Part of a series of civil rights laws, the Community Reinvestment Act (CRA) was passed in 1977 to fight explicitly racist redlining policies. The CRA requires federal bank regulators—the Office of the Comptroller of the Currency, the Federal Reserve, and the Federal Deposit Insurance Corporation—to evaluate the performance of banks and thrifts to determine how well each meets “the credit needs of its entire community, including low- and moderate-income neighborhoods.” Independent mortgage banks and credit unions—or nonbanks—are not subject to the CRA.

Federal banking regulators are considering revisions to the CRA, and one issue they have raised is whether and how the regulations should explicitly take race into account, given the CRA’s genesis and purpose.

Although current CRA regulations do not consider race, data collected under the Home Mortgage Disclosure Act (HMDA) include information about home mortgage borrowers’ race or ethnicity, allowing us to examine how well banks perform in lending to borrowers of color relative to the nonbanks not subject to the CRA.

Based on an analysis of mortgage loans made to owner-occupant home purchasers, we find that banks substantially underperformed nonbanks in serving borrowers and neighborhoods of color.

This shortfall is partially attributable to the fact that banks make fewer Federal Housing Administration (FHA) loans, and government channels tend to lend more frequently to borrowers of color. But this is not the whole story. Our analysis shows banks make a lower proportion of their loans to neighborhoods and borrowers of color through both government and conventional lending channels.

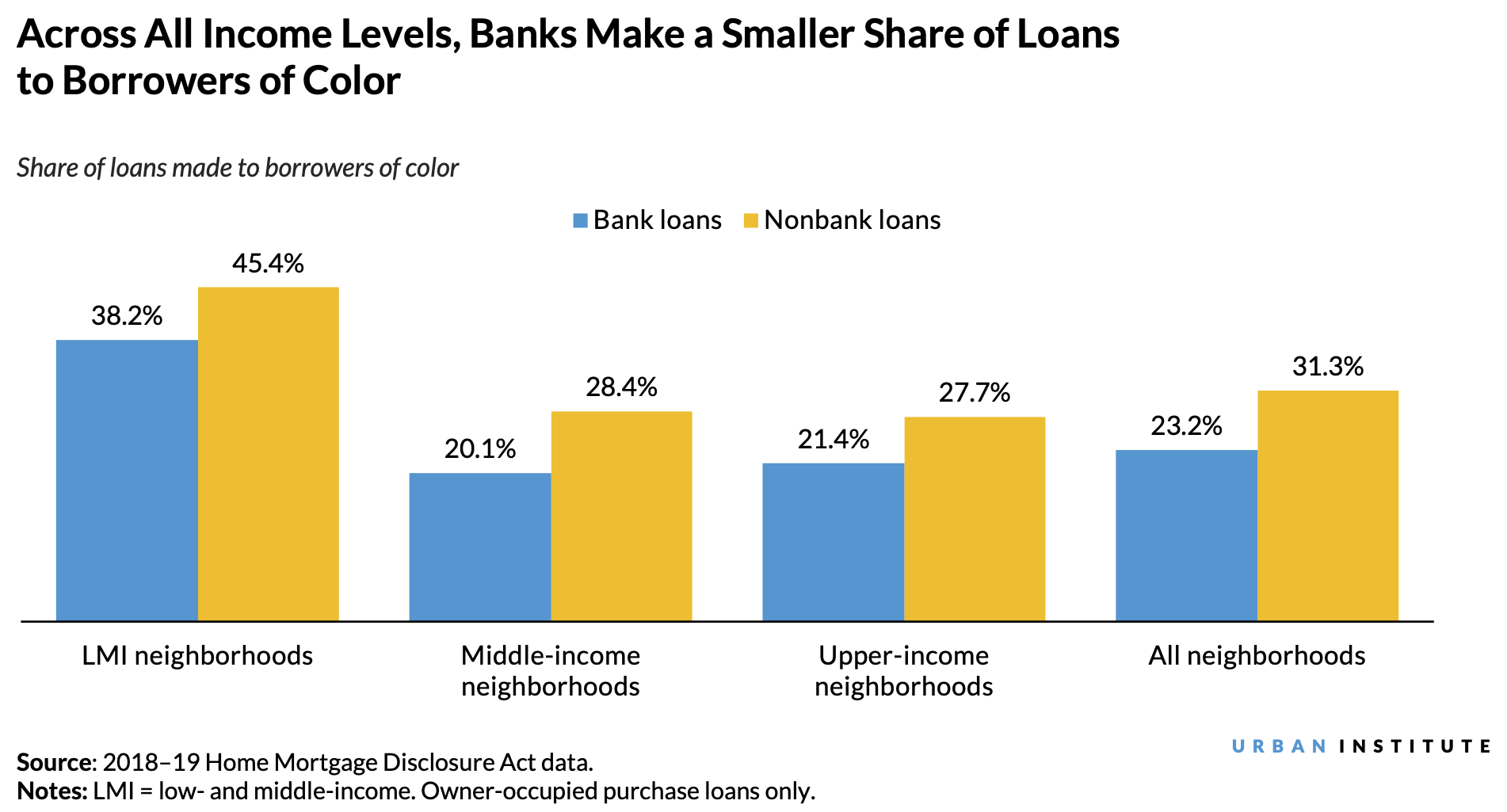

Compared with nonbanks, banks consistently make a smaller share of loans to borrowers and neighborhoods of color

