<p>A manufactured home by Clayton Homes. Photo courtesy of Clayton Homes.</p>

Manufactured housing is the least expensive type of housing. So, considering the severe shortage of affordable housing in the US, why is the annual production of new manufactured housing so low?

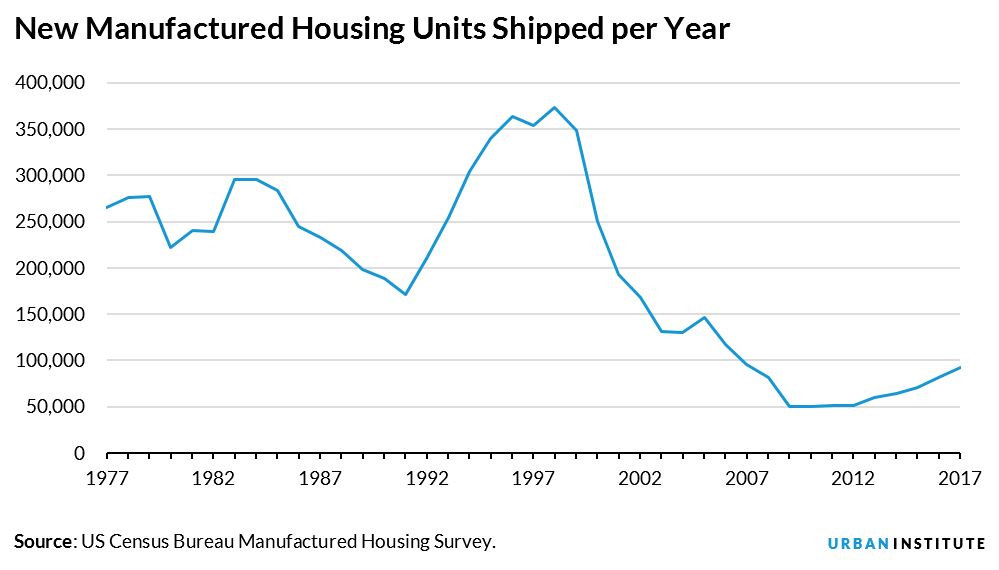

Manufactured housing is 35 to 47 percent cheaper per square foot than new or existing site-built housing, yet the number of manufactured homes shipped each year has gone from averaging 242,000 per year between 1977 and 1993 to just 92,500 units in 2017.

Before 1977, manufactured housing was unregulated at the national level. In 1977, the US Department of Housing and Urban Development (HUD) implemented the first federal construction standards after passage of the 1974 Manufactured Housing Construction and Safety Standards Act.

These requirements regulate energy efficiency, durability, fire safety, transportability, and material and construction quality. Additional quality improvements were implemented through 1994 and 2000 HUD code updates. Between 1977 and 1993, the number of manufactured housing units shipped fluctuated between 200,000 and 300,000, averaging 242,000 per year.

From 1994 to 1999, the number of manufactured units increased to more than 300,000 per year, an unsustainable number caused by overproduction and loosened financing standards, which resulted in credit being extended to borrowers who could not afford the units.

The decline of manufactured housing

As foreclosures and repossessions increased in 1999, unsold and used manufactured units flooded the market, reducing demand for new units. Tighter credit standards for new borrowers further decreased demand, and production crashed, decreasing to an average of 170,000 per year between 2000 and 2005.

After 2005, the number of units shipped continued to slip. Since 2007, the number has been less than 100,000 per year, reaching a low of 50,000 units per year from 2009 to 2012. 2017 marked a modest recovery to 92,500 units (87,600 for the first 11 months, which we annualized, considering reduced December activity).

A similar picture unfolds if we look at manufactured homes as a share of the new stock of single-family homes, which ranged from 16 to 25 percent between 1977 and 1995 but has averaged just 10 percent in recent years.

Three reasons manufactured housing production remains low

Today’s affordable housing crisis has resulted from home prices and rents outpacing family incomes. Manufactured homes, which are less expensive and of a higher quality than in the 1990s, could help solve this problem. Yet the number of manufactured units shipped remains low for three reasons.

