<p>Rosa Elisa Salgado, center, walks down a corridor of the Wolfson Campus of Miami Dade College after an interview, Monday, May 4, 2015, in downtown Miami. The Colombian-born grandmother, who prefers to say that she is between 70 and 80-years-old, graduated from the college with two of her grandchildren, May 2, 2015. Photo by Wilfredo Lee/AP.</p>

According to recently released US Department of Education (ED) data, 17 percent of Americans who owe money on federal student loans are over age 50. These older borrowers collectively hold $247 billion in outstanding federal student debt, an amount that has grown roughly threefold since 2003, accounting for inflation.

Using new data on education debt, we can see who these borrowers are and what their needs may be. Our analysis shows that older borrowers fall into two groups: those who have education debt for themselves (roughly 3.5 percent of older adults), and those that have debt for their children or grandchildren (roughly 8 percent). Although both groups hold similar amounts of debt, people who have education debt for themselves are more likely to be behind on payments or say they feel financially insecure. Policymakers who want to reduce the impact of education debt among older Americans should consider interventions that distinguish between these two groups.

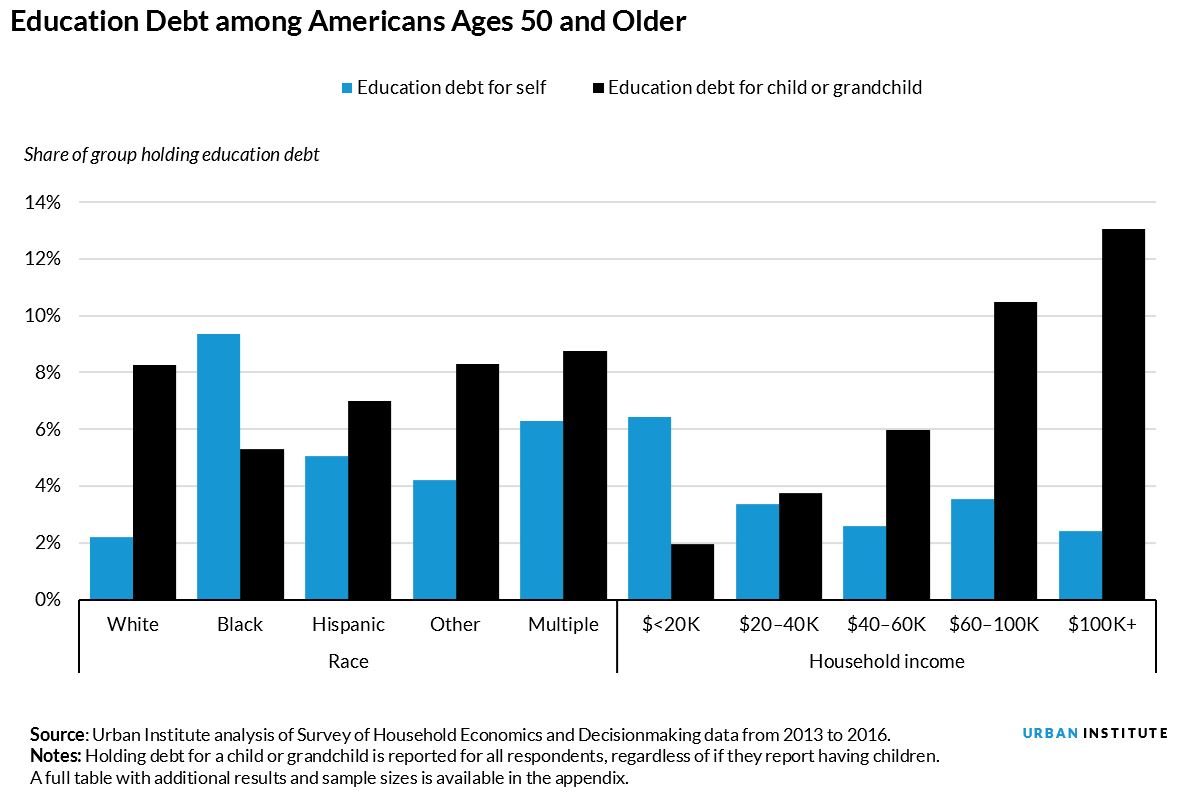

Borrowing patterns and outcomes differ by gender, race and ethnicity, socioeconomic status, and educational attainment. We find that the likelihood of holding education debt among people ages 50 or older varies by demographic characteristics, but the story differs depending on whether the debt is held for the adult or for their children or grandchildren.

As household income rises, the likelihood of holding education debt for a child or grandchild increases. Only 2 percent of high-income people (earning $100,000 or more a year) over age 50 hold debt for their own education, but 13 percent of these high-income adults hold education debt for a child or grandchild.

There are differences by race, as well. Black adults over age 50 are roughly three times as likely to hold education debt for themselves as white adults over age 50. Conversely, white respondents in our sample are more likely to hold education debt for their children and grandchildren than black respondents.