Using 2018–19 HMDA data, we found that banks made a lower proportion of loans to borrowers of color—those who identify as Black, Hispanic, Asian, or another nonwhite race. Overall, banks made 23.2 percent of their owner-occupant home purchase mortgage loans to borrowers of color, compared with 31.3 percent for nonbanks.

We also broke down the results by neighborhood income level. A low- and moderate-income (LMI) neighborhood is a census tract with a median income up to 80 percent of the area median income, a middle-income neighborhood has a median income between 80 and 120 percent of the area median income, and an upper-income neighborhood has a median income greater than 120 percent of the area median income.

In LMI neighborhoods, 43.5 percent of homeowners are homeowners of color, and homebuyers of color receive 45.4 percent of nonbank loans in these neighborhoods. Bank loans to homebuyers of color in 2018 and 2019 compose only 38.2 percent of bank lending in those neighborhoods—a 7.2 percentage-point difference.

This racial lending gap continues up the income ladder. In middle-income neighborhoods, banks lagged nonbanks by 8.3 percentage points; in upper-income neighborhoods, the gap between banks and nonbanks is 6.3 percentage points.

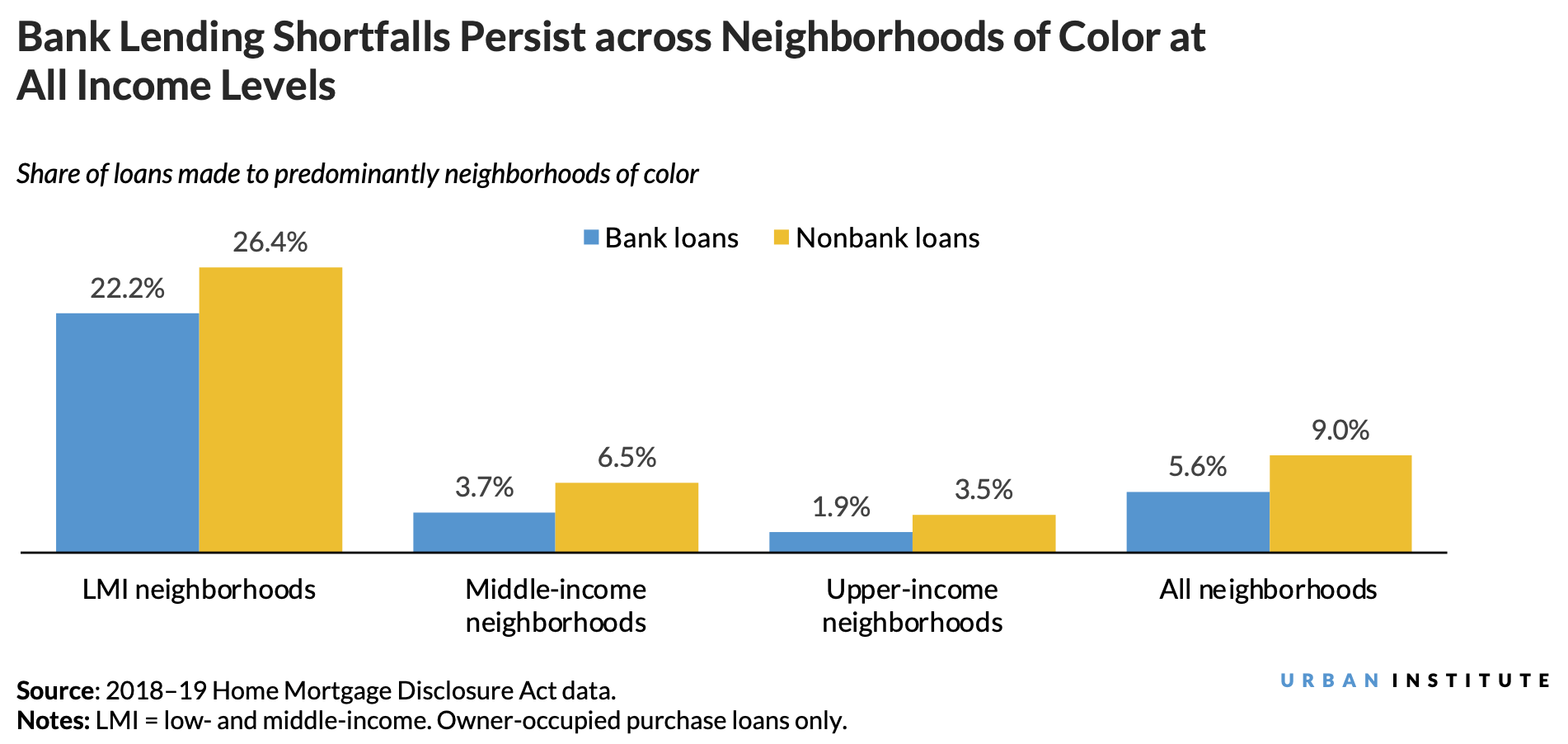

Next, we examined owner-occupied purchase lending in neighborhoods where more than 70 percent of households are people of color, using 2015–19 American Community Survey data. It’s important to note that lending to LMI neighborhoods is not the same as lending to neighborhoods of color. Indeed, only 40 percent of LMI neighborhoods are predominately residents of color.

Again, we find disparities between banks and nonbanks: 5.6 percent of bank loans were made in neighborhoods of color in 2018 and 2019, compared with 9 percent of nonbank loans.

The gap is particularly strong in communities that are both LMI and neighborhoods predominantly of color: 22.2 percent of bank loans in LMI neighborhoods were made in neighborhoods of color, compared with 26.4 percent of nonbank loans in LMI neighborhoods of color.

Why do banks lag behind?

Banks make fewer mortgage loans through government channels (21 percent) than nonbanks (39 percent), which can partially explain the shortfalls. This is important because overall, government channels are significantly skewed toward lending to borrowers of color, as government loans tend to allow for more risk layering—a wider combination of lower credit scores, higher debt-to-income ratios and higher loan-to-value ratios.

But again, this is not the whole story. Within each government and conventional channel, banks make a disproportionately lower share of loans to neighborhoods and borrowers of color. We find that banks make 7.2 percent of their government loans and 5.2 percent of their conventional loans to neighborhoods of color, compared with 11.7 percent and 7.3 percent, respectively, for nonbanks.

