The challenges faced by students of color—particularly black students (PDF)—in higher education have roots in our nation’s racist history, from slavery to Jim Crow to redlining. A prime legacy of this history is the large wealth gap between black and white Americans—and this gap helps explain both why black students borrow more for college on average and why doing so is especially risky.

This issue is garnering well deserved attention from Senators Doug Jones, Elizabeth Warren, Kamala Harris, and Catherine Cortez Masto, who recently issued a call for information (PDF) “on how to address racial disparities in student debt and the broader challenges faced by students of color.”

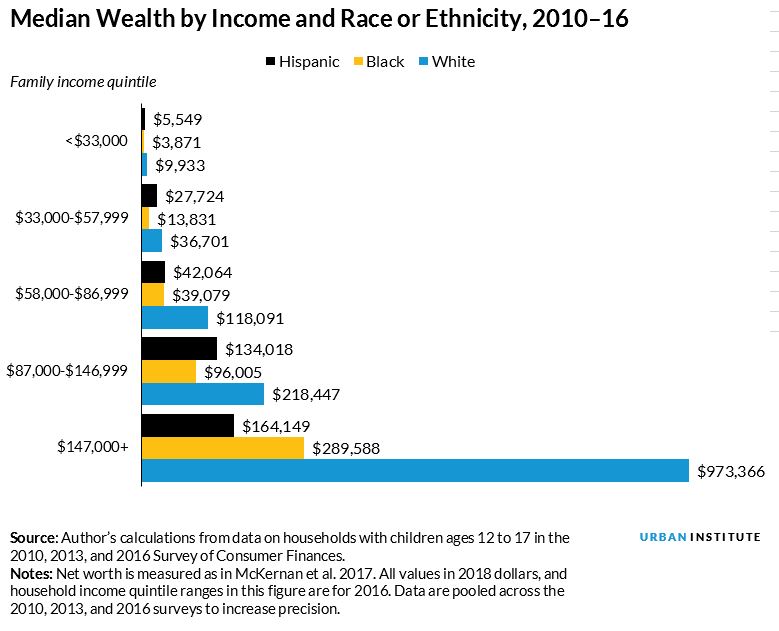

Wealth gaps increase with income

Racial and ethnic disparities in wealth are well documented, with 2016 data showing the median white family having nearly 10 times as much wealth as the median black family. (The gap between white and Hispanic families is similar in size.) This means students of color tend to have fewer family assets to draw on for college, often leading them to choose between attending lower-priced institutions or taking on more debt. After leaving college, students of color are less likely to be able to lean on family members for financial support that might ease the burden of loan repayment.

Higher education policy research tends to focus more on income than wealth, not because income is more important, but because it is easier to measure. The quadrennial National Postsecondary Student Aid Survey collects income data on a nationally representative group of college students, but it only collects limited information on wealth.

The available data indicate income is a poor proxy for wealth, especially for black and Hispanic families. The typical low-income family has less than $10,000 in net worth, regardless of race or ethnicity. But racial and ethnic disparities in wealth grow with income, as the figure below shows. The typical middle-income white family has roughly three times the wealth of the typical middle-income black or Hispanic family.

Racial and ethnic differences in student borrowing persist across income levels

How wealth gaps translate into student borrowing is not uniform across groups. Black students are more likely to borrow than white students in every income group. (Average amounts among borrowers are similar, at around $6,000.) And these data likely understate black-white differences in education debt, as they only capture borrowing in a single year.

The lower average wealth among black families might explain some of the difference in borrowing between black and white students, especially among middle- and high-income families. (Low-income families of all races and ethnicities tend to have few assets.) And research shows that proxies for wealth, such as homeownership and parents’ education levels, are associated with the likelihood of default.

Hispanic students are less likely to borrow than white students at every income level, despite coming from families with less wealth (although Hispanic families have higher average income and wealth (PDF) than black families). Potential explanations include the greater rates at which Hispanic students enroll (PDF) in lower-cost community colleges and higher average levels of loan aversion. At community colleges, 22 percent of students are Hispanic and 14 percent are black, but at for-profit colleges the pattern is reversed: 15 percent of students are Hispanic and 25 percent are black. This pattern might explain why low-income black families are more likely to borrow than other low-income students.

Borrowing by parents is highest among high-income and black families

Undergraduate student borrowing is constrained by loan limits that vary between $5,500 and $7,500 per year for students who are financially dependent on their parents. But parents can take on their own debt through the PLUS program, which has no limits other than the total cost of attending college.

Gaps in borrowing rates between the parents of black and white students persist across income levels. (Once again, Hispanic families are less likely to borrow than white families.) Amounts borrowed are similar across races and ethnicities within income levels but increase with income from about $10,000 among the lowest-income borrowers to about $20,000 among the highest income borrowers. The greater propensity of black parents to borrow likely reflects their lower average access to wealth, both in liquid assets that can be drawn on directly and in home equity that can be borrowed against.

What do wealth and borrowing gaps means for federal student aid policy?

Student debt is not inherently bad; a recent study found that taking on debt can increase the likelihood that students succeed. But students take on risk when they take on debt, and that risk is greater if they cannot turn to relatives for help.

Making student loan payments income-based and automatic would help by exempting low-income borrowers from making payments without having to file any paperwork. Given that black students borrow more and have lower average lifetime earnings, a universal income-based repayment system with forgiveness could narrow the black-white gap in default rates—and perhaps the wealth gap.

But federal policymakers might want to go further and reduce the amount of debt that students of color need to take on to pursue higher education in the first place.

Congress could increase the generosity of the Pell grant program, reducing the need for borrowing among low-income students, most of whom come from families with little or no wealth. This could narrow racial and ethnic differences in borrowing—given the correlation between income and race and ethnicity—but it would not provide additional support to students from low-wealth families with higher incomes.

To address that gap, Congress could design a grant program targeting grant funds based on family wealth. This could be difficult because it would require information on assets that would be costly to collect and difficult to verify. Recent higher education policy efforts have focused on simplifying the federal aid application process, not complicating it.

Congress could direct funding to institutions to reduce the prices paid by students of color. Broad-based “free college” programs would be an expensive way to accomplish this goal and would be unlikely to narrow racial and ethnic wealth gaps because they would benefit all racial and ethnic groups—and poorly designed programs could widen gaps.

An alternative would be targeted support to institutions that enroll large numbers of students of color—such as community colleges, historically black colleges and universities, and Hispanic-serving institutions—through a tailored grant program or through direct support to institutions with a track record of producing good outcomes for students of color.

These trade-offs highlight the limitations of using race-neutral policies to address the effects of centuries of racist policies. Grant and loan programs on their own are unlikely to make a large dent in the racial and ethnic wealth gap, even as these programs promote upward mobility by enabling more students to enroll in and complete college. But understanding these wealth gaps is critical to designing higher education policies that do more good than harm for students of color.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.