<p>Photo by MoMo Productions via GettyImages.</p>

Our recent report confirms that a higher percentage of young adults are living with their parents these days. In 2000, only 12 percent of people between the ages of 25 and 34 lived with their parents, but by 2017, that number had almost doubled to 22 percent. That’s 5.6 million more young adults still living with their parents.

This trend shows no signs of reversing, despite the economy continuing to improve. Is this a problem?

Young adults may enjoy perks living with their parents, but our research has established that those who lived with their parents between the ages of 25 and 34 were significantly less likely to be homeowners, or even household heads, 10 years later. Given the wealth-building benefits of homeownership, living longer with parents may hurt young adults’ long-term financial success.

Why are today’s young adults more likely to live under their parents’ roofs?

We found that young adults’ demographic and socioeconomic characteristics—mostly delayed marriage—and regional housing costs explain about 56 percent of the 10 percentage-point change in the share of those living with parents between 2000 and 2017. A significant increase in student debt and tight credit conditions may also contribute to this trend.

What are the potential consequences on homeownership of living with parents for longer?

We reasoned that if living with parents helps young adults save for a down payment, it could accelerate homeownership later in life. Saving for a down payment while staying with your parents might also facilitate the purchase of a more expensive home or allow a young adult to put more down, resulting in a smaller mortgage payment.

Using the Panel Study of Income Dynamics, we selected young adults who were between the ages of 25 and 34 between 1999 and 2005 and tracked their headship and homeownership status after 10 years (2009 to 2015). We compared three groups:

- those who lived with their parents from ages 25 to 34

- those who rented during those years

- those who owned their own homes during those ages

We found that living longer with parents influenced both headship and homeownership 10 years later; 32 percent of those who lived with their parents as young adults had still failed to launch 10 years later (68 percent had become household heads or spouses of household heads), compared with almost all the earlier renters and homeowners.

And of those who lived with their parents, only 37 percent of them owned their own homes 10 years later, compared with 48 percent and 84 percent of those who had rented and owned earlier, respectively.

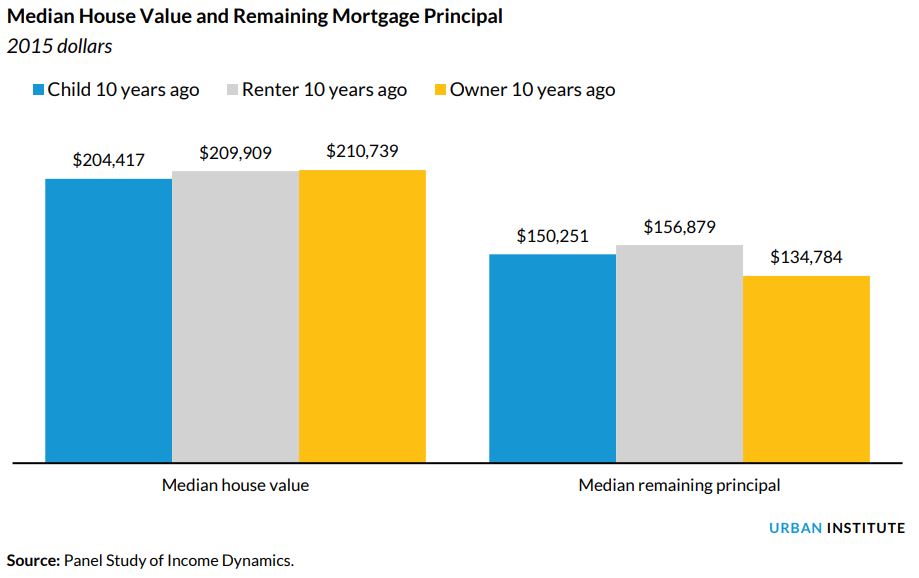

So maybe headship and homeownership are delayed for those who are slower to launch. But when these young adults do eventually buy a home, do they purchase a more expensive home or use a smaller mortgage, thanks to the savings they’ve amassed from living with their parents?

There is no evidence to suggest the former occurs. The median home value does not differ according to the living arrangement of young adults 10 years earlier. Median house values range between $200,000 and $210,000 for both groups.

Additionally, those who became homeowners earlier have the smallest remaining mortgage principal, reflecting the longer debt payback period.

Time spent living with parents can have a lifelong financial impact. Despite the Great Recession, housing is still one of the most important wealth-building tools in the US. Recent analysis also finds that buying a home earlier in life provides a greater investment return as retirement nears.

While long-term data will reveal the trends and consequences for millennials living with their parents, our study suggests it is beneficial for young adults to depart from their parents’ homes, sooner rather than later.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.