<p>Photo by Monkey Business Images via Shutterstock.</p>

In 1977, Congress enacted the Community Reinvestment Act (CRA) to encourage lending where it was needed most. More than four decades later, the Office of the Comptroller of the Currency (OCC) is considering 1,485 comments on and suggestions for how CRA regulations should be modernized.

To support this effort and help ground it in evidence, we analyzed 2016 data about CRA lending and submitted these results as a comment letter to the OCC.

The modernization effort aims to promote transparency and consistency in reporting and examination requirements without imposing an undue regulatory burden. One way is to allow full public disclosure of the new Home Mortgage Disclosure Act (HMDA) data that began being collected and reported to regulators in 2018.

The new HMDA data could be particularly useful in understanding how banks are meeting communities’ multifamily lending needs.

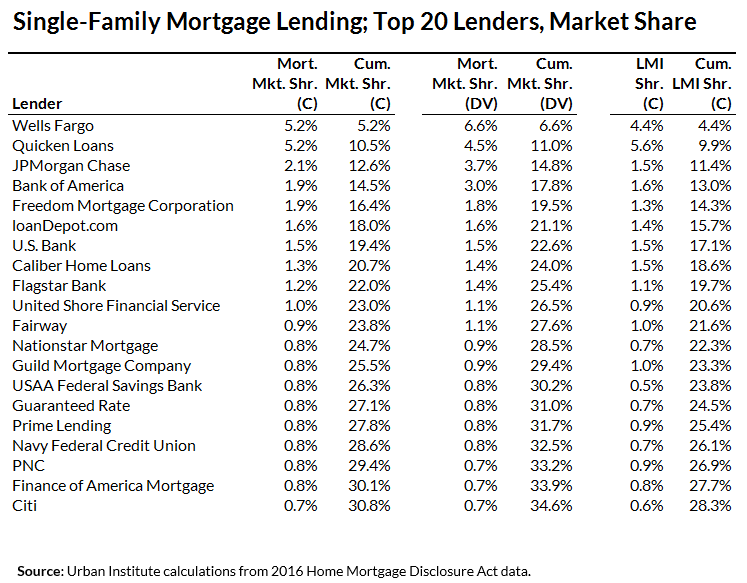

The concentration of single-family lending

As the first table shows, single-family lending is not very concentrated—many banks each make a relatively small portion of lending. The top single-family lender (by both loan count and dollar volume) is Wells Fargo, an institution subject to the CRA, with a 5.2 percent market share as measured by loan count and 6.6 percent as measured by dollar volume.

The second-largest lender is Quicken Loans, an institution not subject to the CRA (because it is not a depository institution), also with a 5.2 percent market share as measured by loan count.

So the top two institutions hold 10.5 percent of the market, and the top 20 lenders hold 30.8 percent of the market. The concentration for single-family low- and moderate-income (LMI) lending looks similar to single-family lending overall.

But to determine how well a bank serves its community, we need to look at its behavior in individual communities. The following table shows the same analysis for the 20 largest metropolitan statistical areas (MSAs).

The overall concentration at the MSA level is not much higher than at the national level. No single institution has more than a 20 percent market share in the top 20 MSAs. In several, a single institution has more than a 10 percent market share, usually because the institution is (or used to be) headquartered there (like Quicken in Detroit and Wells Fargo in San Francisco and Minneapolis).

Again, the LMI market share is similar to the overall market share. In the 75 MSAs we analyzed, the top lender in several markets (usually a bank headquartered in that market) had more than a 10 percent single-family market share. The lending share was more than 20 percent in only two MSAs: Banco Popular de Puerto Rico in San Juan, Puerto Rico, and GECU in El Paso, Texas.

The concentration of multifamily lending

The next table shows the same analysis for multifamily lending. At a national level, the largest lender, JPMorgan Chase, is an order of magnitude larger than the next largest lender, Wells Fargo, as measured by loan count, and is considerably larger, as measured by dollar volume.

JPMorgan Chase holds 18.8 percent of total multifamily lending by loan count, including 20.3 percent of all LMI multifamily lending. However, the rest of the market is relatively dispersed, with the top 20 market share at around 38 percent.

Although multifamily lending nationally is not particularly concentrated, except for JPMorgan Chase, multifamily lending tends to be dominated by a single lender in many MSAs.

The shaded boxes in the final table indicate MSAs where the top multifamily lender has more than a 20 percent market share. In 9 of the top 20 markets, the top lender has more than a 20 percent market share; in 3 of these markets, the top lender has more than a 40 percent market share. The numbers for LMI lending look very similar.

How can the enhanced HMDA data help?

Since 2018, HMDA has required lenders to collect and report data on the number of units in a multifamily property, as well as the number of income-restricted units.

But the Consumer Financial Protection Bureau now intends to publicly report only the number of units in the property in large ranges (5–24, 25–49, 50–99, 100–149, and 150+) and income-restricted units only as a percentage of total units.

This makes it difficult to use the data to understand the size and cost (and thus, potential rent) of units in properties with new multifamily loans and makes it impossible for those using public data to determine how many income-restricted units a property has. Anyone not in a regulatory agency who wants to understand how well a bank is serving its community won’t have access to the data they need.

The bottom line is that multifamily lending is more concentrated than single-family lending in individual communities, with the largest lenders making a disproportionate amount of loans. It is critical that these lenders play as important a role in LMI lending as they do in overall lending. The new HMDA data can give the market better information on the number of units—particularly income-restricted units—being created in LMI areas.

Making bank activities more transparent without imposing incremental regulatory burden isn’t easy, but publicly disseminating the new HMDA multifamily data would do just that. Why not use this information fully to promote transparency on multifamily CRA activity?

Related content:

- The Community Reinvestment Act Lending Data Highlights

- Most CRA-qualifying loans in low- and moderate-income areas go to middle- and upper-income borrowers

- While less plentiful, multifamily loans pack a bigger CRA punch than single-family loans

- Small business and community development lending are key to CRA compliance for most banks

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.