<p>(Alexphotographic / Getty Images)</p>

Accurately appraising a home’s value is an important factor in determining whether and how a potential buyer can receive mortgage financing. Estimating a home’s value has implications not only for the lender’s and borrower’s level of risk but also for establishing how much wealth, or equity, the family has in their home.

Traditionally, a property assessment is conducted by a certified appraiser as part of the mortgage process. The appraiser visits the home in person to appraise the condition of the property’s interior and exterior and, along with their evaluation of the current real estate market, including sales of comparable properties in the neighborhood, determines the property’s value.

But in-person appraisals are susceptible to racial discrimination and human bias. Disparities in home value appraisals would have important repercussions for both the racial homeownership gap and racial wealth gap, as low appraisals for Black families can further limit their ability to build wealth.

Automated valuation models (AVMs) are a type of financial technology that can be an alternative or supplement to in-person appraisals. Many lenders use AVMs as part of their lending decision process. AVMs apply mathematical algorithms to a database of housing activity, including sales transactions, to calculate a home’s value. Hypothetically, by limiting the human assessment element and potential racial bias, AVMs could provide a more accurate picture of a home’s value in majority-Black neighborhoods, which could hold promise for closing the racial wealth gap.

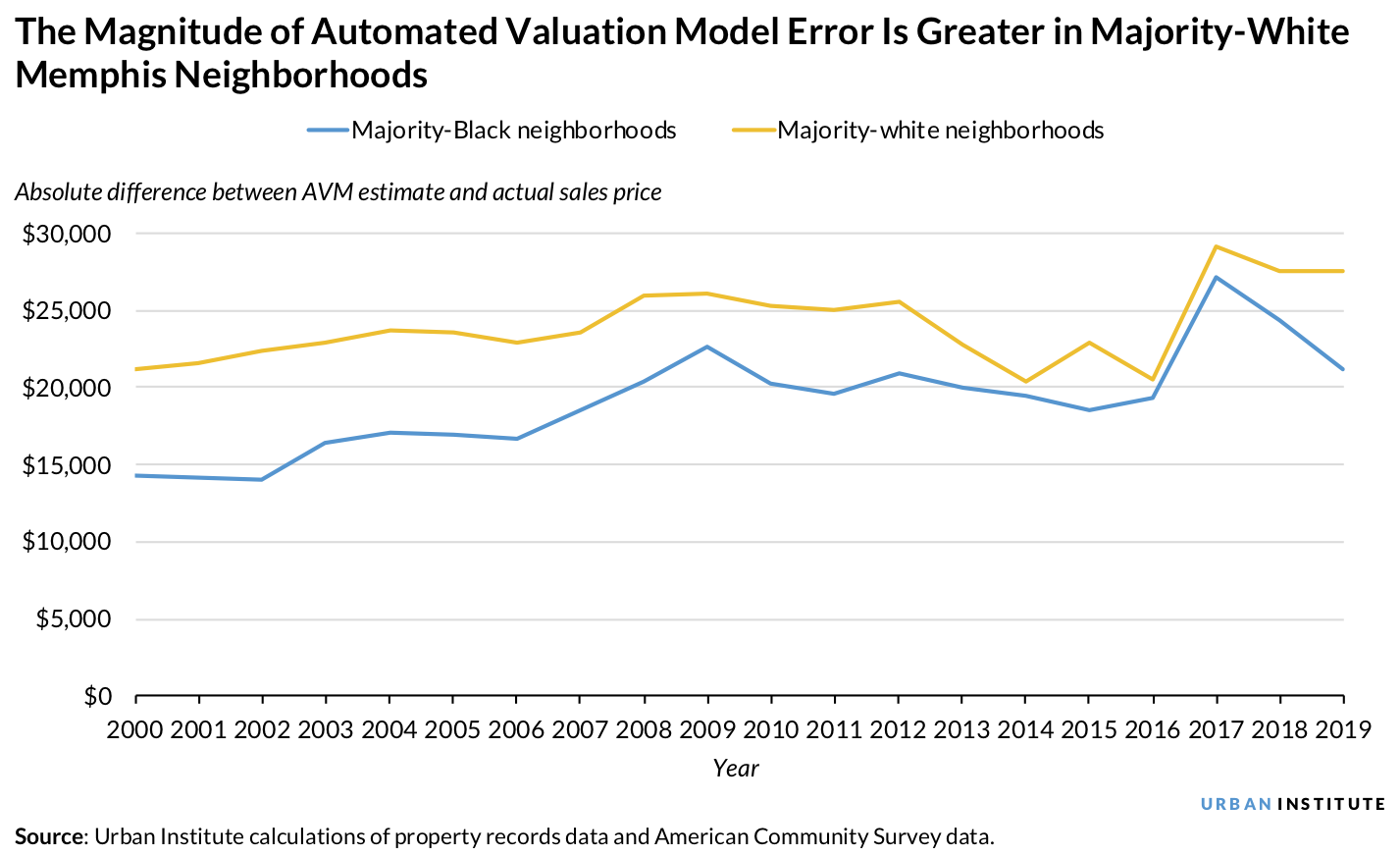

In our recent report, we examined data from Atlanta, Memphis, and Washington, DC, to determine how AVMs contribute to racial disparities in home value estimates. We studied the accuracy of AVMs in majority-Black neighborhoods relative to majority-white neighborhoods by comparing the AVM estimate with the actual sales price.

