<p>FG Trade/Getty Images</p>

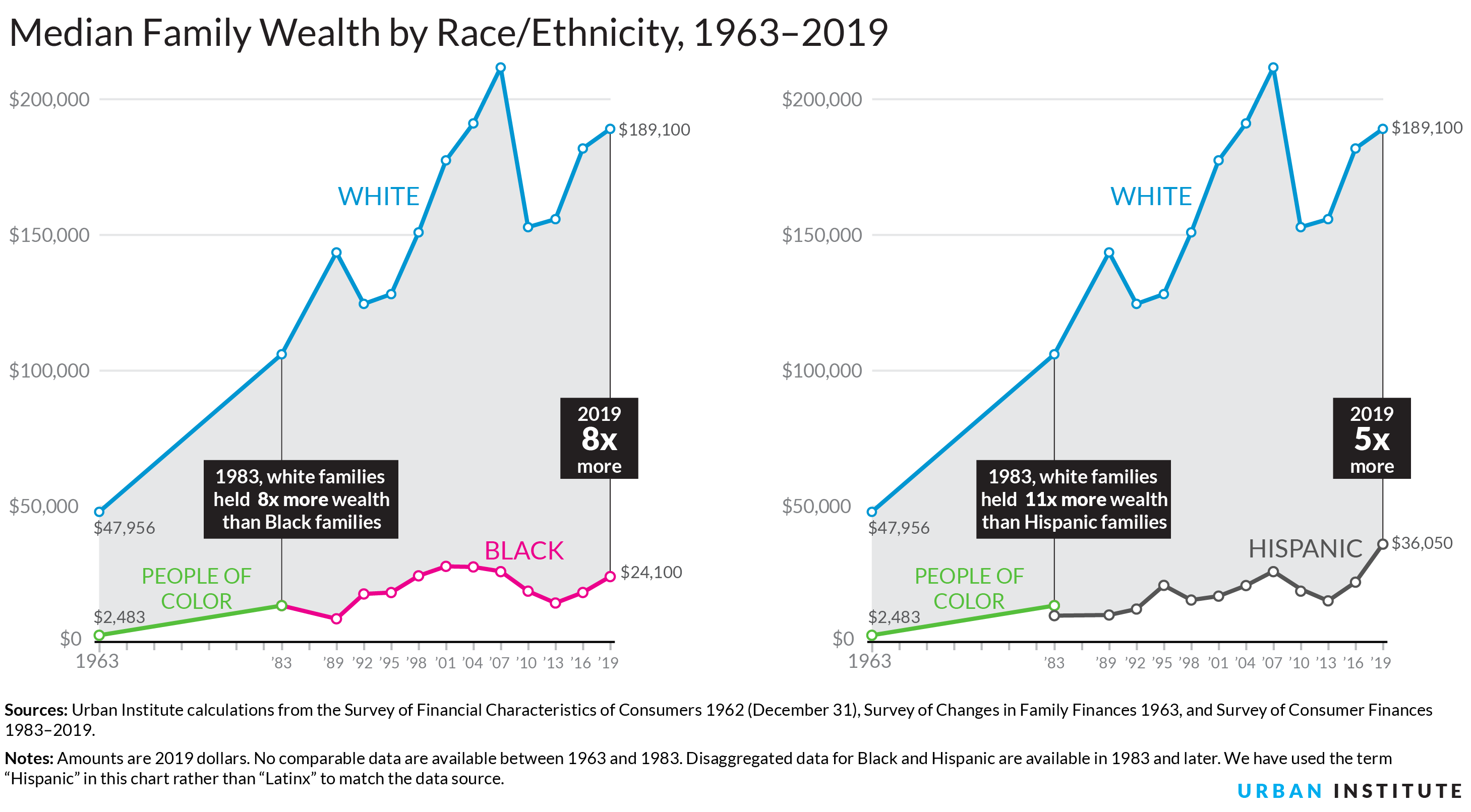

Over the past half a century, the difference in net worth held by families of color compared with white families has expanded substantially and is likely to grow amid the COVID-19 pandemic. In 1963, white families had a median wealth of about $45,000 more than families of color. By 2019, white families’ median wealth had grown to about $165,000 more than Black families and about $153,000 more than Latinx families.

