<p>Photo courtesy of the Manufactured Housing Institute.</p>

Increasing the annual supply of the one of the most affordable types of housing, manufactured housing, from the 93,000 units produced in 2017 could ease the country’s severe shortage of affordable housing.

In our new research brief, we explain how encouraging buyers of manufactured homes to choose mortgages over chattel loans could make manufactured housing more affordable, potentially leading to an increase in demand and supply.

Chattel loans dominate the manufactured housing finance space

Most manufactured homebuyers use chattel loans rather than more affordable mortgage loans to finance their purchase. To qualify for a mortgage, a manufactured home must be titled as real property; in most states, this requires the owner to own both the structure and the land on which it is sited. Otherwise, the property is personal property and is eligible only for chattel financing.

Why might a mortgage-eligible buyer use more expensive chattel financing instead? We think it’s mostly about convenience and confusion.

Chattel loans are more convenient for most manufactured homebuyers for two reasons:

- In most states, manufactured homes are titled by default as personal property, whether or not the buyer owns the land. It’s up to the owner to change this designation by documenting land ownership and that the home is fixed to the land. This is a hassle.

- Chattel lenders are also typically available on-site when manufactured homes are sold, so the borrower can walk away with a loan the same day the home is purchased.

Confusion also plays a part because consumers are likely unclear about rules for titling, which differ by state.

Buyers choose chattel loans for other reasons. Many chattel borrowers do not qualify for a mortgage, as the qualifying criteria are more stringent. Some states have a lower property tax on personal property than on real property.

And in some cases, a chattel loan might make more sense. For example, if the land belongs to a family, the family might not want one member to encumber the land because he or she has put a manufactured home in the corner of the property, and subdividing the land requires additional cost.

Nevertheless, we wanted to understand more about how often a buyer eligible for a mortgage uses a chattel loan and to get more clarity on how much additional cost chattel financing adds. So we looked into the data.

Most buyers who use a chattel loan qualify for a mortgage

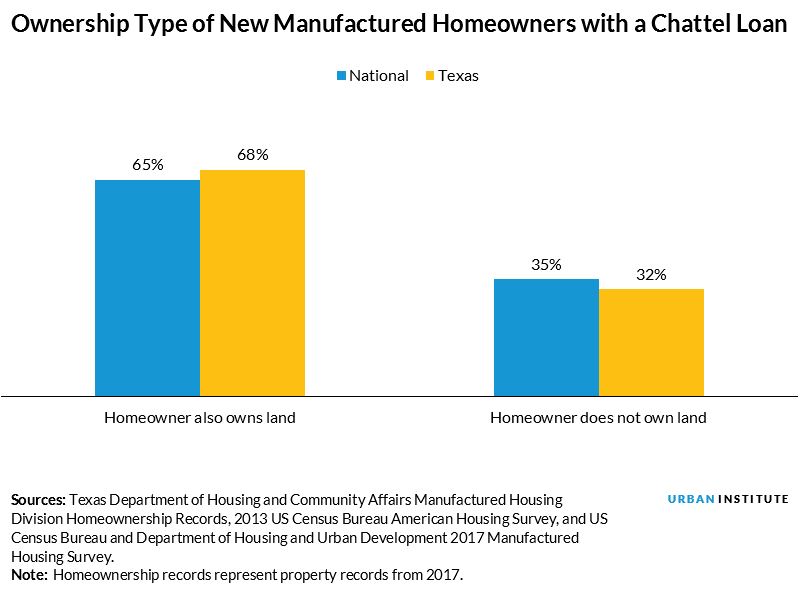

A sizable majority of manufactured homebuyers taking out chattel loans were eligible for a mortgage. We merged data sources to look at the titles of manufactured homes in the United States and in Texas, where more than 20 percent of new manufactured homes are shipped.

In 2017, 81 percent of newly shipped manufactured homes were titled as personal property, making them eligible for only a chattel loan, and 19 percent were titled as real property, making them eligible for a mortgage. Of the 81 percent titled as personal property, 65 percent of owners owned the land and could have qualified for a less expensive mortgage.

In Texas, the share of manufactured homes titled as personal property for which the owner owned the land was 68 percent.

These percentages are upper bounds. Not everyone who has purchased a manufactured home and owns the land would qualify for a mortgage.

Chattel loans cost consumers more than mortgage loans

How big a difference does mortgage financing make? We analyzed Home Mortgage Disclosure Act data and found that the average chattel loan costs consumers 4.4 percentage points more per year than the average mortgage for manufactured housing. On an $80,000, 20-year loan, this additional cost would be $2,600 a year, or 5.6 percent of income for a family making $50,000 a year.

Of course, not everyone who takes out a chattel loan saves 4.4 percent by switching to a mortgage. Differences in credit profiles, loan-to-value ratios, and closing costs could change the equation. But the cost differential between chattel and mortgage financing is significant.

Although not a universal solution, encouraging more manufactured housing customers to consider a mortgage would provide better consumer protection and offer considerable savings. From a public policy perspective, it would be useful to explore whether states can make the titling process easier and less expensive for manufactured housing, perhaps with an expedited process at the state level.

The reduced costs and greater protections could stimulate demand for manufactured housing, thus boosting production of these homes and adding units to the scarce supply of affordable housing.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.