Photo by Gary Friedman/Los Angeles Times via Getty Images.

Housing finance debates have long raised these questions: What is the ideal US homeownership rate, and what should be the federal government’s role in encouraging homeownership? Offered answers have lacked detailed evidence on the costs of homeownership versus renting.

In a recent article in the Journal of Economic Perspectives, we show that homeownership remains highly beneficial for most families, offering both financial gains and a way to build wealth. Homeowning is especially beneficial for those who expect to own their home for a long enough period to overcome the sizable transactions costs and the cyclical volatility of home prices.

A full accounting of the costs of homeownership

Our analysis examines the costs of homeownership for borrowers who

-

purchased a home valued at $134,200 in 2002 (the national median home price, per Zillow),

-

used a 30-year fixed-rate mortgage with a 20 percent down payment (along with mortgage application costs),

-

remained in the home for varying amounts of time, and

-

refinanced once in 2012.

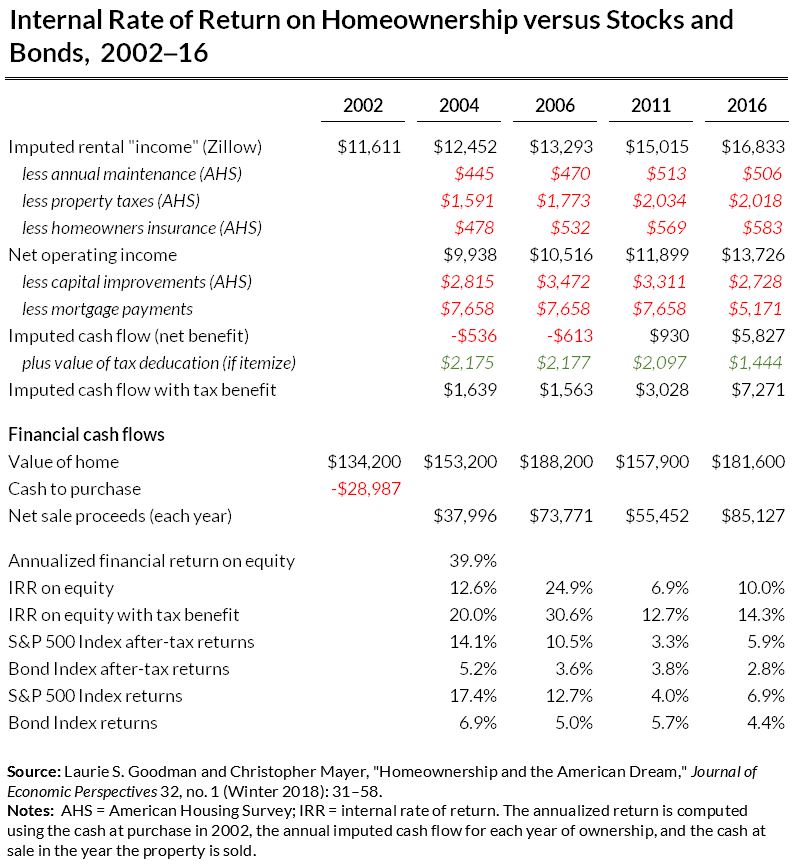

We begin by determining what a homeowner would have paid to rent a comparable property. From this amount, which the homeowner saves, we subtract all the costs of homeownership, including operating costs, maintenance costs, property taxes, homeowner’s insurance, capital expenditures, and annual mortgage, to get the property’s cash flow.

We then consider the tax deduction value for borrowers who itemize. Finally, to calculate the property’s internal rate of return, we consider the gain or loss from the sale of the home, the property’s cash flow each year, and 7 percent transactions costs from the sale.

The table above shows the results of this analysis for holding periods ranging from 2 to 14 years. We show the returns both with and without the tax benefit. For example, a homeowner who kept the home for 14 years, from 2002 to 2016, had an annualized return of 10 percent without the tax benefit and 14.3 percent with the tax benefit. There were individual years within this window in which renting would have been more advantageous, but homeownership was advantageous most of the time, as demonstrated by the high annualized rates of return.

Homeownership financially outperforms stocks and bonds

The returns for homeownership, not including the tax benefit, are higher than the after-tax returns on a bond index and on the S&P 500. If we consider the historical value of tax benefits, the returns to homeownership are higher than the alternatives. This is true, even for homes sold in 2011, near the low in home prices.

