likely reflect the early-stage response to COVID-19 by mortgage lenders. This is because the mortgage rate is not locked until the mortgage application is complete, so data on mortgage rates are more timely than data on borrower and loan characteristics.

We can examine evidence on mortgage rates from recently issued mortgage-backed securities and news about the market to determine how much access to credit is constricting in response to the COVID-19 crisis.

Evidence from mortgage rate data

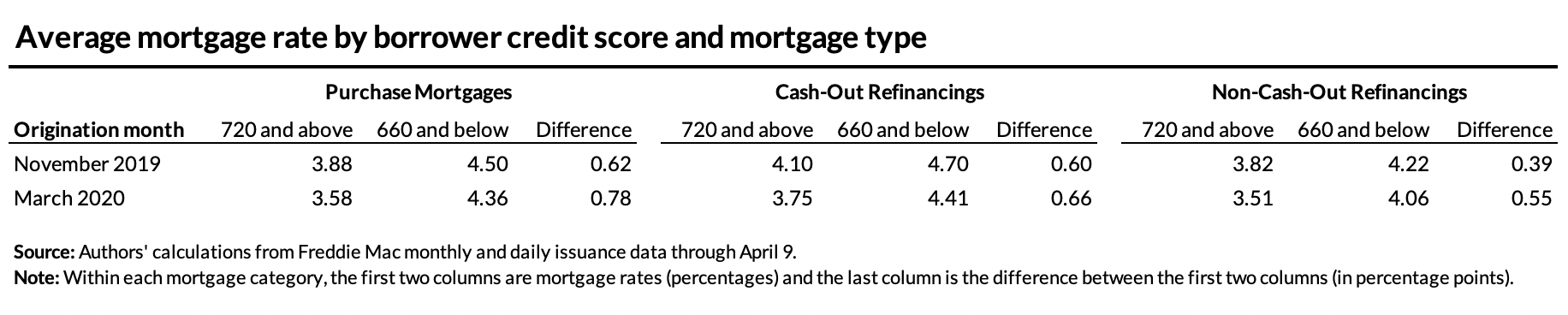

As of March 2020, people with high credit scores (720 and above) are locking in mortgage rates that are as much as 78 basis points lower than borrowers with low credit scores (660 or below). Particularly within the nonbank space, having a better credit score corresponds with a mortgage rate that is as much as 83 basis points lower than for a borrower with a weak credit score. These spreads between low and high credit scores are much wider than they were before the pandemic.

The table below shows that the most recent drop in mortgage rates benefited borrowers with high credit scores more than those with low credit scores. For purchase loans, borrowers with credit scores of 660 or below experienced a 14 basis-point drop between November and March, while borrowers with scores of 720 or above experienced a much bigger drop of 30 basis points. Thus, the differential between the two groups has expanded from 62 basis points to 78 basis points. This same pattern occurs in refinances as well, widening the rate differential between the two groups.

