<p> </p>

<p>(Ying Liu / 500px/Getty Images)<br />

</p>

Despite historically low interest rates, not everyone can access capital to buy or fix a home or switch to a lower-interest loan. According to the most recent Home Mortgage Disclosure Act (HMDA) data, 16.1 percent of all mortgage applications in 2020 were denied. Of those denials, Black borrowers had the highest denial rate (27.1 percent), whereas white borrowers had the lowest (13.6 percent).

The simplest way to calculate mortgage denial rates is to divide all denied loans by total loan applications. But breaking out different types of mortgages to calculate the most relevant denial rates reveals often-overlooked racial disparities in the mortgage market.

Using other methods of calculating denial rates can help researchers uncover more details about who is denied for what loans and why and can inform strategies to increase homeownership, make it more affordable, and make home improvement and home equity extraction easier and safer.

Mortgage denial rates vary by loan purpose

In 2020, HMDA data show home improvement loan applications had the highest denial rate (38.8 percent). Though they’re more likely to live in older homes, more than half of Black (63.0 percent) and Hispanic (56.6 percent) home improvement applicants were denied loans to make necessary repairs and renovations.

Compared with white and Asian borrowers, Black and Hispanic borrowers were also significantly more likely to be denied home purchasing loans and refinancing loans for existing mortgages that would allow them to take advantage of historically low interest rates. The denial rate was also high for cash-out refinances, particularly for Black and Hispanic households. This suggests that even with sufficient home equity from the recent rise in home prices, homeowners of color face greater barriers to extracting cash from their housing wealth when needed.

More differences within home purchase loans

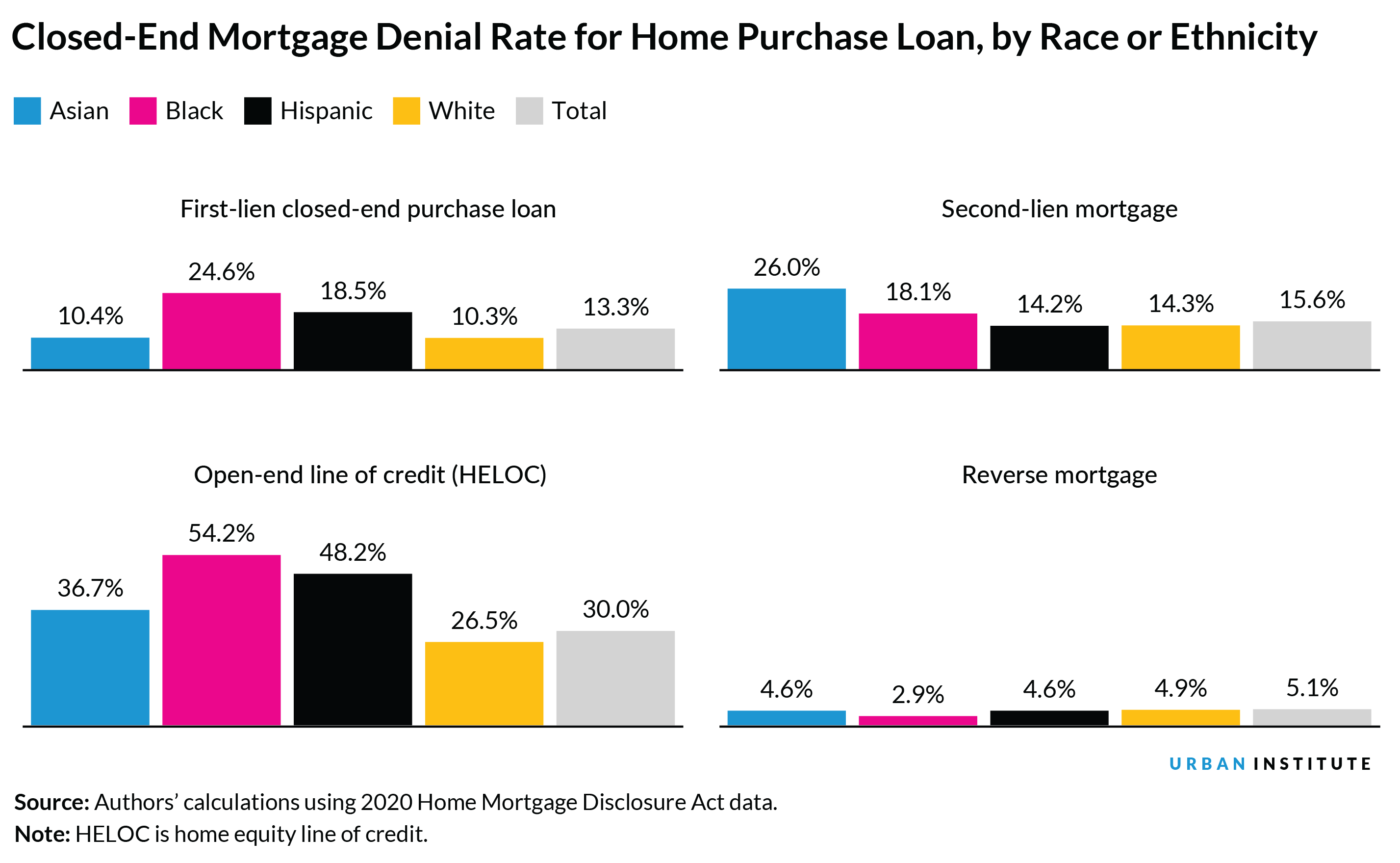

In the HMDA data, the home purchase loan includes both home equity lines of credit (HELOCs) and reverse mortgages, and it includes second-lien mortgages if the borrower is using piggyback loans. To determine the denial rate of purchase loans, researchers should first remove HELOCs and reverse mortgage loans from the data. Then, to focus on first-lien mortgages, researchers would remove second-lien mortgages.

