<p>Xochitl Menjivar / EyeEm / Getty Images</p>

For many families concerned about their economic security in the wake of the COVID-19 pandemic, refinancing an existing mortgage can lower expenses. To do so, an in-person home appraisal by a certified appraiser is typically required to assess the property’s value. The ratio of the mortgage amount (the amount being loaned) to the property value, or the loan-to-value (LTV) ratio, is an important measure of mortgage risk, as it shows the amount of equity the borrower has in the home.

But with the ongoing pandemic, in-person appraisals pose health risks. The inability to obtain in-person appraisals poses a challenge for families hoping for relief through refinancing or those taking advantage of historically low mortgage interest rates by purchasing a home.

To help these families, the Federal Housing Finance Agency (FHFA) announced in late March that the government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac must grant flexibility for appraisal verifications on loans they intend to purchase, including encouraging lenders to accept appraisal waivers when eligible. These waivers present little risk to the GSEs and encourages many homeowners to refinance or tap into their home equity to bolster their financial situation in an uncertain environment.

Appraisal waiver use has increased following the FHFA’s announcement, spurring an increase in refinance activity

An appraisal waiver allows a loan applicant to forgo the traditional method of appraising a home and to determine the home’s value through automated underwriting instead. Fannie Mae and Freddie Mac have traditionally offered appraisal waivers for low-LTV rate-term refinance mortgages, for a small number of purchase mortgages, and for cash-out refinances. Since the FHFA’s announcement, appraisal waivers have increased by 14 percent overall, and it has contributed to an increase in refinance activity.

|

GSE Mortgage Originations by Property Valuation Method |

||||||||

|

|

Overall |

Purchase |

Rate/Term |

Cashout |

||||

|

|

March |

August |

March |

August |

March |

August |

March |

August |

|

Appraisal |

76% |

62% |

95% |

90% |

50% |

37% |

86% |

74% |

|

Appraisal Waiver |

24% |

38% |

5% |

10% |

49% |

63% |

13% |

26% |

|

Other |

1% |

0% |

0% |

0% |

1% |

0% |

1% |

0% |

|

Other includes Onsite Property Collection, GSE-targeted Refinances and loans where the method is unavailable |

