A sizeable portion of those who take out mortgages are single female borrowers, but they can face outsize challenges when entering the mortgage market. In 2020, single female borrowers received 19.7 percent of total mortgage loans extended, a much lower share than single male borrowers (32.6 percent) and male-female couples where the male is the borrower and the female is the coborrower (34.5 percent).

In this post, we explore the demographic profiles of single female borrowers and how they have fared in the mortgage market during the COVID-19 pandemic. Additionally, we discuss the policy implications of our analysis and recommend steps policymakers could take to better support this borrower group. (We use the Home Mortgage Disclosure Act database, which collects demographic data on the sex of borrowers. As a result, our findings adhere to a male-female binary, which we recognize is not inclusive of the way everyone identifies and doesn’t account for gender identity.)

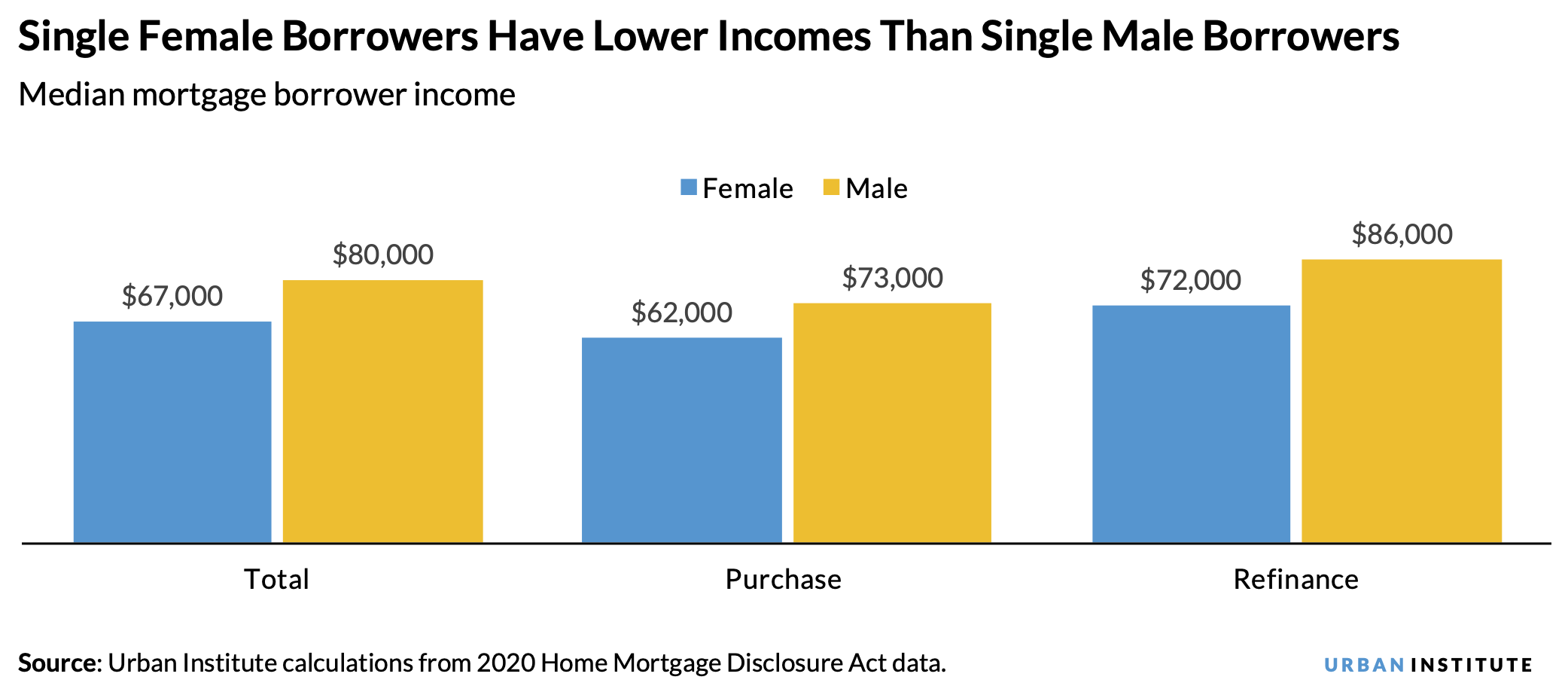

1. Single female borrowers are less affluent than single male borrowers

Single female borrowers tend to have lower incomes, higher mortgage-debt-to-income ratios, and a greater propensity to have below-median incomes or to live in low- and moderate-income communities than single male borrowers.

