Photo by Monkey Business/Shutterstock.

Today’s young adults are less likely to own a home compared with baby boomers and Gen Xers at the same age. Our recent work has investigated why millennials have lower homeownership rates than prior generations, but the long-term consequences of homeownership delays are not well understood.

Our analysis starts the conversation about these consequences. We find that delaying homeownership may reduce the wealth that millennials generate over their lifetime.

Most of today’s older homeowners bought their first homes before age 35

Using the Panel Study of Income Dynamics (PSID), a dataset that has followed US individuals since 1968, we tracked people who reached age 60 between 2003 and 2015. The PSID switched to a biannual survey in 1997, so we used information at age 61 for those who were not surveyed at age 60.

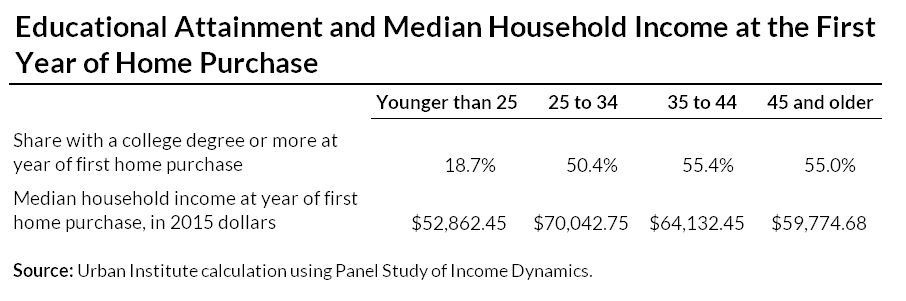

Today’s older adults became homeowners at a younger age than today’s young adults. Half the older adults in our sample (bought their first house when they were between 25 and 34 years old, and 27 percent bought their first home before age 25 (figure 1). But only 37 percent of household heads ages 25 to 34 and 13 percent of those ages 18 to 24 owned a home in 2016.

Those who bought earlier got the biggest bang for their housing buck

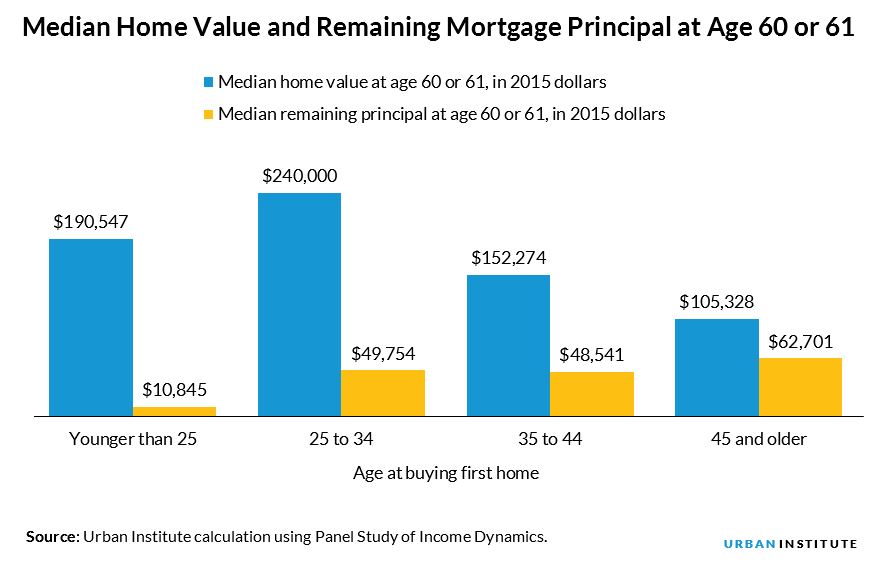

The impact of these earlier purchases is significant. Those who bought their first home between ages 25 and 34 have the greatest housing wealth by their sixties. At age 60 or 61, their median home equity (in 2015 inflation-adjusted dollars) is close to $150,000 (figure 2).

Those who bought their houses later have significantly lower housing wealth. Ten years of appreciation alone can make a big difference. There is a $72,000 difference in the median housing wealth of those who bought their first home between ages 25 and 34 and those who waited until they were 35 to 44. If they wait until they are 45 or older, the median wealth is more than $100,000 lower.

And while those who bought their houses before age 25 have a median home equity of $130,000, it’s important to understand why those who bought the earliest don’t end up with the most median home equity (table 1).

The youngest buyers have lower incomes, are less educated, and buy lower-priced homes. The median first-home value for these buyers is less than $70,000, while the median first-home value is around $125,000 for the other three groups.

But even though these younger homeowners ended up with less median equity, they have the largest return on their housing investment. The ratio between the median home equity at age 60 or 61 and median price of the first home decreases with the first age of homebuying: the ratio is highest for those who bought their first home before age 25 (1.93) and the lowest for those who bought their first homes after age 44 (0.36).

The bottom line is, those who bought houses before age 25 got the biggest bang for their housing buck.

Those who bought earlier live in more expensive houses and have less mortgage debt in their sixties

For those who bought their first homes when they were younger, greater home equity came from home price appreciation and paying down their mortgage debt. Those who bought their first home between ages 25 to 34 live in more expensive houses in their sixties than those who bought earlier or later. Their median house value at age 60 or 61 is $240,000.

Those who bought before 25 have lower median house value when they are older (as would be expected from their lower educational attainment) but have lower mortgage debt because they have owned their home longer. Their median remaining principal is less than $11,000, considerably lower than the other three groups.

Our analysis shows that those who bought their first home earlier are financially better off in their sixties. This suggests that deferring home purchases could have long-term economic consequences for millennials and the nation’s economic well-being.

As people age into retirement, they rely more heavily on their wealth rather than their income to support their lifestyles. Today’s young adults are failing to build housing wealth, the largest single source of wealth, at the same rate as previous generations.

While people make the choice to own or rent that suits them at a given point, maybe more young adults should take into account the long-term consequences of renting when homeownership is an option.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.