||||||||

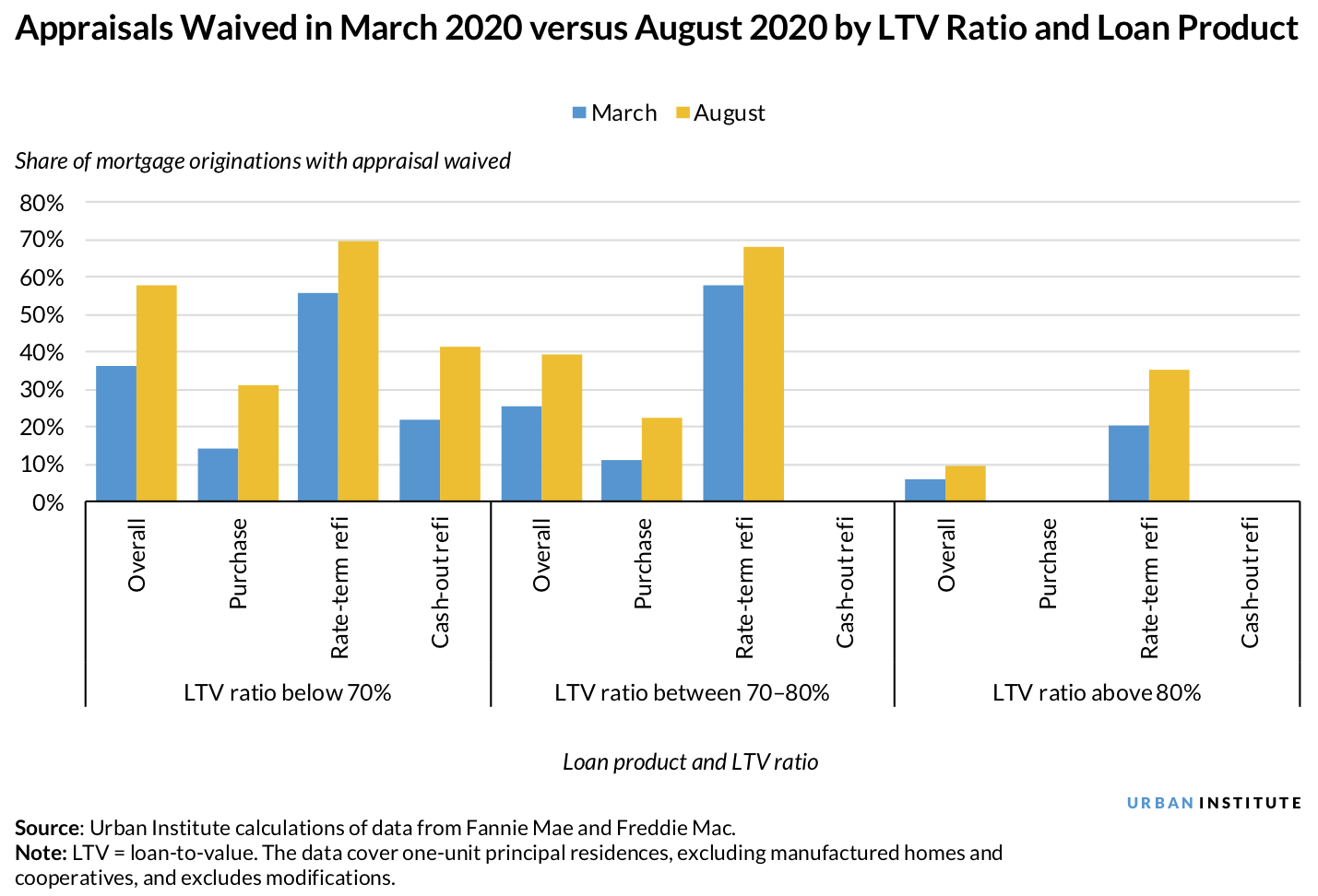

Five months after the FHFA’s announcement, more than one-third of total mortgage originations used an appraisal waiver. The increase in waivers has been most pronounced for refinance originations, with rate-term refinances increasing 14 percentage points and cash-out refinances increasing 13 percentage points.

Appraisal waiver use increased across all LTV buckets and for all mortgage types, most commonly in the lowest LTV categories. But waivers have been used extensively for rate-term refinances even for high-LTV loans. No waivers were offered for cash-out refinances for mortgages with LTV ratios above 70 percent or for purchase loans with LTV ratios above 80 percent.