In 2020, the median income for a single female borrower was $67,000, which was $13,000 less than that of a single male borrower. This trend held for both purchase and refinance loans, with the average income for a single female borrower $11,000 and $14,000 less than for a single male borrower, respectively. In fact, nearly half of purchase loans for single female borrowers are to borrowers earning below 80 percent of area median income compared with just 37 percent for single male borrowers.

As a result of earning less than single male borrowers, single female borrowers also have higher mortgage debt relative to income; the average value of mortgage debt is 3.3 times a single female’s income compared with 3.2 times a single male’s income. And female borrowers tend to live in less affluent communities: 21 percent of purchase loans to single female borrowers are in low- and moderate-income census tracts compared with 18.8 percent of loans to single male borrowers.

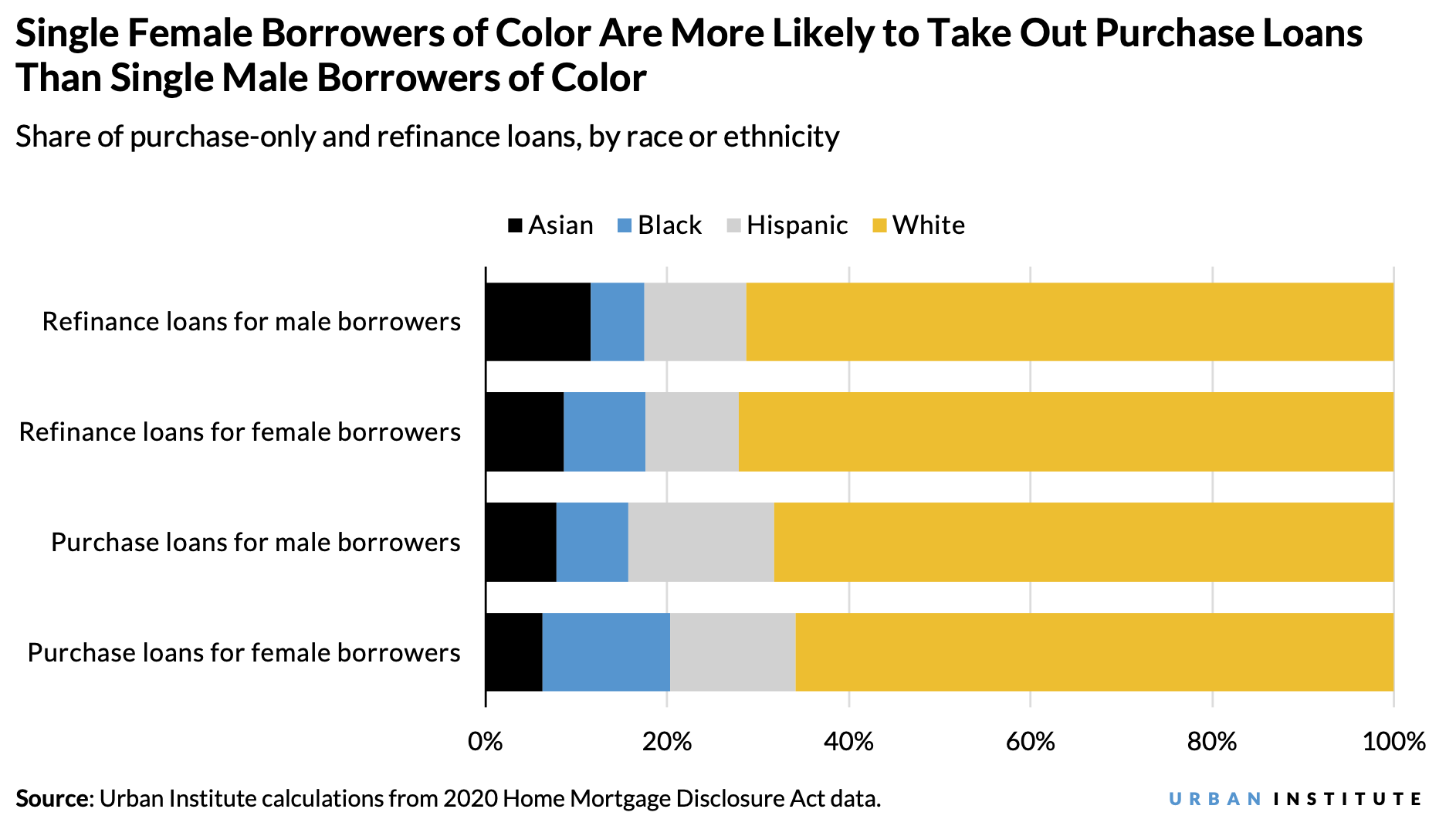

2. Single female homebuying borrowers are more likely to be borrowers of color

In 2020, 34 percent of single female homebuying (i.e., purchase) borrowers were people of color compared with 31.7 percent of single male homebuying borrowers. More single female homebuying borrowers are Black than single male homebuying borrowers, and a lower share are Hispanic and Asian.

For refinancing loans, the racial and ethnic composition skews heavily white, but the overall share of borrowers of color is not too different between single women and single men. We find the same pattern among borrowers of color for refinance loans as for purchase loans: a greater share of single Black women refinance than single Black men, and a lower share of single Asian and Hispanic women refinance than Asian and Hispanic men.

