<p>Photo courtesy of the Manufactured Housing Institute.</p>

Increasing the annual supply of manufactured housing (MH) could ease the country’s severe shortage of affordable housing.

But current production of manufactured housing is low, and restrictive zoning and expensive financing might be to blame. We can increase demand for these homes (and, in turn, supply) by helping more people understand their financing options for MH. For instance, many borrowers might qualify for a low-cost mortgage rather than for a personal property loan.

To demystify this market, we explain four ways financing for manufactured housing differs from financing in the rest of the single-family market.

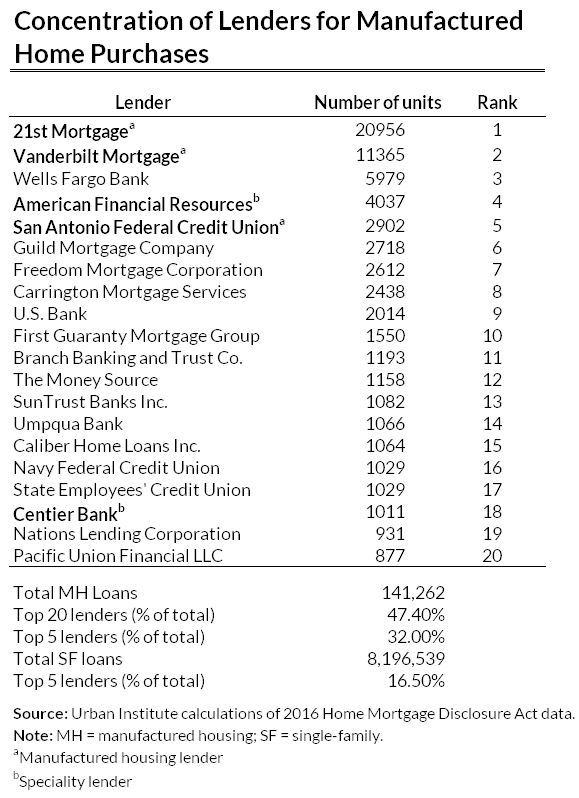

1. The market is served by a small group of specialized lenders

We used Home Mortgage Disclosure Act data to classify manufactured housing lenders into three categories:

- MH lenders: More than 90 percent of their single-family business is manufactured housing

- Specialty lenders: 15 to 90 percent of their business is manufactured housing

- General lenders: Less than 15 percent of their business is manufactured housing

Of the five lenders that offer the most loans to purchase manufactured housing, 78 percent of the lending is originated by three MH lenders, two of which dominate the market: 21st Mortgage (20,956 loans) and Vanderbilt Mortgage (11,365 loans). The MH lender San Antonio Credit Union was in fifth place, with 2,902 loans.

Rounding out the top five lenders are American Financial Resources, the largest specialty lender, which made 4,037 MH loans in 2016, and Wells Fargo, the largest general lender, which made 5,979 loans. The other lenders in the top 20 are all general lenders, except for one other specialty lender, Centier Bank.

Loans made by MH lenders are generally more likely to be chattel (personal property) loans, whereas loans made by general lenders are usually mortgage loans, which carry lower interest rates.

The concentration of lenders is higher in the MH market than in single-family lending in general. The top five MH lenders compose 32.0 percent of the total market, versus 16.5 percent in the overall single-family market. The top 20 MH lenders compose 47.4 percent of the total market, versus 31.1 percent in the overall single-family market.

2. The average loan size is small

The median loan size for manufactured homes was $72,000, compared with $199,000 for single-family homes. This reflects MH’s role as a source of affordable housing.

Within the manufactured housing market, the average loan size for borrowers served by general lenders is $90,000, compared with $56,000 for MH lenders and $58,000 for specialty lenders.

These results indicate that general lenders are more apt to finance multiple MH units that are combined into one dwelling and are more apt to finance the land and the manufactured home.

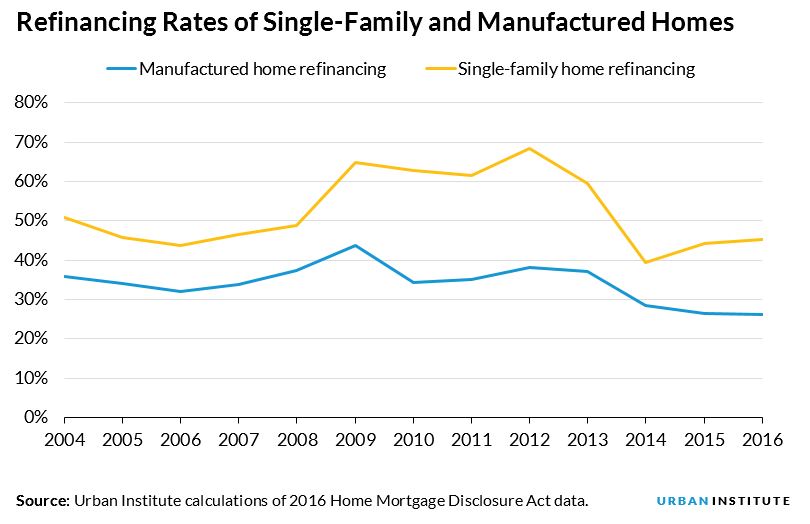

3. Refinancing is rare and is usually done by general lenders

The share of manufactured home borrowers who refinance has always been lower than that of single-family borrowers. After narrowing slightly, the gap between the refinance share in the single-family and manufactured housing markets has steadily increased since 2013.

The refinance share in 2016 was 45 percent for single-family loans, compared with 26 percent for MH loans. This is in part because of the lack of cash-out refinancing opportunities for MH.

Eighty-four percent of refinance mortgages were made by general lenders. Small, specialized MH lenders are mostly in the purchase mortgage business and don’t have as much of a footprint in the refinancing space.

This trend could be because of the lack of refinancing options for small mortgages, difficulties in refinancing chattel loans, few opportunities to refinance to take cash out, or the fact that the major marketing channel for the MH lenders is new homes from MH dealers.

4. Cash is king, particularly for used units

Although we don’t have nationwide data on cash sales of manufactured housing, data from the Texas Manufactured Housing Association show that in Texas, the most popular state for manufactured housing, 56.9 percent of manufactured homes in 2016 were purchased using cash.

Cash sales were more prevalent for used properties than for new properties. Thirty-two percent of new homes were purchased using cash, while 74 percent of used homes were purchased using cash.

During the manufactured housing crisis in the early 2000s, when shipments and prices plummeted because of an oversupply of units shipped in the late 1990s, the cash-sales share for MH was well above that for single-family homes.

Since 2008, the cash-sales share has narrowed between the sectors, reflecting in large part the increase in the cash-sales share in single-family homes following the Great Recession, particularly as investors bought foreclosed properties.

The government-sponsored enterprises (GSEs), Fannie Mae and Freddie Mac, are required to expand support for manufactured housing during 2018 as part of their Duty to Serve directive.

As the GSEs and other policymakers, legislators, and advocates continue to consider the potential of manufactured housing to ease the shortage of affordable housing, it’s important to understand that lending for these homes is concentrated in the hands of a few companies that specialize in this lending, that the loans are small, that refinancing is rare, and that cash is king, particularly for used units.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.