These trends have important tax implications. Approximately 40 percent of homeowners did not itemize under the old tax law, and fewer will itemize under the 2018 tax law. For itemizers, the benefits of homeownership will not disappear but will be smaller because of limitations on the ability to deduct state and local taxes and a lower limit on the mortgage interest deduction.

But homeowners continue to benefit from other federal tax subsidies, including the lack of tax paid on “imputed rent” (the return an owner gets by living in their own home that would be taxable if rent were paid to a landlord). Owner-occupants also pay little or no capital gains tax when their home appreciates in value.

The size of the benefit depends on where you live

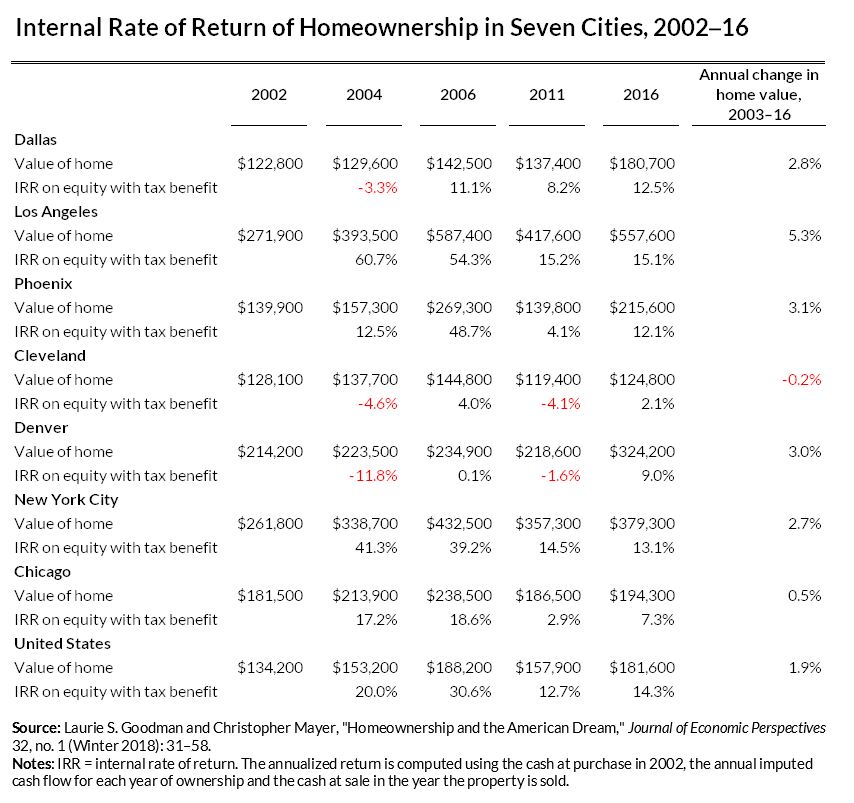

The financial benefits of homeownership are different across the seven metropolitan areas we examined: Chicago, Cleveland, Dallas, Denver, Los Angeles, New York City, and Phoenix.

Analysts often point to price appreciation to justify homeownership, but our study highlights the importance of comparing rents with home prices. In five of the seven markets (Dallas, Denver, Los Angeles, New York City, and Phoenix), home price appreciation was higher than the national average, but only in Los Angeles were the financial returns higher than the 14.3 percent return for the national average.

Rent savings from owning in Denver, Los Angeles, New York City, the highest cost markets, were low relative to the cost of the home (that is, purchasing a home was relatively expensive compared with the rent paid).

These results also suggest that the benefits from owning are higher in smaller cities and rural areas, where home prices are low. Of the seven markets, Cleveland was the only one where homeownership produced a lower rate of return than the S&P 500.

The returns on homeownership are not just financial, of course. Homeownership provides a stable place to live and an inflation hedge because mortgage costs are generally fixed while rents tend to rise with inflation.

Homeownership has traditionally been an important way to build wealth. The Survey of Consumer Finances shows that the average homeowner has household wealth of $231,420, while the average renter has household wealth of $5,200. But these numbers do not sort cause and effect, even though wealthier people buy homes and homeownership builds wealth. Many families lost their homes during the Great Recession, which had negative wealth effects. But numerous studies have shown that, on average, those who bought homes before the crisis built more wealth than similarly situated renters, even taking into account the wealth effects of those who could not sustain homeownership during the crisis.

Homeownership is not the universal panacea, but the financial returns on homeownership have been more beneficial than renting for most homeowners and will likely remain so if current patterns continue.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.