Despite improvements in recent years, Hispanic homeownership still significantly lags behind non-Hispanic white homeownership. Homeownership is key for building wealth, and consequently, the homeownership gap between white and Hispanic households has serious implications for the total wealth gap between those groups.

Similar to our prior work mapping the black homeownership gap, we examined the 100 US cities with the largest number of Hispanic households and created a map to show the size of the Hispanic homeownership gap and the scope of the affected population across selected US metropolitan areas.

Each dot on the map represents the size of the Hispanic population in that metropolitan statistical area, and the dot’s color represents the magnitude of the Hispanic-white homeownership gap.

The gap is largest in the Northeast and smallest in the Southwest

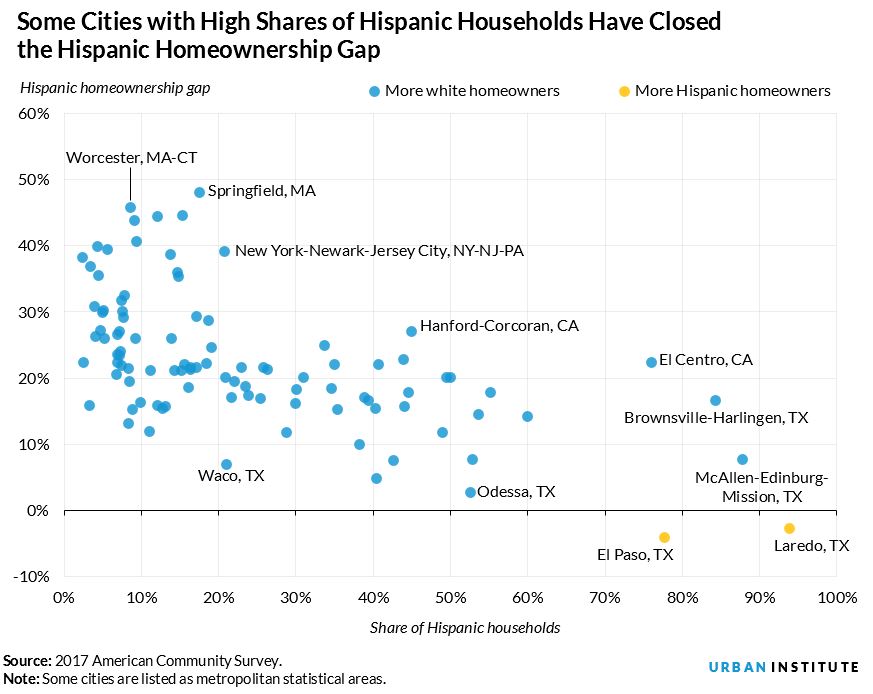

Our analysis shows that as the Hispanic share of a metropolitan area’s population grows, the size of the homeownership gap tends to decline.

Of the 10 cities with the largest number of Hispanic households, 7 of them— Dallas, Houston, Los Angeles, Phoenix, Riverside, San Antonio, and San Diego—are in the Southwest. The Southwest in general is home to a substantial share of the US Hispanic population. Accordingly, we find that the gap is generally smaller for cities in the Southwest, and the gap is even smaller in many Texas cities.

On the other hand, many Northeastern cities have smaller—though not insubstantial—Hispanic populations. Even Northeastern cities with the largest Hispanic populations have comparatively lower Hispanic shares of their population.

For example, New York City has the second-highest number of Hispanic households—almost 1.5 million—but they represent only 21 percent of total households. The Hispanic homeownership gap is notably larger in the Northeast than in other regions of the country.

The chart below demonstrates this relationship between the size of the gap and the Hispanic share of the population and highlights some of the cities with the smallest gaps.

Only two cities have closed the gap: El Paso and Laredo, Texas

Of the 100 cities we analyzed, 2 have reversed the gap and have a higher rate of Hispanic homeownership today than non-Hispanic white homeownership: El Paso and Laredo, Texas. El Paso’s Hispanic homeownership rate (63.9 percent) is 4.1 percentage points higher than its white homeownership rate, and Laredo’s Hispanic homeownership rate (61.5 percent) is 2.8 percentage points higher than its white homeownership rate.

Both El Paso and Laredo are majority-minority cities: 77.7 percent of El Paso’s households and 93.9 percent of Laredo’s households are Hispanic. Notably, they are also both situated on the US-Mexico border and, as such, are communities with sizeable immigrant populations. In each city, roughly a quarter of the population is foreign-born.

El Paso and Laredo’s border locations have been beneficial to the local economy: trade with Mexico is a significant contributor to economic and job activity in both cities. The housing markets are also strong.

We suspect that one partial explanation for the shrinking homeownership gap in the Southwest is the availability of affordable housing, particularly when compared with the lack of affordable housing in the Northeast. In fact, earlier this year, El Paso was recognized as one of the most affordable housing markets in the US.

What does the future look like for Hispanic homeowners?

Over the next 25 years, the Hispanic population will make up more than half of all net new households in the United States. Hispanic Americans will drive future housing demand and, by extension, general economic growth in this country.

Most of the US Hispanic population is younger than 35, and Hispanic millennials represent over a quarter of the cohort about to reach homebuying age.

In our barriers to homeownership brief, we estimate millennial homeownership potential by race and find that more than 21 million mortgage-ready millennials in 31 large metropolitan areas around the country have the credit scores, debt-to-income ratios, and credit history that suggest they could qualify for a mortgage. Of these mortgage-ready millennials, 4.6 million are Hispanic.

How can we boost Hispanic homeownership?

Although the Hispanic homeownership rate has increased steadily over the past five years, considerable barriers remain to achieving equitable access to credit, down payments, and opportunities to build wealth.

Policymakers and participants in the housing arena can support Hispanic homeownership through outreach efforts. These efforts should focus on sharing information about how to qualify for a mortgage, the importance of having credit history and a strong credit profile, and the availability of low–down payment products, as well as down payment assistance programs in all 50 states.

Mortgage financing also does not adequately serve Hispanic borrowers. Hispanic people on average use more cash than credit when making purchases. A lack of credit history precludes those who might otherwise be mortgage-ready from qualifying for a loan.

Thus, reforms in mortgage finance that address creditworthiness determination—such as greater use of rental payments, telecommunication bills, and utilities in credit assessments—can help expand homeownership to Hispanic borrowers and reduce the racial homeownership gap.

Hispanic borrowers also often have multiple family members contributing to monthly expenses, but typical underwriting rules only consider the income of those named on the mortgage. Giving greater weight to the income of those living in the home who are not on the mortgage would be helpful.

Cultural shifts are happening, and policymakers should act to ensure equitable growth in the housing market and the larger economy. Given the progress made in El Paso and Laredo, and with other cities closing the Hispanic homeownership gap, it seems possible to significantly reduce the Hispanic-white homeownership gap nationwide in the coming years.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.