<p>Photo by MHJ/Getty Images.</p>

Private mortgage insurance (PMI) is intended to reduce the losses for whatever entity holds the risk of loss for a mortgage that goes into default. The degree of protection provided by PMI has been a topic of conversation lately as Fannie Mae and Freddie Mac’s conservator, the Federal Housing Finance Agency, works to establish their new capital framework (PDF) and as the credit rating agencies begin to update their method for rating residential mortgage-backed securities (RMBS).

Moody’s proposed an update to its residential mortgage-backed securities methodology, which would affect the rating of the bonds for government-sponsored enterprise (GSE) credit risk transfer deals and nonagency RMBS and would give more credit (in the form of lower subordination levels) to deals that have PMI.

Given the increased focus on the topic, understanding the historical behavior of GSE loans with mortgage insurance is important. Examining Fannie Mae loans from 1999 through the first quarter of 2018, we conclude that PMI reduces the loss severity of loans with high loan-to-value (LTV) ratios by 19 to 24 percentage points—a very substantial reduction.

So it is important to recognize PMI’s contribution when developing measures assessing loan-level risk, giving proper “credit” in sizing capital requirements or assessing subordination levels for securitizations.

Mortgage insurance is common for high LTV GSE loans but is rare today with nonagency loans

The Fannie Mae and Freddie Mac charters require that all GSE loans in which the borrower has made a down payment that’s less than 20 percent of their home’s value (i.e., the LTV greater is than 80 percent) obtain some form of credit enhancement; PMI constitutes the overwhelming majority (98–99 percent) of the credit enhancement used.

PMI is designed to reduce Fannie and Freddie’s potential losses in the event of a liquidation to levels comparable with the loss of a loan with a lower LTV ratio. Standard practice is for PMI to reduce the GSE’s exposure for an 85 LTV mortgage by 12 percent (a 75 LTV equivalent); a 95 LTV mortgage by 30 percent (a 66.5 LTV equivalent), and a 97 LTV mortgage by 35 percent (a 63 LTV equivalent).

Lenders may also, at their option, require privatemortgage insurance for loans that will be held in portfolio or included in private label securities. Currently, the percent of postcrisis portfolio loans with PMI is less than 10 percent and is near zero for private label securitizations. The former reflects lenders seeking to take the credit risk themselves in a time of low perceived risk. The latter reflects how the credit rating agencies have, in the postcrisis period, given very little credit to mortgage insurance, in large part because of the low credit ratings of most mortgage insurers.

Mortgage insurance’s decreased role in nonagency lending could change if its value was better understood

Following the Great Recession, S&P, Moody’s, and Fitch rewrote the mortgage insurance (MI) section of their RMBS criteria to focus on two risks to RMBS investors: a mortgage insurer’s inability to pay because of insolvency and a solvent mortgage insurer’s unwillingness to pay. The haircuts assumed by the rating agencies to cover these factors are harsh, resulting in a steep discount to the contribution of the MI. This has made it difficult for the mortgage insurers and the private label security issuers to agree on a price that makes sense to both parties. The smaller rating agencies (DBRS, Kroll, and Morningstar) also give little to no credit for mortgage insurance.

Moody’s has proposed a change to this MI rating methodology, reducing the harshness of the haircuts. If a number of rating agencies change their methodologies to give more credit for mortgage insurance, it may become more attractive for originators to encourage it on loans that could end up in private label securities, as it could potentially lower rates for nonagency borrowers. It could also expand existing credit guidelines for certain products by allowing for increased LTV ratios.

Mortgage insurance substantially reduces the loss severity of higher LTV loans

To assess PMI’s effect on risk, we examined a sample of data on Fannie Mae 30-year fixed-rate, full-documentation, fully amortizing mortgages. We excluded any loans that were put back to the originator; if mortgage insurance is rescinded, it will result in a put back to the originator, as it is not eligible under the GSE charter. We only used Fannie Mae data because Freddie Mac data are released with a longer lag.

The new Private Mortgage Insurance Eligibility Standards (PMIERs), first instituted in 2014 and since revised, make it more difficult for insurers to rescind the insurance. We calculated the loss severity for Fannie as the loss at liquidation divided by the unpaid principal balance at 180 days delinquent. The mortgage insurers reimburse the GSEs for lost interest up to a certain maximum on the loans; this is included in the MI proceeds.

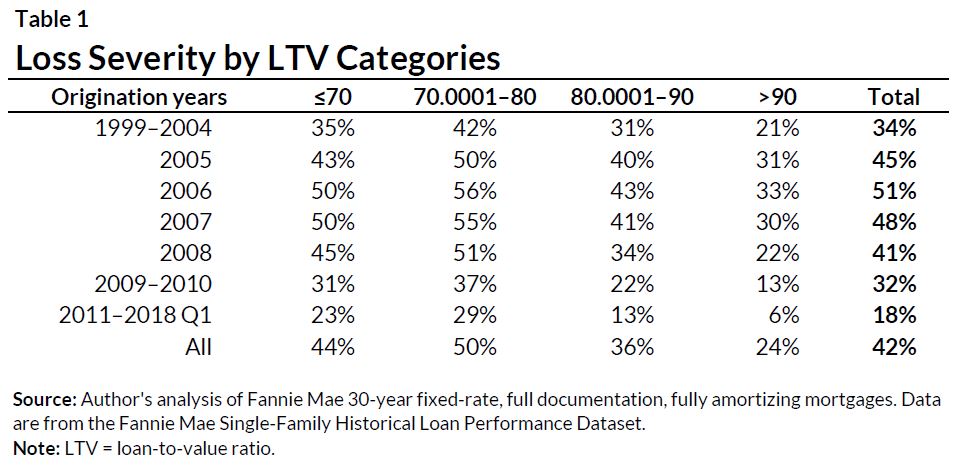

Table 1 shows the loss severity by LTV categories and origination years. All loans with an LTV above 80above have PMI. The net loss severity to Fannie Mae is highest for loans in the 70 to 80 LTV range. This midrange has the highest severity because private mortgage insurance reduces the severity for the loans with LTVs above 80, and the loans below 70 LTV are inherently less risky.

In the first column of table 2, we average the net loss severities for the 80<-90 and >90 LTVs from table 1 and compare those loss severities (which take PMI into account) with the severities that would have occurred without PMI.

We show that PMI cuts the actual loss severity for the 1999 to 2018 Q1 80 LTV+ loans by 22 percentage points, from 53 percent to 31 percent. The severity reduction ranged from 19 to 24 percentage points, with the severity reduction higher in periods with higher severities.

The data clarify that private mortgage insurance does serve to significantly reduce the loss severity of higher LTV loans.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.