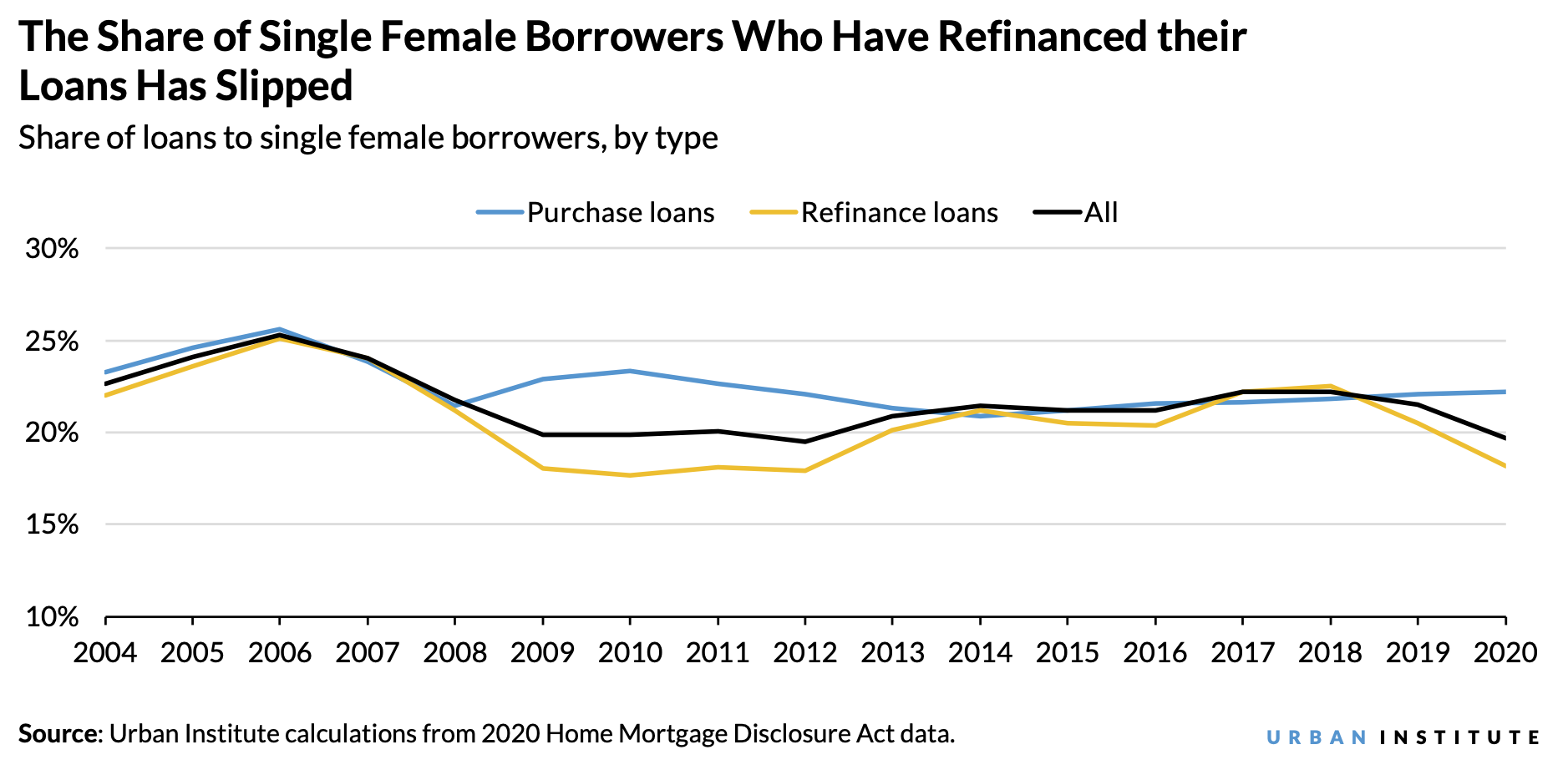

3. The refinancing loan share for single female borrowers has slipped

At a glance, it appears the share of all borrowers who are single women fell to a historic low in 2020, but when we break down the data into purchase and refinance loans, we find the share of purchase loans is still robust. After 2014, the single female borrower share for homebuying gradually increased, while the single male borrower share stayed flat. But the single female borrower refinance share has dropped dramatically since 2018.

Typically, mortgage borrowers refinance when interest rates decline. Despite a considerable drop in interest rates in 2020, single female borrowers refinanced less than single male borrowers. Out of all mortgage loans from single female borrowers, 57.9 percent were refinance loans compared with 60.6 percent for single male borrowers.

If we focus just on market shares, we find that single female borrowers compose only 18.2 percent of the refinance share in 2020 compared with 22.2 percent of the purchase share. That is, the refinance share was 82 percent of the purchase share for single female borrowers. For single male borrowers, the refinance share was 92 percent of the purchase share (31.6 percent refinance and 34.5 percent purchase). This discrepancy points to lenders’ tendency to refinance larger loans first. Single female refinance borrowers have an average loan amount $54,000 less than single male refinance borrowers.

Streamlined refinancing programs could support single female borrowers

Single female borrowers face many challenges when they enter the mortgage market because they are generally less affluent: they have lower incomes and take out smaller loans. These challenges can also affect equity in the mortgage market, as single female purchase borrowers are more likely to be people of color than single male borrowers. Single female borrowing for home purchases held up well during the first year of the pandemic despite these challenges, which is good news, and we applaud continued efforts to expand the credit box to borrowers who can sustain homeownership.

But the refinance share for single female borrowers has declined dramatically. Refinance activity is important in lowering borrower payments, and our analysis shows that the borrowers most in need of refinancing, single female borrowers of color, are the least likely to receive it. These data point to a need for more streamlined refinance programs that these borrowers can take advantage of during the next interest rate decline. Such a program would allow originators to process loans more quickly, which could mean we would see less cherry picking of the largest, most profitable loans—a group where single women are dramatically underrepresented.

Ultimately, if policymakers want to support single female borrowers in the mortgage market, they must understand who these borrowers are and realize that many of the policy interventions that have been discussed over the years, such as expanding the credit box for purchase mortgages and streamlined refinance programs, would be particularly valuable for this group.

The Urban Institute has the evidence to show what it will take to create a society where everyone has a fair shot at achieving their vision of success.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.