We found that even though the magnitude of the error (the absolute dollar difference) was larger in majority-white neighborhoods, the percentage magnitude of the error (the proportional difference for what that error meant) was larger in majority-Black neighborhoods after adjusting for lower sales prices in majority-Black neighborhoods.

Lower sales prices heighten the percentage magnitude of AVM error in majority-Black neighborhoods

Our findings in the Atlanta, Memphis, and Washington, DC, metropolitan statistical areas suggest that AVM-estimated home values in majority-Black neighborhoods did not exhibit systematic bias (by average dollar difference) over time. This post shows results for Memphis; results for Atlanta and Washington, DC, which also contributed to the interpretation of our findings, are available in the full report.

In fact, the magnitude of AVM error was larger in majority-white neighborhoods.

But, after adjusting for the sales price, which is lower in majority-Black neighborhoods, we found that the percentage magnitude of error was greater in majority-Black neighborhoods.

That means the absolute dollar-value error might be less in these neighborhoods, but the proportional size of the error is larger because the average home price in majority-Black neighborhoods is much lower. For example, the percentage difference between a $100,000 AVM estimate and a $115,000 sales price (15 percent) is higher than the percentage difference between a $400,000 AVM estimate and a $415,000 sales price (4 percent), even though the absolute difference ($15,000) is the same.

These findings highlight the racist roots underpinning the systematic undervaluation of homes in majority-Black neighborhoods. For example, zoning historically was used to steer industrial activity toward majority-Black neighborhoods, leading to disproportionate toxic exposure and depressed land values for Black residents. These lower land values continue to weigh on home prices and contribute to the gap between home values in majority-white neighborhoods and majority-Black neighborhoods.

To explain the greater percentage magnitude of error in majority-Black neighborhoods, we built a regression model controlling for home values and other key dimensions such as property differences, neighborhood conditions, and turnover rates. Even after these controls were added, the neighborhood’s majority race was still a statistically meaningful reason behind differences in the percentage magnitude of error, a result necessitating additional research because AVMs are unaware of the neighborhood’s majority race.

How modelers and policymakers can close this race-based gap and help Black families build wealth

Amid growing demand for financial technology solutions in response to the COVID-19 pandemic, AVM use is poised to increase. But our results suggest that a wider use of AVMs will not, on their own, eliminate (PDF) the racial homeownership or wealth gap. In fact, they could exacerbate the gap because of their disproportionate effect on majority-Black neighborhoods.

This is a systematic undervaluation issue: homes in majority-Black neighborhoods have a lower value than homes in majority-white neighborhoods partly due to systemic racism’s effects on housing. But AVM inaccuracy compounds the problem by providing proportionately less accurate estimates for homes in majority-Black neighborhoods. This inaccuracy could make neighborhood-wide disparities even worse when these homes are used as comparable sales in the transaction of another property.

The impact of percentage magnitude of AVM error has implications for Black wealth accumulation and the broader racial wealth gap. When an AVM underestimates a home’s value, it reduces the estimated amount of housing wealth the homeowner holds, which could also result in a canceled home sale. Conversely, an AVM-produced home value estimate that is too high could artificially boost home values, unnecessarily reduce housing affordability, and risk homeowner wealth if home values corrected.

To address the potential disparate impact of AVMs on majority-Black neighborhoods, modelers can expand the variables included in their AVMs to improve performance in lower-price majority-Black neighborhoods. This focus on identifying data sources to understand and address racial inequities is a key component of the administration’s executive order that aims to promote racial equity through federal initiatives.

More foundationally, federal, state, and local policymakers can implement policies that boost direct investment into majority-Black neighborhoods, which, in turn, can reduce neighborhood blight (PDF) and increase home values. Mission-based purchases of distressed homes, which are disproportionately located in majority-Black neighborhoods, can also allow homes to be resold to qualified low-income households seeking to achieve homeownership and help stabilize home values.

Steps to reduce AVM inaccuracy and support home values in majority-Black neighborhoods can help Black families achieve the full benefits of homeownership.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.