<p>Photo by ArchiViz via GettyImages.</p>

The racial homeownership gap has persisted in America for decades. The gap has grown since the Great Recession and has contributed to the racial wealth gap.

Studies have highlighted how a substantial disparity in the value of homes owned by black and white homeowners exacerbates the racial wealth gap. We recently confirmed and quantified this housing wealth gap using Panel Study of Income Dynamics (PSID) data. We identified three patterns of obtaining and sustaining homeownership that contribute to the housing wealth gap.

- Black homebuyers buy less expensive first homes with more debt than white homebuyers

- Black households buy homes later in life than white households and

- Black homeowners are less likely to sustain their homeownership than white homeowners

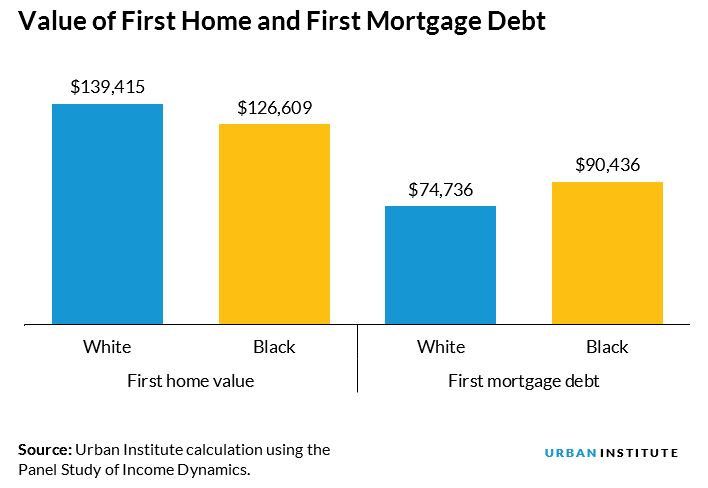

Black homebuyers purchase less expensive first homes using more debt

Using PSID data, we tracked the housing tenure choices since young adulthood of people who turned 60 or 61 between 2003 and 2015. The inflation-adjusted average housing wealth at age 60 or 61 for white households was $124,000, compared with $54,000 for black households, a 57 percent gap.

The average first home purchased by black homebuyers is valued at $127,000, compared with $139,000 for white homebuyers, yet black homebuyers, on average, have higher mortgage debt ($90,000) than white homebuyers ($75,000). Surprisingly and notably, the difference in mortgage debt ($15,000) is larger than the difference in the home value ($12,000).

The higher mortgage debt relative to the house value suggests that black households fall behind in their journey to building future wealth at the initial purchase. Higher mortgage debt not only lowers current and future wealth but could be a barrier to moving and realizing housing wealth gains.

Black households are more likely to buy homes later in life

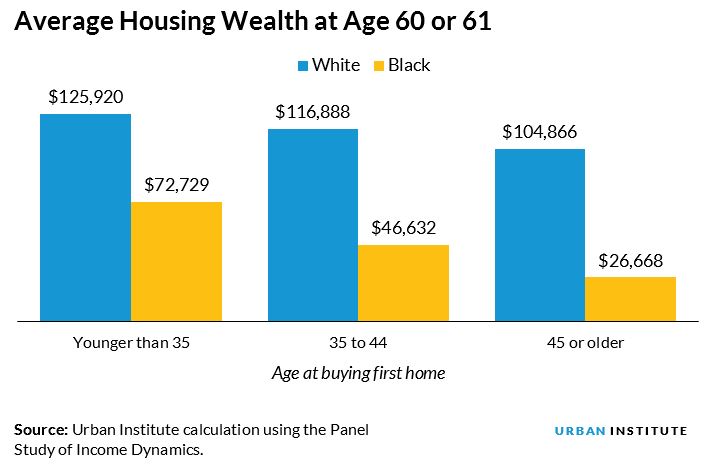

Our previous research makes it clear that buying a home at a younger age leads to greater wealth in retirement. Eighty-seven percent of white homeowners bought their first homes before age 35, compared with only 53 percent of black homeowners. Not only are black households less likely to buy their homes young, 18 percent of them never own a home before turning 60 or 61.

Delaying homeownership affects future housing wealth. For both black and white households, those who bought their homes before age 35 have the greatest return on housing at age 60 or 61. Because a greater proportion of black homebuyers buy their first homes later in life, their future housing wealth is stunted. But the black households who did buy their homes in the same age bucket as white households still have substantially lower housing wealth than white households at age 60 or 61. This suggests that the age of buying does not fully explain the black-white housing wealth gap.

Black homeowners are less likely to sustain their homeownership

Black households are less likely to remain homeowners after owning their first home. The number of black homeowners who transition to rental housing before turning 60 or 61 is substantially higher than white homeowners. For example, of the households who purchased their first home after age 44, 34 percent of black homeowner households switched to rental housing, while only 9 percent of white households did so. This suggests that black households are less likely to sustain their homeownership after first buying, which aggravates their future wealth-building potential.

We found that black households who sustained their homeownership had more than $23,500 higher housing wealth at ages 60 and 61 than black households who moved from owning to renting during their lives. Although this amount does not close the housing wealth gap, it suggests that another crucial factor in narrowing the wealth disparity is sustaining homeownership.

Implications and future research

It’s alarming to see the black homeownership rate fall to same level it was 50 years ago when the Fair Housing Act was first passed. As homeownership remains a key avenue for creating long-term wealth, especially for minorities, who, on average, have lower financial wealth (PDF), these trends will likely exacerbate future wealth inequality.

Evidence also shows that homeownership and wealth transfers from parents to children, indicating that racial housing wealth disparities will be passed on to future generations if not addressed promptly and effectively.

To narrow the racial homeownership and housing wealth gap, policy and system changes that focus on helping households gain access to sustainable homeownership earlier in life, and to maintain that ownership throughout life, are critical. These findings suggest that more research is needed to further understand all the contributors to the wealth gap between black and white households, including research into the different mortgage borrowing practices.

Previous research has also compared mortgage costs between black and white households and examined house price appreciation across black and white neighborhoods to understand the housing wealth gap. It would also be useful to investigate the factors that contribute to racial wealth and homeownership gaps across different cities. We will continue to explore this issue in our upcoming research projects.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.