<p>Photo via Shutterstock.</p>

There has been a recent chorus of support for modernizing the regulations under the Community Reinvestment Act (CRA), and the Office of the Comptroller of the Currency (OCC) is considering 1,485 comments on how the regulations that implement the CRA should be modernized. To support this effort and ground it in solid evidence, we recently analyzed 2016 data about CRA lending and submitted these results as a comment letter to the OCC.

In two previous blog posts, we’ve highlighted important findings from our analysis:

First, small business lending and community development lending play an enormous role in helping most banks fulfill their CRA requirements.

Second, multifamily lending is much smaller than single-family lending, but plays a disproportionate role in both meeting the needs of low- and moderate- income (LMI) communities and in helping banks meet their CRA responsibilities.

This blog post highlights a third important point: 60 percent of CRA-qualifying loans in LMI census tracts are made to middle- and upper-income borrowers, including 29 percent to higher income borrowers. This suggests that those currently contemplating CRA modernization may want to consider giving less CRA “credit” for loans to higher income borrowers in lower income areas.

Banks get credit under the CRA for providing single-family mortgages to LMI borrowers and for making loans to borrowers in LMI census tracts, regardless of borrower income. Given the CRA’s focus on the LMI communities within which banks operate, it makes sense to give some CRA credit both for lending in LMI communities and for lending to LMI borrowers. But while lending to middle- and upper-income borrowers in LMI communities can encourage community diversity, it should not be the predominant form of single-family CRA lending.

Our research raises the question of whether these two types of lending should be treated interchangeably, as they are now.

Single-family lending is an important element in banks meeting their CRA requirements, ranking below small-business loans but ahead of all other types of lending.

Table 1 shows total single-family (one to four units) lending nationally, as well as by banks (subject to the CRA) and nonbanks.

Thirty percent of loans by loan count were considered LMI, with 21 percent made to LMI borrowers and 14 percent to LMI areas. (The sum of LMI borrowers plus LMI areas is more than the total because some loans are in both categories.) Thus, there are more loans made to LMI borrowers than to LMI areas.

But when we look at the value, the figures are more equal. The dollar volume of LMI lending is 20 percent, with 12 percent to LMI borrowers and 11 percent to LMI areas. The volumes are more similar because the average loan size for LMI lending is $159,000 and includes loans averaging $134,000 to LMI borrowers and $183,000 to borrowers in LMI areas.

When we compare banks and nonbanks, we find that banks do less LMI lending. The share of bank lending to LMI borrowers is 16 percent by dollar volume compared with 23 percent for nonbank lenders. In a previous blog post, we showed that this was because banks make far fewer Federal Housing Administration loans, which are heavily LMI. But the numbers in table 1 show a consistent pattern for banks and nonbanks. Both make more loans to LMI borrowers than to LMI areas, but the dollar volumes are not that different, as the loans to LMI borrowers are smaller than the loans in LMI areas.

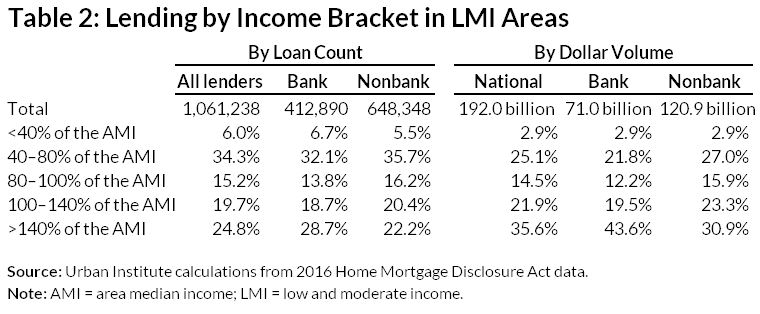

So who is borrowing within LMI areas? Table 2 shows that loans to LMI borrowers (those earning less than 80 percent of the area median income, or AMI) are about 40 percent of the total loans in LMI areas. Another 15 percent of loans go to borrowers earning between 80 and 100 percent of the AMI, and the remaining 45 percent are to borrowers earning more than the AMI.

If we look at the results by dollar volume, we find that about 28 percent of the dollar volume of loans to LMI areas goes to LMI borrowers, 15 percent goes to borrowers earning between 80 and 100 percent of the AMI, and the remaining 58 percent goes to borrowers with incomes greater than the AMI. These numbers are similar for banks and nonbanks. But 44 percent of banks’ lending, by dollar volume, went to borrowers with incomes above 140 percent of the AMI, significantly higher than the 31 percent of nonbanks’ lending.

In many cases, the income information is missing from this analysis. We have allocated missing values proportionately between the categories. In actuality, the analysis of average loan size shown in table 3 shows that the missing values are more apt to be loans to high-income people, so the analysis in table 2 may actually overstate the LMI borrower share.

There are good reasons for counting loans made to LMI census tracts as qualifying for CRA compliance. Not only is geography the historic basis of the CRA, but such lending encourages income diversity in lower income tracts. But 60 percent of the dollar value of loans in LMI census tracts is not going to LMI borrowers.

That may be fine in the aggregate, but examiners should look at individual bank behavior to make sure individual institutions are not overly reliant on this type of lending to meet their CRA responsibilities. That is, examiners should make sure that institutions are not solely skimming the larger, more profitable loans in gentrifying areas to “count” toward CRA requirements.

Moreover, when contemplating CRA modernization, this analysis raises the question of whether one wants to account for the pattern we have found by giving less CRA “credit” for loans to higher income borrowers in lower income areas.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.