<p>Photo by Stockfour/Shutterstock.</p>

Income-driven repayment (IDR) plans, which tie monthly payments to a borrower’s income, have become increasingly popular among student loan borrowers. Despite the growth of these plans, we’ve only recently begun to understand which borrowers opt for IDR.

In a recent blog post, I presented data from the 2016 Survey of Consumer Finances (SCF) on the household incomes and average loan size of borrowers who report enrollment in federal income-driven student loan repayment plans.

In this post, I explore which households use IDR, which use a non-IDR plan such as standard or graduated repayment, and which report that they are not making payments because of forbearance, inability to pay, or reliance on some other debt forgiveness program.

These data are subject to caveats. The data are a snapshot in time, so they capture borrowers who have just entered repayment and those who have been in repayment for decades. Further, the SCF is a small, self-reported sample, so small differences might be attributable to sampling error rather than substantial differences in the underlying populations.

Nonetheless, SCF data provide a window into the types of households that use IDR, relative to borrowers who use other repayment plans and those not making payments.

IDR plans have been available to some federal borrowers since 1994, but the recent uptick in IDR usage might explain why borrowers using IDR to repay student loans tend to be younger than those using non-IDR plans. Borrowers older than 50 are less likely to be on IDR repayment plans.

In households where the highest level of education attained by the household head or partner is an associate’s degree or less, borrowers tend to be equally likely to use IDR plans, use non-IDR plans, or not make payments. At higher education levels, borrowers are more likely to use non-IDR plans, though a sizable share still use IDR.

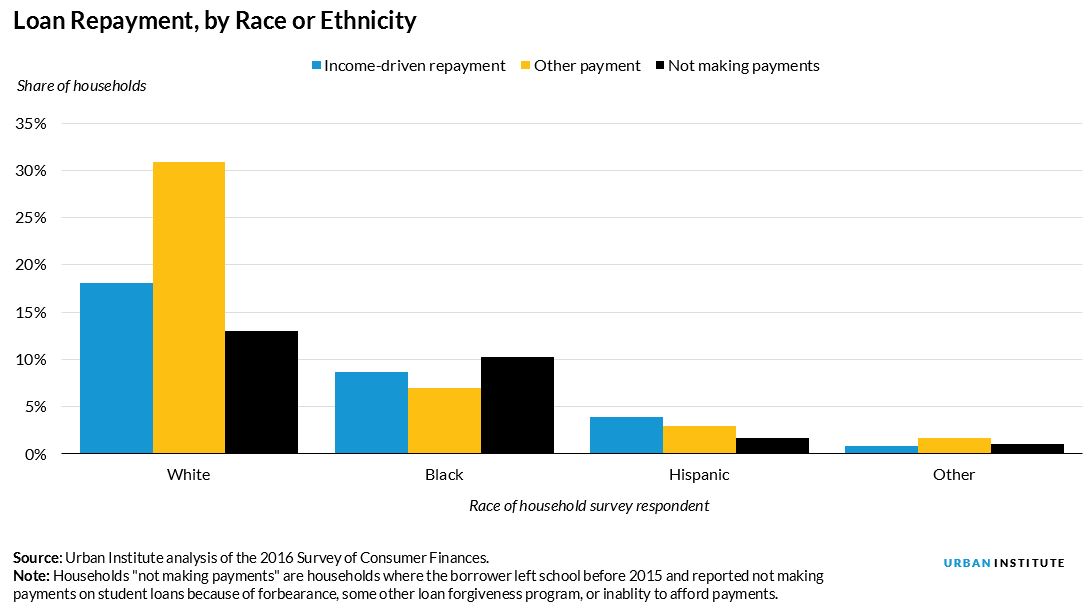

Recent studies have shown that the risk of student loan default is higher for borrowers of color, particularly black borrowers, than for white borrowers. Households headed by a person of color are about equally likely to use IDR as they are to use non-IDR repayment plans, while households headed by white respondents are more likely to be on a non-IDR plan.

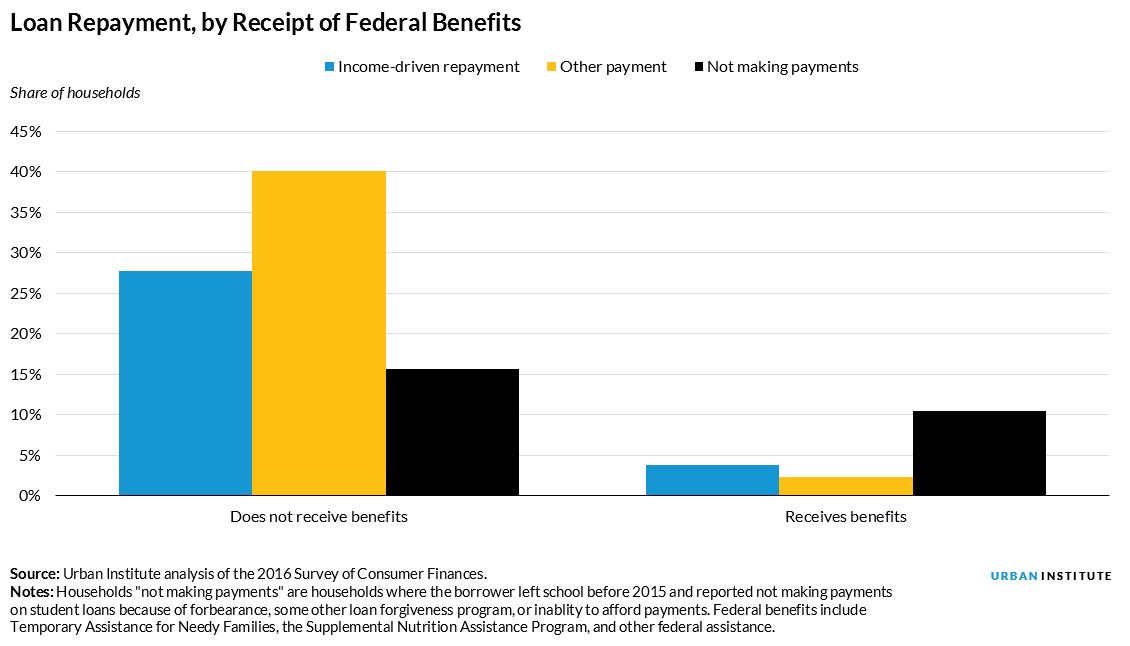

Another way of understanding the economic needs of borrowers in different repayment plans is to look at whether anyone in the household receives a federal benefit from Temporary Assistance for Needy Families, the Supplemental Nutrition Assistance Program, or other welfare benefits such as Supplemental Security Income. More than a third of borrowers not making payments on their student loans also noted they were on federal assistance.

As policymakers revise and reshape parameters and eligibility for IDR plans, these data provide an important glimpse into the demographics of borrowers who use IDR plans. While the US Department of Education has improved its reporting on borrowers who use IDR, these data underscore the need for further data, particularly by household need, race, and ethnicity.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.