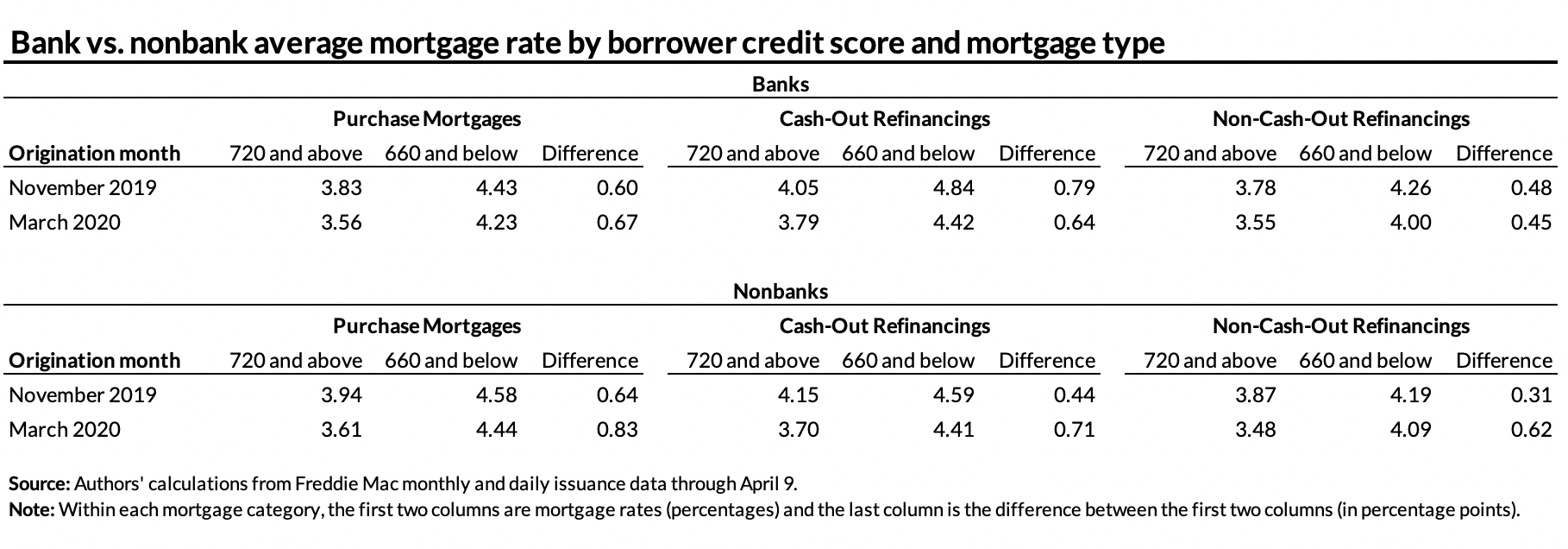

The table below shows how these same disparities between borrowers with low credit scores and high credit scores differ for bank and nonbank lenders. Nonbanks account for about half of outstanding agency mortgages (49 percent of agency mortgages and 52 percent of agency mortgage volume). For banks, the change in the rate differentials between borrowers with the lowest and highest credit scores are modest, and in the case of cash-out refinancing, the differentials are inverted. In contrast, for nonbanks, the spreads between borrowers with the lowest and highest credit scores has expanded dramatically. For example, the differential for purchase loans has increased from 64 to 83 basis points, and it has increased from 32 to 61 basis points for rate-term refinances.

Moreover, even though these rates were likely locked before the GSEs announced the widespread availability of forbearance for troubled borrowers and before the full extent of the COVID-related lockdowns were known, it was clear that delinquencies would be much higher because of the pandemic. Servicers need to advance the payments due to the investors in mortgage-backed securities, even if the borrower is delinquent. The advancing puts a larger burden on nonbanks than on banks, as banks have access to alternative funding sources.

Evidence from industry indexes and practices

We expect to see more credit tightening in the weeks ahead. The Mortgage Bankers Association Mortgage Credit Availability Index looks at underwriting guidelines, which is a leading indicator of mortgage production. The March reading indicates this index has tightened dramatically to its lowest levels since 2015. The tightening is more apparent for jumbo and nonqualified mortgage origination than for Federal Housing Administration or GSE loans. The more dramatic tightening in the non-agency space reflects the fact that even though the Federal Reserve has intervened to stabilize the agency mortgage-backed securities market, it is difficult to sell non-agency mortgages in the capital markets.

JPMorgan Chase has reportedly started requiring credit scores of at least 700 and minimum down payments of 20 percent for most home loan customers. Existing customers seeking to refinance and borrowers applying under the company’s affordable housing program, DreamMaker, are exempt from this requirement. Other lenders, including Wells Fargo, U.S. Bank, and Flagstar Bank, have also tightened their requirements, albeit in a less public manner.

Finally, many nonbank originators have felt pressure to tighten their credit box because the recently enacted rules instituting mortgage forbearance for borrowers failed to address the financial burden this places on servicers. When a homeowner misses a payment, mortgage servicers cover these payments by advancing the payments on that loan to investors. Nonbank servicers are less able to fund these advances because they do not have deposits available to tide them over, access to the Federal Reserve discount window, or access to Federal Home Loan Bank System advances. As a result, many nonbank originators have tightened their credit box to minimize the likelihood that a new loan would require forbearance.

This tightening in nonbank lending has been magnified because bank warehouse lines of credit have tightened the loan characteristics they will accept as collateral on loans to nonbank counterparties. This tightening has affected loans bound for one of the federal agencies and has been even more pronounced in the non-agency market. Warehouse lenders offer lines of credit to nonbanks and earn a return when the loan originated by the nonbank is sold to an investor. As investor appetite has receded, particularly for non-agency mortgage-backed securities (those not purchased by the Federal Reserve), warehouse lenders are raising the credit standards required for those loans, affecting nonbanks’ level of credit availability.

Both the data and the information we are hearing from the industry indicate that it will be increasingly difficult for people with less-than-pristine credit to secure a mortgage in the months ahead. Given the important role that homeownership plays in building wealth, we should avoid increasing the barriers to homeownership for those who otherwise have the ability to buy a home during this period.

The quickest and most effective action the federal government could take to keep credit accessible is to establish a liquidity facility for mortgage servicing advances. In addition, allowing financing for AAA non-agency securities via the Term Asset-Backed Securities Loan Facility would be important to reopening the non-agency market. These two actions would go a long way toward supporting the mortgage and broader housing market during this crisis.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.