View the methodology appendix here.

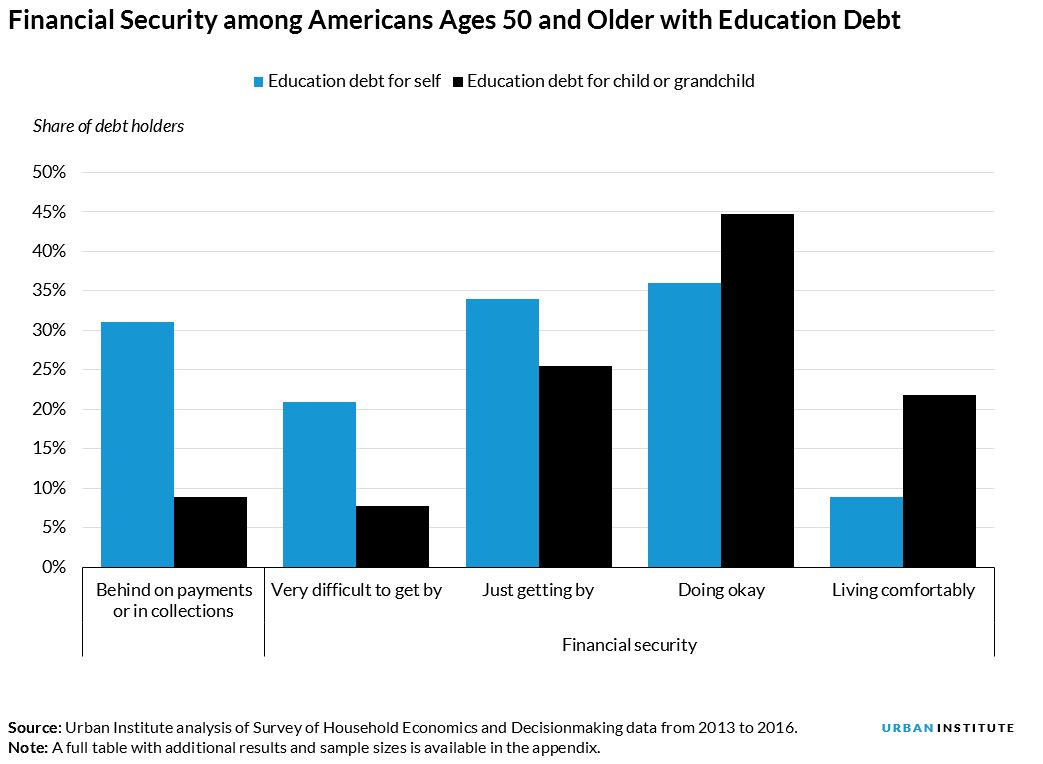

Older adults who hold debt for their children have different financial standing than those who hold debt for themselves. Fifty-five percent of those who owe money for their education after they reach age 50 report they find it “very difficult to get by” or that they are “just getting by.” In contrast, just 33 percent of those with debt for their children report that they are experiencing low or very low financial security.

Although most of this education debt is held as student loan debt, borrowers who have education debt for themselves are more likely to report holding at least some of this debt on a credit card. Those holding education debt on a credit card are likely paying higher interest rates than they would with a federal student loan, and they are losing out on borrower protections, such as income-based repayment.

Total debt amounts are similar among the two groups, but those who borrow for their children are more likely to report making higher monthly payments. Those who borrow for their children are also more likely to be current on payments. While 31 percent of older borrowers with debt for themselves are behind or in collections on payments, only 9 percent of those who borrow for their children or grandchildren are behind or in collections.

View the methodology appendix here.

Differences in financial stability among older borrowers may start at loan origination. For example, those who borrow for their children’s education from the federal government under the Parent PLUS program must not have an adverse credit history, but there are no credit checks for federal borrowers who need funds for their own education.

Student loan debt is different from other debt. It typically cannot be discharged in bankruptcy, and people who default on federal debt may have their wages garnished or have their earned income tax credit or Social Security benefits offset to pay off the debt. Our analysis shows that people who borrowed for themselves may be more at risk for these consequences and are generally more financially insecure than people who borrowed for their children or grandchildren.

Income-based repayment plans are available for federal borrowers who have debt for either their own education or for their children or grandchildren’s education (although the plan available to people borrowing for their children’s education is less generous and only available after consolidation). The data do not allow us to estimate the proportion of older Americans who use these plans, but the federal government should consider new ways to promote income-based repayment plans to older Americans, who may not be familiar with the options available.

Although the proportion of older Americans who owe money for education is small, policymakers should monitor the impact of education debt on older Americans, particularly for black borrowers and for borrowers who earn less than $20,000 a year. These people are more likely to hold education debt for themselves, rather than for their children or grandchildren. To support monitoring, the federal government should report student loan data disaggregated by loan type (e.g., Parent PLUS loans) and age, allowing for further understanding of the debt older Americans hold.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.