<p>Comfort Boateng sorts through two large boxes of mortgage and financial papers as she talks about her financial situation on August 18, 2014 in Bowie, Maryland. Fairwood is among one of the richest black neighborhoods in America, yet it was among the hardest hit from the financial crisis of 2008, and more than half of the people who bought homes there wound up in foreclosure. Photo by Michel du Cille/The Washington Post via Getty Images.</p>

Since 2001, the black homeownership rate has seen the most dramatic drop of any racial or ethnic group, declining 5 percent compared with a 1 percent decline for white families and increases for Hispanic and “other” families, which primarily include Asian Americans and Pacific Islanders (AAPIs).

The cohort of black Americans that has lost the most ground relative to other racial and ethnic groups is middle-aged homeowners ages 45 to 64. These homeowners, having lost their homes during the 2008 crisis, find themselves unable to move back into homeownership as they approach retirement age.

Married black households—traditionally the most likely to own homes—lost more ground than single-headed black households. These trends will affect retirement prospects for black Americans and their ability to pass wealth to the next generation.

From 2001 to 2016, white families had higher homeownership rates than other groups. In 2001, black and Hispanic families had similar homeownership rates (46 percent), but by 2016, black families had fallen behind (41 versus 46 percent). The homeownership rate for all groups rose from 2001 to 2006, but it rose less for black families than for other races and ethnicities. And although the homeownership rate fell for all groups from 2006 to 2016, it fell more for black families.

The homeownership rate for black families fell 5 percent. White families experienced a 1 percent drop, and Hispanic and “other” (primarily AAPI) families experienced increases. The 3 percent drop in the overall homeownership rate reflects changes in the composition of the general population.

In fact, black homeownership rates are now at levels similar to those before the passage of the Fair Housing Act in 1968, while rates are up for every other group.

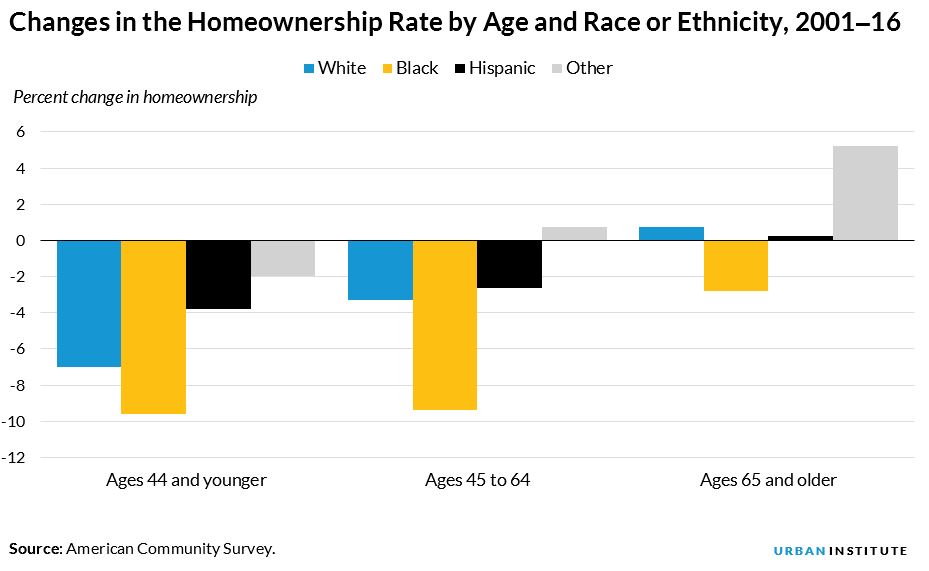

A striking drop in homeownership for middle-aged black household heads

For all races and ethnicities, the homeownership rate rises as the age of the household head increases, peaking between ages 65 and 74 before declining. We divided homeowners into three age groups:

- Ages 44 and younger = “younger” group

- Ages 45 to 64 = “middle-aged” group

- Ages 65 and older = “older” group

In 2016, the overall homeownership rate was 63 percent: 44 percent for the younger group, 72 percent for the middle-aged group, and 78 percent for the older group.