This step is crucial because the denial rate for HELOCs (30 percent) is more than double the denial rate of first-lien closed-end purchase loans (13.3 percent).

The denial rate for HELOCs is especially high for Black (54.2 percent) and Hispanic (48.2 percent) borrowers, again showing that these borrowers face greater challenges tapping into home equity. Second-lien applications are most likely to be denied among Asian borrowers (26 percent).

Including these categories, the purchase denial rate is 13.4 percent, 0.1 percentage points higher than the rate for first-lien closed purchase loans. Though the overall difference is minor, differences for Asian and Hispanic borrowers are slightly larger.

Denial rates also differ by property and occupancy types

Researchers could further divide home purchase loans by occupancy and property types. The denial rate differs by whether the property is a primary or secondary residence or investment property and by the type of property.

For Black and white borrowers, mortgages for primary residences had a slightly higher denial rate than mortgages for secondary residences and investment properties. Among Asian borrowers, the denial rate was highest for secondary residences (12.5 percent). For Hispanic borrowers, investment properties had the highest denial rate (19.3 percent).

Manufactured homes had substantially higher denial rates than one-to-four-unit homes across racial and ethnic groups, and denial rates were even higher for loans not secured by land. For Black borrowers, more than 75 percent of applications for manufactured homes were denied in 2020, even of those secured by land.

Mortgage Denial Rates for Types of Home Purchase Loans, by Race and Ethnicity, 2020

| Asian | Black | Hispanic | White | Total |

| Occupancy type | |||||

| Primary residence | 10.2% | 24.7% | 18.5% | 10.4% | 13.5% |

| Secondary residence | 12.5% | 23.6% | 17.1% | 8.2% | 9.9% |

| Investment property | 11.2% | 22.4% | 19.3% | 10.3% | 12.7% |

| Property type | |||||

| One-to-four-units | 10.1% | 18.8% | 14.0% | 7.6% | 10.1% |

| Manufactured homes | 52.4% | 75.5% | 64.8% | 50.9% | 57.6% |

| Secured by land | 39.8% | 76.4% | 52.1% | 41.0% | 47.9% |

| Not secured by land (Chattel loans) | 58.5% | 75.2% | 69.8% | 59.8% | 64.4% |

Source: Authors’ calculations using 2020 Home Mortgage Disclosure Act data.

Notes: Analysis includes closed-end first-lien home purchase loans only.

Do withdrawn or incomplete applications or preapproval denials count toward the denial rate?

When calculating the denial rate, researchers usually remove applications withdrawn by the borrower or closed because of an incomplete file. Though these applications are technically not denied by the lender, they nevertheless failed to result in financing. This could be the applicant’s decision, but it could also represent a “soft" denial.

Data show Asian (16.2 percent) and Black (15.0 percent) applicants are more likely to withdraw mortgage applications, and Hispanic (3.6 percent) and Black (3.8 percent) applicants are more likely to have files closed for incompleteness.

More research is needed to determine why these potential borrowers did not complete their applications and what supports they need to reach the finish line. Housing counseling, for example, could help some complete the application process.

Some researchers also exclude loans denied at the preapproval stage, though others include them in their calculations. Though we include the preapproval denials here, dropping them would slightly lower the denial rate for home purchase loans.

In a conversation with Consumer Financial Protection Bureau researchers, we learned the bureau does not have a common standard for denial rate calculations and methods differ according to the research purpose, but its annual report on the HMDA data excludes preapproval denials.

Addressing Loans Taken Out of Applications and Preapproval Denials

| Asian | Black | Hispanic | White | Total |

Percent of applications taken out of the denial rate calculation | |||||

| Application withdrawn by applicant | 16.2% | 15.0% | 14.3% | 12.8% | 12.4% |

| File closed for incompleteness | 2.8% | 3.8% | 3.6% | 2.4% | 2.5% |

Denial rate comparison including and excluding preapproval denials | |||||

| Denial rate excluding preapproval denials | 10.0% | 23.6% | 17.7% | 9.7% | 12.6% |

| Denial rate including preapproval denials | 10.4% | 24.6% | 18.5% | 10.3% | 13.3% |

Source: Authors’ calculations using 2020 Home Mortgage Disclosure Act data.

Notes: Analysis includes closed-end first-lien home purchase loans only. Among total loans, the data show a lower share of applicants withdraw their applications and have their files closed for incompleteness because a greater share of loans directly sold to financial institutions do not have race and ethnicity information.

What do we do with this information?

Researchers can learn much more about the nuances of the mortgage market by digging further into the denial rate. When presenting denial rates, researchers should clearly state what is—and what is not—included in their calculations. Though we observed that denial rates are higher for Black and Hispanic borrowers, the size of the gap varies significantly.

By identifying specific disparities and their causes, researchers and decisionmakers can develop strategies to help more people get over these financing barriers, address the legacies of racist policies and practices, and tap into the security and wealth-building power of homeownership.

The Urban Institute has the evidence to show what it will take to create a society where everyone has a fair shot at achieving their vision of success.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.