Photo by westend61 via Getty Images.

US Senator Cory Booker (D-NJ), whose presidential campaign ended last week, introduced a bill to create American Opportunity Accounts, or “baby bonds,” as a bold solution for closing the racial wealth gap. But this proposal has yet to be fully tested at a large scale. It is time to invest in a demonstration and evaluation of this idea.

The racial wealth gap has become a widely-discussed issue not only by scholars, but also by the media, advocates of economic security, and 2020 presidential candidates.

The racial wealth gap is the disparity in net worth held by white families and net worth held by families of color. The Urban Institute’s research shows that at the median, white families have 10 times more wealth than African American families and 8 times the wealth of Latino families. Similarly, young white adults ages 18 to 24 have 15 times the median wealth of African American young adults.

Wealth is not just for the wealthy

Wealth is used to pay college tuition, start a small business, and for down payment on a home – investments that can provide a stepping stone to the middle class. Part of the racial wealth gap is explained by disparities in the receipt of gifts and inheritances.

Black and Hispanic families are five times less likely to receive a large gifts and inheritances and receive smaller amounts when they do. Private wealth transfers like this could make the difference between when a family puts a down payment on a first home or how much debt a college graduate has when they enter the workforce.

Booker’s proposal is based on a concept developed by Darrick Hamilton, executive director of the Kirwan Institute for the Study of Race and Ethnicity, to provide a publicly funded endowment to every newborn, with babies born into low-wealth families receiving tens of thousands of dollars more than babies born into affluent families.

How do baby bonds work?

Under Senator Booker’s bill, every newborn would receive an initial endowment of $1,000. Then, each family’s annual income would be used—given the lack of data collected by the government on family wealth—as the basis for the sliding scale to determine the amount of each annual contribution to the child’s endowment.

The American Opportunity Accounts would be held by the US Treasury Department until the child becomes a young adult. At that point, the young adult could use the endowment to invest in an asset, such as education or a home.

Baby bonds would provide larger transfers to young adults of color

The intent is for every young person to enter their adult life with an endowment that would lead them to future economic security. According to our estimates (using an annual compound interest rate of 2 percent), if today’s 18-year-olds from families in poverty had received baby bonds, they could start adulthood with endowments of up to $42,253.

Those coming from lower-income families would have higher baby bond endowments than those from higher-income households, because they would have received higher annual transfers to their endowment each year during childhood under Senator Booker’s proposed design.

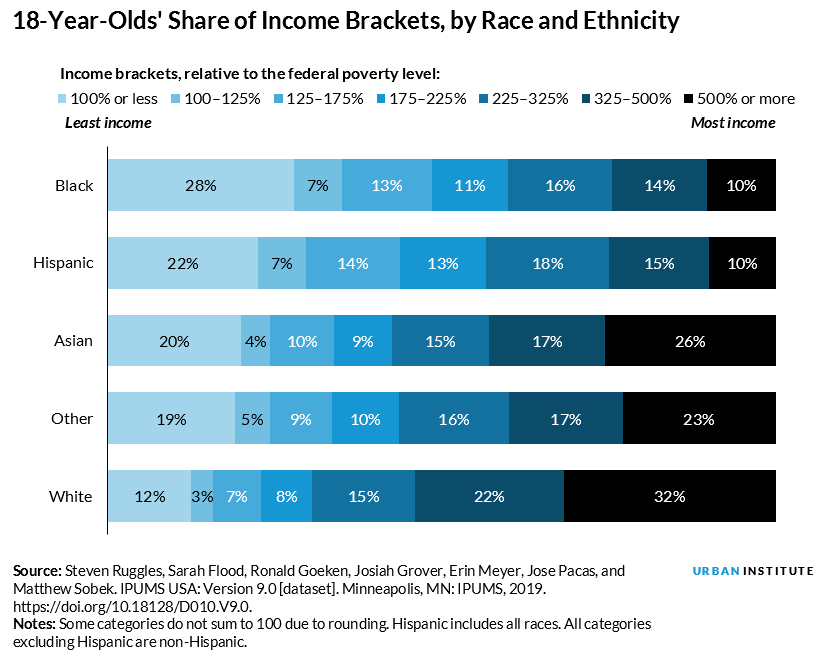

The figure below illustrates the 2017 share of 18-year-olds in each racial and ethnic group who fell into the income brackets Booker’s bill uses to determine the annual contribution a child would receive.

Every racial and ethnic group has a substantial share of 18-year-olds with family incomes at or less than the federal poverty level. However, there are considerably more 18-year-olds of color who fall into this income bracket. Under Booker’s bill, children whose family incomes remain at this level would receive annual contributions of $2,000 until they turned 18.

By contrast, the figure also shows that 18-year-olds of color are considerably less well represented than white 18-year-olds in families with incomes greater than 500 percent of the poverty level. A child born into a family whose income falls into this bracket would still receive $1,000 at birth but would not receive an annual supplement to their endowment in any subsequent year that the household income was this high.

How much would baby bonds cost, and how could we afford it?

Senator Booker’s offices estimate the cost to be $60 billion annually, and the Committee for a Responsible Federal Budget estimates a cost of $650 billion over a decade. Although this is a significant amount of money, Senator Booker’s bill offers a set of tax increases geared to the wealthiest households to pay for the cost increase. The Committee for a Responsible Federal Budget estimates that these tax increases would more than offset the cost of Baby Bonds.

An alternative “pay for” approach to consider is a more equitable treatment of existing tax subsidies that the government pays to families to encourage wealth building. In 2013, the government spent approximately $385 billion per year on asset-development subsidies, such as home mortgage interest deductions, property taxes, and retirement savings plans.

However, about 70 percent of this tax expenditure accrues to the highest 20 percent of income earners. By making some equitable adjustments in the design of these tax subsidies, generated savings could be used to pay for endowments for young adults to establish their economic security.

Would baby bonds close the wealth gap?

A study by Naomi Zewde of the City University of New York (formerly at Columbia University) finds it may. She simulated how baby bonds could reduce the wealth held by young white adults from 15 to 1.6 times the wealth held by young Black adults.

These results are very promising. But a policy change of this magnitude warrants a demonstration and evaluation to better understand what it would take to implement such an innovative program and to measure the effects and cost of baby bonds.

A plan for future study

To obtain results within a time frame that could facilitate near-term policy decisionmaking, baby bonds could initially test the effects and costs of baby bonds for people ages 18 to 24.

In a hypothetical study, a sample of this age group could be given an endowment based on their household income. The study could follow how these young adults invest their endowments, measure how their income levels and wealth change over time, and determine if the initial wealth gaps between young white adults and young adults of color decline.

Such a study would represent a significant undertaking by the philanthropic and research sectors, but it could boost understanding of this bold proposal to address our country’s widening racial wealth gap from the bottom up.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.