The data on borrowers of color reveal similar patterns. In government channels, banks make 28.6 percent of their government loans to these borrowers; for nonbanks, the share is 37.8 percent.

In both government and conventional channels, banks make proportionally fewer loans to LMI neighborhoods of color and borrowers than nonbanks, largely because, within each channel, banks have a narrower credit box. Although bank and nonbank loans tend to have similar loan-to-value ratios, bank loans tend to have higher average credit scores and lower average debt-to-income ratios.

Banks Originate Fewer Loans to Neighborhoods and Borrowers of Color through Conventional and Government Channels

|

|

Government channel |

Conventional channel |

|||

|

|

Banks |

Nonbanks |

Banks |

Nonbanks |

|

|

Share of loans to neighborhoods of color |

7.2% |

11.7% |

5.2% |

7.3% |

|

|

Share of loans to LMI neighborhoods of color |

4.2% |

6.3% |

2.9% |

3.9% |

|

|

Share of loans to borrowers of color |

28.6% |

37.8% |

21.8% |

27.1% |

|

|

Share of loans to LMI borrowers of color |

11.7% |

14.2% |

6.7% |

8.6% |

|

Source: 2018–19 Home Mortgage Disclosure Act data.

Notes: LMI = low- and middle-income. Data reflect owner-occupied purchase loans.

One factor driving these gaps is that bank lenders have become much more risk averse since the mortgage crisis and Great Recession. The bank share of the mortgage market has steadily decreased since 2013; banks currently account for about 25 percent of total mortgage lending.

Many banks exhibit their risk aversion by imposing underwriting overlays (higher minimum credit scores, lower maximum debt-to-income ratios) that narrow the FHA and government-sponsored enterprises’ (GSEs’) credit boxes and make it more difficult for borrowers without pristine credit to secure a loan.

These overlays disproportionately affect neighborhoods and borrowers of color, as the legacies and ongoing effects of structural racism have contributed to lower credit scores and higher debt-to-income ratios among Black and Hispanic borrowers. Credit data and a measure of debt to income are important inputs into the automated underwriting systems used by the government-guaranteed entities and GSEs.

Whatever regulators decide about explicitly considering race under the CRA, banks can do more to help close racial homeownership gaps and help communities of color tap into the wealth-building power of homeownership. By putting the Great Recession behind them, banks can better serve a new, more diverse group of homeowners by participating fully in the FHA market and lending to the complete extent of the GSE and FHA credit boxes by eliminating overlays on credit scores and debt-to-income ratios.

The Urban Institute has the evidence to show what it will take to create a society where everyone has a fair shot at achieving their vision of success.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.