Wealth inequity matters for everyone, not just those at the bottom. Wealth is not just money in the bank but an ever-present resource that allows families to address emergencies and invest in wealth-generating assets, such as earning an education, buying a home, or starting a business. Wealth enables people to reach their full potential and contribute more to the overall economy, which benefits Americans of all backgrounds.

To close the racial and ethnic wealth gap, policymakers need bold solutions, which are now more pressing because of the COVID-19 pandemic’s disproportionate impact on Black and Latinx families.

An inclusive pandemic recovery is necessary to ensure COVID-19 doesn’t exacerbate the racial and ethnic wealth gap

In 2019, the median Black family had 13 cents of wealth for every dollar held by white families, and Latinx families had 19 cents to the dollar. Put another way, the typical white family had eight times the wealth of the typical Black family and five times the wealth of the typical Latinx family. Despite some fluctuations over the past four decades, this ratio disparity was as high in 2019 as it was in 1983 for the typical Black family and half what it was in 1983 for the typical Latinx family.

The 2019 wealth data were collected before COVID-19 began to spread in the US, so the pandemic’s impact on wealth and wealth disparities remains to be seen. During the Great Recession, the most recent time when employment and economic growth had substantial declines, the average wealth of American families decreased by 28.5 percent compared with what wealth would have been, given wealth accumulation trajectories. White families’ wealth fell 26.2 percent, while the wealth of Black families fell by 47.6 percent and Latinx families’ wealth fell by 44.3 percent.

The current economic downturn has differed from the Great Recession in several respects, including a sharper increase in unemployment. Black and Latinx families have been more likely than white families to experience these consequences. These families have experienced higher rates of job loss, of using savings or selling assets to meet spending needs, and of risking exposure through in-person work or public transit.

The pandemic itself has also hit Black and Latinx communities harder, as they are more likely to contract, be hospitalized for, and die from COVID-19. These families are also more likely to not have health insurance, which means that contracting COVID-19 could force them to deplete their savings, incur debt, or forgo medical care. And families who suffer the death of a member face the additional burden of funeral expenses.

Altogether, the economic and health consequences of COVID-19 will most likely further deplete the wealth of Black and Latinx families, which does not bode well for reducing the racial and ethnic wealth gap or for these families’ near- or longer-term economic well-being.

How policymakers can reduce the racial and ethnic wealth gap

Closing the wealth gap requires short- and long-term policies that provide economic relief over the next year and reduce the structural barriers preventing Black and Latinx people from building wealth.

In the short term, many families need financial support to offset lost income from job loss, reduced hours, and closed businesses. These losses can prevent people from paying their bills, increasing the threat of eviction and foreclosure. As of mid-December, 24.4 percent of Black households and 19.9 percent of Latinx households with mortgages were behind on their payments, compared with 8.3 percent of white homeowners. Although Congress continues to seek partial solutions to help struggling families in the short run, they do little to ease wealth inequality in the long run. Urban Institute researchers have assessed some of these short-term solutions and proposed additional ones to address the income, eviction, and foreclosure crises and health care needs.

More permanent remedies address the occupational segregation that results in disproportionate shares of Black and Latinx people in jobs where it is more difficult to stay at a safe distance, avoid crowded situations and enclosed spaces, and limit duration of exposure. Although the COVID-19 crisis will end, taking these types of proactive measures could better protect these workers’ health in the future. Ensuring Black and Latinx people have more access to quality health care and insurance is important during the current crisis and for their long-term well-being.

Long-term solutions must also address the root causes of racial inequities. These policies can take the form of a federal job guarantee that helps sustain families when workers lose their jobs, efforts that accelerate home equity for families of color, and baby bonds that give young adults an equitable chance at building their own wealth. Additional policies, such as a refundable savers’ credit, automatic individual retirement accounts, and universal health insurance, should be examined for their ability to reduce the racial wealth gap.

By enacting short-term solutions, policymakers can help ensure the racial wealth gap does not widen further as we fight the pandemic and look toward recovery and rebuilding. Longer-term solutions would set the country on a path of greater equity and inclusion and take steps toward closing the wealth gap, creating a healthier economy and more prosperous future for all Americans.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.