<p>Graduating students arrive for the Columbia University 2016 Commencement ceremony in New York, NY. Photo by Timothy A. Clary/AFP/Getty Images.</p>

A recent report from the US Department of Education’s Office of Inspector General indicates that enrollment in income-driven repayment (IDR) plans, which allow borrowers to repay student loans based on how much they earn, has increased substantially over the past five years. $51.5 billion of the student loan debt from the 2014–15 cohort of borrowers is being repaid through an IDR plan, compared with $7.1 billion from the 2010–11 cohort of borrowers. As more borrowers enroll in IDR, it is important to understand the demographics of those who use this program.

Income-driven repayment plans, which typically set payments at a given share of a borrower’s income and grant forgiveness after a set period, have been in place for several years but are frequently the subject of reform proposals from politicians on both sides of the aisle. The Urban Institute’s new data tool, Charting Student Loan Repayment, allows you to model the effects of different loan policies or design your own plan.

The costs of an IDR plan depend not only on the parameters, but also on who uses it. For example, borrowers with high debt and modest incomes entering IDR plans could have a higher amount of loan debt forgiven than borrowers with low debt and low incomes. Because the federal government absorbs the costs of unrepaid loans, knowing how the benefits of IDR are distributed is important.

To understand these dynamics, I use the 2016 Survey of Consumer Finances (SCF) to look at households that are paying off federal student loans through either an IDR plan or a non-IDR plan (i.e., a standard 10-year repayment, a graduated plan, or some other arrangement). I also include a third category: households that report having debt after attending school but are not making payments on the debt because of forbearance, enrollment in another debt forgiveness program, or self-reported inability to make payments.

Read the full methodology here

Of the households with federal debt surveyed in the SCF, 29 percent report making payments through IDR, 41 percent report making payments through a non-IDR plan, and 24 percent report that they are not enrolled and not making payments (6 percent report that they are in two or more categories).

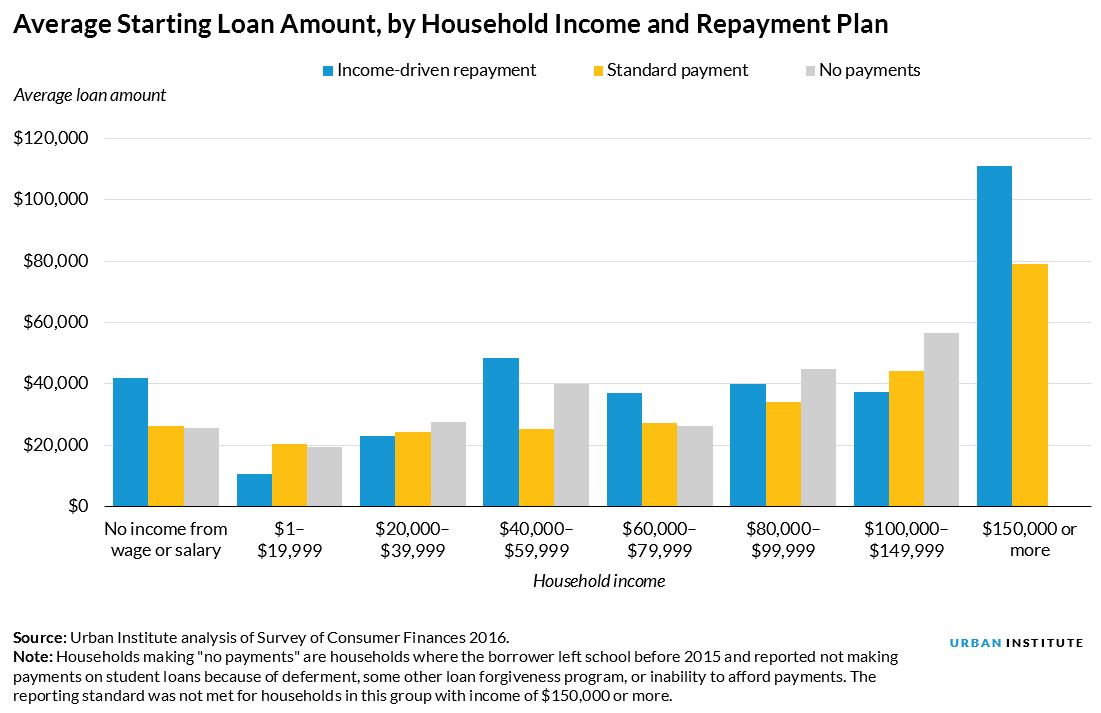

An examination of households with federal student loans by total household income (wage and salary) yields distinct patterns. As might be expected, households with low or modest incomes appear to use IDR repayment plans over non-IDR repayment plans. Some high-income households use IDR, but most are on standard or non-IDR plans. Those who report having loans but are not making payments tend to have low or no income from wages or salary.

Average starting student debt taken on by households in these categories indicates that loan size generally increases with current household income. Because IDR is designed to relieve the strain of high debt relative to income, we might expect borrowers on IDR plans to have higher starting student loan debt than those in a similar income bracket on non-IDR plans. But this is not universally true across our household income categories.

These finding are subject to caveats. Because the SCF is a snapshot of about 6,200 US households in 2016, I capture borrowers who have just entered repayment and those who have been in repayment for many years. Thus, the SCF sample is not representative of the decisions of new borrowers (i.e., those who have entered repayment for the first time). In general, IDR borrowers in my sample tend to be younger and have newer loans (59 percent in IDR plans had their most recent loan issued after 2009 versus 52 percent in non-IDR plans). Income-driven repayment borrowers were also less likely to have a spouse or partner in the household compared with non-IDR borrowers (60 percent had a partner versus 72 percent with no partner), which could result in lower overall household income.

My results reveal that most households using IDR to repay student debt make between $20,000 and $60,000 a year, but IDR is also used by those making substantially more. One concerning finding is the high number of low-income households that report being in forbearance or not making payments because of financial hardship. These borrowers would likely benefit from IDR but might not be aware of the program or know how to enroll.

As policymakers try again to redesign student loan repayment under IDR, understanding the borrowers who use the program is as important as the program’s structure. Policymakers will not only need to decide which borrowers are eligible for the program, but also how to ensure that those who need it most can access it.

Note: this post has been updated to show that 59 percent of borrowers in the sample had their most recent loan issued after 2009, not before.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.