1. Restrictive zoning

Approximately 34 percent of new manufactured homes are in communities, while the rest are on privately owned land (often owned by the person who owns the manufactured home or by a relative). Restrictive zoning ordinances affect both types.

As zoning has become more restrictive, it has become more difficult to build new manufactured housing communities, particularly in areas with good schools, jobs, and public transportation. In addition, restrictive zoning has driven up land costs. The result: few new manufactured home communities have been built since 2000.

Moreover, localities often restrict the placement of manufactured homes through outright bans that do not even mention aesthetic criteria or by requiring that they be placed on larger lots than site-built homes.

These zoning restrictions impede the use of manufactured homes as an affordable housing tool in urban and suburban areas and may help explain why a disproportionate amount of manufactured housing is in rural and unincorporated areas (49 percent of units are located outside a metropolitan statistical area, versus 22 percent of all single-family detached housing units).

2. Restrictive or unavailable financing

Manufactured housing may be titled as either personal property (chattel) or real property (mortgage). In 2016, only 17 percent of new manufactured homes shipped were titled as real property. Most were financed as chattel.

Chattel loans tend to have lower balances, have shorter terms (10, 15, or 20 years), carry higher interest rates, and have fewer underwriting requirements than their mortgage counterparts. In most states, to obtain a mortgage loan, the manufactured home must be affixed to a permanent foundation on land owned by the manufactured home’s owner. The mortgage encumbers both the land and the manufactured home.

Many people who owned their own land and purchased a manufactured home between 2001 and 2010 took out a chattel loan despite their theoretical ability to apply for a mortgage. The Consumer Financial Protection Bureau estimates that 65 percent of this group used chattel loans for two reasons: First, it’s an easier transaction with lower costs at origination, often arranged in conjunction with the home purchase. Second, manufactured home loans tend to be for smaller amounts, for which mortgage financing is difficult to secure.

The lack of access to financing, particularly for small mortgage loans, and the higher costs to consumers for chattel lending increase the price of manufactured homes, which stymies demand.

3. Lower appreciation

While manufactured homes have lower initial costs, the homes do not have the same price appreciation of site-built homes. Yet much of the appreciation in single-family, site-built home values is because of the appreciation of the land, not the structure. Since 2000, the value of the land has, on average, appreciated 2.35 times the rate of the structures.

Studies that compare the appreciation of manufactured housing units on the homeowner’s land with the appreciation of site-built homes have mixed results. Some show similar appreciation, and others show slightly lower appreciation. Lower appreciation for manufactured housing may be because of the lack of financing options available for older manufactured homes, which affects resale value.

Production is expected to increase this year

Absent changes, we expect the number of manufactured housing units shipped to gradually increase. Further stimulus from the 2018–20 implementation of Fannie Mae and Freddie Mac’s Underserved Market Plans, and the fulfillment of their Duty to Serve Obligation, which focuses on manufactured housing, may also boost production. HUD has also recently renewed its focus on manufactured housing, announcing that it will “review its existing and planned manufactured housing regulatory actions to assess their actual and potential compliance costs and reduce regulatory burden.” Noting the “significant role [manufactured housing] plays in affordable housing,” HUD has invited the public to comment by February 26, 2018, on these regulations “to assist in identifying regulations that may be outmoded, ineffective, or excessively burdensome and should be modified, streamlined, replaced, or repealed.”

Industry capacity has shrunk dramatically since 1990, when 100 manufactured housing producers operated 250 plants, but the industry should be able to quickly ramp up from the 34 operators and 121 plants in operation today if demand picks up.

The government-sponsored enterprises’ plans should improve financing and enhance market information in this sector. Major changes on the zoning front remain unlikely, but we believe the number of units shipped could increase significantly from the 2017 level of 92,500. If the number of units shipped returned to the 1977–93 average of 242,000 per year, this would add significant affordable supply to the housing market.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.