<p>Photo by 10'000 Hours via GettyImages</p>

The sustained gap in homeownership between black and white Americans has been studied, quantified, and discussed thoroughly in recent years, particularly because the gap plays an enormous role in suppressing intergenerational wealth building and economic mobility. There is no debate about the gravity of the problem:

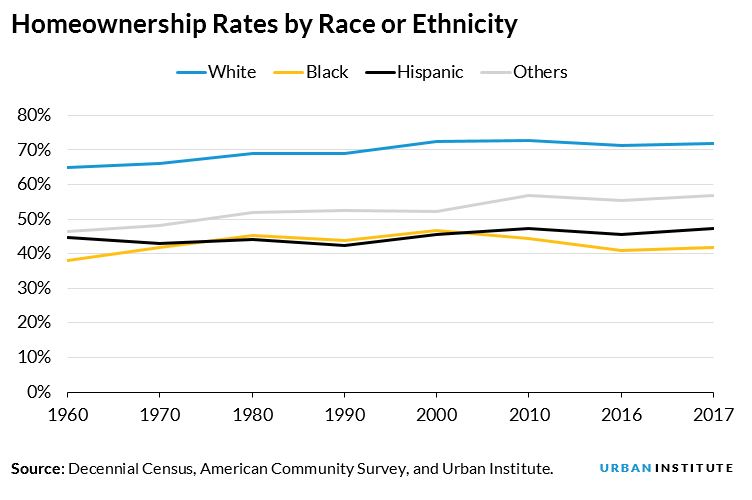

- Since 2001, the black homeownership rate has seen the most dramatic drop of any racial or ethnic group, declining 5 percent compared with a 1 percent decline for white families and with increases for Hispanic families.

- The homeownership rate of black millennials stands at 13 percent today compared with 37 percent for white millennials.

- In the past 15 years, black homeownership rates have declined to levels not seen since the 1960s, when private race-based discrimination was legal.

Historically, homeownership has been the best way to build wealth and remains, for most households, more financially beneficial than renting. Accordingly, the increasing and sustained loss of access to this major wealth-building tool makes it harder for black Americans to close the wealth gap.

Historically, homeownership has been the best way to build wealth and remains, for most households, more financially beneficial than renting. Accordingly, the increasing and sustained loss of access to this major wealth-building tool makes it harder for black Americans to close the wealth gap.

How do we translate what we know into what we do?

In other words, how can we reduce these gaps?

At the end of 2018, thanks to a generous planning grant from the National Association of Realtors and the National Association of Real Estate Brokers, we convened a group of diverse stakeholders to discuss how to move from evidence toward action. These housing industry leaders identified data and knowledge gaps and explored areas ripe for policy intervention at both the national and local level.

Five strategic priorities emerged from the discussion.

1. Understand forces at the local level.

Most metropolitan areas have seen declines in black homeownership in the past decade, with only 4 of the largest 31 metropolitan areas with more than 100,000 black households seeing a marginal increase in the black homeownership rate. We need to understand what is causing these declines and what is happening in the cities where black homeownership rates have increased.

We also need to explore specific market-based approaches, including removing local-level barriers related to affordability and help more renters get on a pathway to becoming homeowners. All communities don’t need the same interventions and a local approach to reducing the racial gaps will be required.

2. Address housing supply and finance challenges.

Following the Great Recession, housing supply dropped significantly, leading to an affordability crisis, especially at the lower end of the market. At the same time, an overcorrection to the crisis by regulators and lenders has made it harder to obtain a mortgage.

We need to understand how the housing shortage and tight credit affect people and communities of color. And we need to quantify how preservation, rehabilitation, and construction of affordable housing, as well as access to small-dollar mortgages, could improve the black homeownership rate in local markets.

3. Help more renters become homebuyers.

Any efforts to reduce renters’ barriers to homeownership should also increase black homeownership, such as analyzing how income is calculated in mortgage underwriting, stabilizing and broadening the reach of down payment assistance and low–down payment lending programs, and exploring how using rental payment history could support mortgage eligibility for millions of black households who are currently renting.

4. Strengthen government mortgage programs.

Two government mortgage insurance programs play an outsized role in supporting black homeownership: the Federal Housing Administration (FHA) and the US Department of Veterans Affairs.

While occupying just 12 percent of the overall mortgage market, the FHA finances 33 percent of purchase activity for first-time homebuyers and 34 percent of all minority purchase activity. Both programs are in need of several reforms and improvements, and we need to be vigilant about ensuring these programs remain viable and robust.

Similarly, housing programs supported by government-sponsored enterprises, Fannie Mae and Freddie Mac, and bank portfolio programs and local finance programs through community development financial institutions (CDFI) and housing finance agencies (HFA) can be better leveraged to do more for this segment of the population.

5. Sustain homeownership through all economic cycles.

Keeping people in their homes after purchase is the key to building housing wealth. We need to better understand how homeowners can use tools and programs to navigate all economic cycles, including taking a closer look at mortgage servicing and safe home equity lending products.

As the Urban Institute begins to raise bold questions in honor of our 50th anniversary, the Housing Finance Policy Center will focus on what it would take to change the trajectory and close the homeownership and wealth gaps for black Americans in the decades ahead.

Changing the course of such an enormous and entrenched problem will require intention, a renewed knowledge base, and the partnership of many stakeholders in the housing ecosystem. We’ll also need a plan. These five strategies are a starting point.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.