Black, white, and Hispanic families experienced drops in homeownership between 2001 and 2016 for the younger and middle-aged groups, with a more mixed picture for the older group.

But the most striking fact is how poorly middle-aged black households have performed relative to other races and ethnicities. Homeownership for black middle-aged families declined 9 percent, compared with 3 percent for white and Hispanic families.

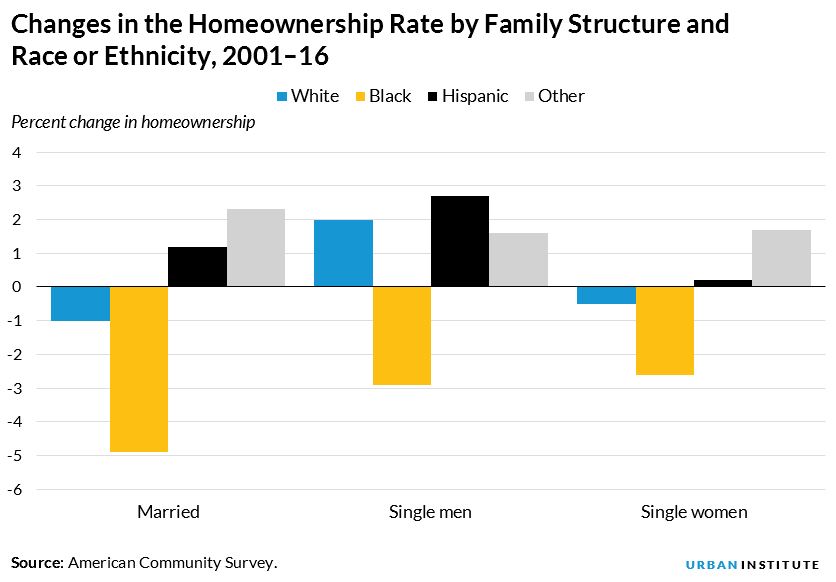

Married black couples experienced a sharp decline in homeownership

In general, married couples have higher homeownership rates than families headed by single homeowners (whether living alone or with others). In 2016, 78 percent of married households owned homes, compared with 48 percent of households headed by single men and 49 percent headed by single women.

Between 2001 and 2016, however, while black households lagged other races and ethnicities for all family structures, the fall in the homeownership rate for married black households was striking. The homeownership rate for married black households was down 5 percent compared with 3 percent for male- and female-headed single black households.

Married white households fell 1 percent in this period, while the rates for Hispanic and “other” married households increased.

Single black men fell further behind

While the declines in homeownership were similar between single male- and female-headed black households, single white and Hispanic men made larger gains in their homeownership rate than white and Hispanic women. Thus, the drop in the black single male homeownership rate contrasts with that of other races and ethnicities.

What can be done?

Homeownership has historically been the best way to build wealth and remains, for most households, more financially beneficial than renting. Reduced access to this wealth-building tool is a significant problem. Since the financial crisis, qualifying for a mortgage has become difficult for people with anything short of perfect credit, blocking as many as 6.3 million loans between 2009 and 2015 alone.

One of the most important steps to help stabilize and increase the black homeownership rate is to expand credit availability, particularly for Federal Housing Administration lending, which black families turn to for 45 percent of their purchase loans.

In addition, allowing greater use of alternative data in mortgage underwriting decisions, including use of rental payment history, and some utilities would benefit black homebuyers. And we need a more thoughtful approach to recognizing the realities of income variability and a greater focus on consumer education and housing counseling related to building credit and using low– and no–down payment and down payment assistance programs.

These and other actions to increase credit availability could allow creditworthy black and minority families to obtain a mortgage and access homeownership’s wealth-building benefits.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.