<p>Alanna McCargo, Vice President of Urban Institute's Housing Finance Policy Center, speaks at the National Fair Housing Alliance’s National Access to Credit Forum. Photo by Robert Abare/Urban Institute.</p>

Owning a home helps families build wealth and is often financially better than renting, but homeownership remains out of reach for too many Americans. This problem is inextricably tied to Americans’ inability to access mortgage credit. Consider these statistics:

- 45 million consumers are “credit invisible”: Over 26 million adults lack a credit history from a major credit bureau, and another 19 million have credit history considered unscorable. Credit scores are critical to obtaining mortgage credit at a fair price.

- All gains in the black homeownership rate since the 1968 Fair Housing Act have been erased.

Urban’s Vice President for Housing Finance Policy Alanna McCargo presented these points in a recent panel discussion at the National Fair Housing Alliance’s (NFHA’s) National Access to Credit Forum, which commemorated the 50 years since the Fair Housing Act became law.

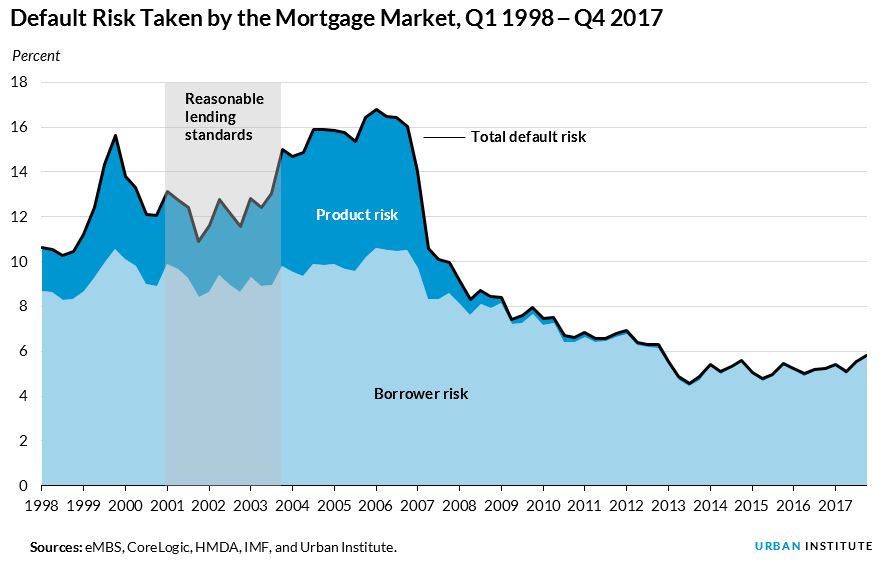

McCargo noted how, since the response to the 2008 housing crisis, lending standards have remained too tight. “Between 2009 and 2015, 6.3 million borrowers who could have obtained loans under reasonable lending standards were not served,” she said.

Larry Parks, senior vice president of the Federal Home Loan Bank Board, noted that the NFHA’s forum was held the day before the 50th anniversary of the 1968 riots in the District of Columbia, which resulted from the disenfranchisement of the black community. “How do we address this gap in homeownership that has been around since the sixties, and is still here today?” he asked.

Similarly, senior economist at Trulia Cheryl Young discussed her organization’s research on the importance of place, which found that majority-black areas have 33 percent fewer traditional financial service establishments than majority-white areas. In Houston, this disparity is particularly stark: majority-white areas have over 2.5 times such establishments as majority-black areas.

Discussing expanding access to mortgage credit, Moody’s chief economist Mark Zandi said, “It would be a huge error to stay where we are,” and described the current system’s approach to credit expansion as “very opaque, very hard to measure, and not as effective as it should be.”

How do we expand access to credit?

In a subsequent discussion on the role of the Federal Housing Administration (FHA), Urban’s Vice President for Housing Finance Policy Laurie Goodman pointed out the FHA’s critical support of low-income homebuyers.

“The FHA really does serve the underserved,” she said. “FHA borrowers, on average, are much more heavily minority, are far more likely to be first-time home buyers, and have much lower incomes than conventional borrowers. The bottom line is that the FHA puts homeownership in reach for many who would not otherwise be able to own a home, and homeownership remains the best way to build wealth.”

Dave Stevens, president and CEO of the Mortgage Bankers Association, pointed to a lack of certainty in the loan origination process as a key obstacle to expanding access to credit for the FHA.

Stevens said there is a lack of clarity surrounding defects in loans and what constitutes a defect severe enough to pursue the most extreme remedies, such as indemnification or enforcement of the False Claims Act. “This creates an outcome where lenders want to pull back from using the full extent of the FHA credit box,” he said.

Stevens also stressed the importance of the FHA’s “taxonomy” of defaults and defects, which ranks errors in loan files and how lenders should be held accountable in different situations.

“There’s going to be some form of error in almost every loan file, if you search for one,” Stevens said. “The problem is, the way the rules are written today, the Department of Justice doesn’t distinguish between what is and is not significant.”

Stevens noted that the FHA has built a default and defect taxonomy, but it has yet to be implemented and does not include remedies. This taxonomy could be tied to the False Claims Act, where only the most serious errors are subject to it.

Mike Calhoun, president and CEO of the Center for Responsible Lending, also pointed out that the FHA needs more resources to fulfill its mission. “They are already running on a shoestring budget,” he said. Calhoun stressed that the FHA needs adequate funding to create innovative products and support underserved communities in new ways.

These solutions are a small part of a much larger picture. The discussion at the NFHA forum revealed that to help more Americans benefit from homeownership, our policies need to innovate, adapt, and become more inclusive.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.