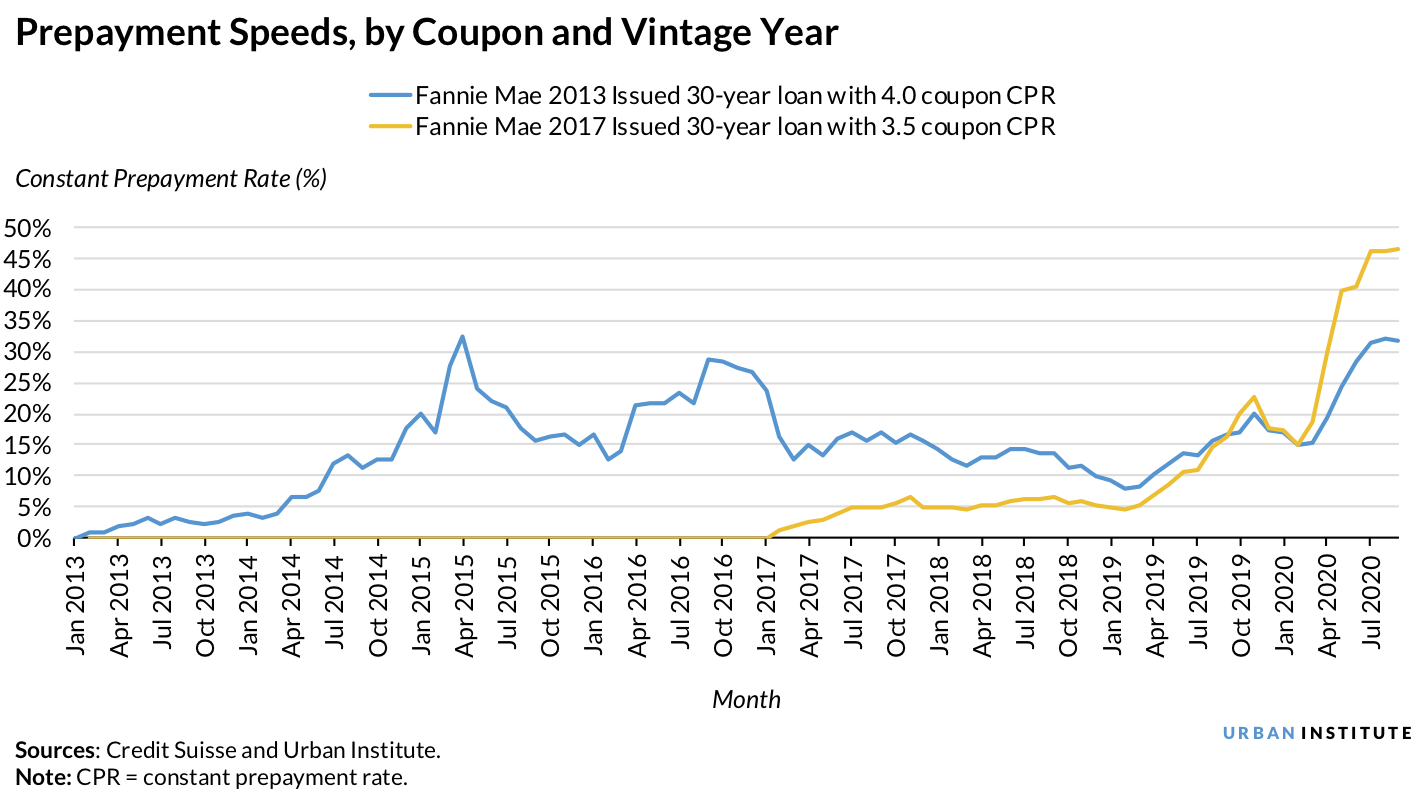

To determine the impact of the appraisal waiver surge on refinance activity, we used mortgage-backed security (MBS) prepayment speeds, which measure the annualized rate at which a pool of loans is repaid and is a proxy for refinance activity because mortgage refinancing is the most common cause of a mortgage prepayment. (Other reasons for prepaying a mortgage include moving or receiving a financial windfall and paying off the mortgage, but these apply to few borrowers.) We compared 2017 MBS prepayment speeds as of September 2020 with 2013 MBS prepayment speeds as of 2015 and 2016. Because the 2013 loans and 2017 loans had similar coupon rates that were attractive for refinancing in 2015 and 2016 and in September 2020, respectively, we believe this to be an apt comparison.

The prepayment speed on 2017 Fannie Mae pools began to rise noticeably in April 2020 and soared to 47 percent as of September 2020, exceeding the 2015 peak rate of 33 percent for 2013 Fannie Mae pools. The much greater prepayment speeds in September 2020 compared with those in 2015 and 2016 suggest that the appraisal waiver, not available as extensively in the 2015–16 surge, has increased refinance activity.

Appraisal waivers come with little risk to the GSEs and could save homeowners money on their annual mortgage payment

Despite the benefits of refinancing, the increased use of appraisal waivers raises concerns about the risks of these mortgages to Fannie Mae and Freddie Mac. But the overwhelming majority of these originations are refinances of mortgages that the GSEs already held, suggesting that the GSEs have not taken on any additional credit risk even as in-person appraisals are waived. Research also suggests that facilitating the refinance process and helping borrowers access lower rates or a reduced term could reduce the likelihood of mortgage default.

Refinancing could offer sizeable benefits to borrowers. Using a basic mortgage calculator, we see that a 30-year mortgage with a balance of $200,000 in September 2017 and a 3.9 percent fixed interest rate (the average rate in September 2017) results in a monthly principal and interest payment of $1,085. After three years of on-time payments, the balance would drop to $188,654. Refinancing the $188,654 with the same 30-year term and no equity taken out, at a rate of 2.9 percent (the rate in late September 2020), would result in a new principal and interest payment of $931, for a savings of $154 per month. Over a year, that’s nearly $2,000 (or 14 percent) in savings.

For borrowers trying to achieve another goal, such as taking cash from their home to provide more near-term liquid assets or shortening the length of the mortgage, the savings will likely be lower.

For many homeowners, the increased use of appraisal waivers has provided a tangible financial benefit and helped them weather the economic stress of the COVID-19 pandemic.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.