<p>Ed Freeman/Getty Images</p>

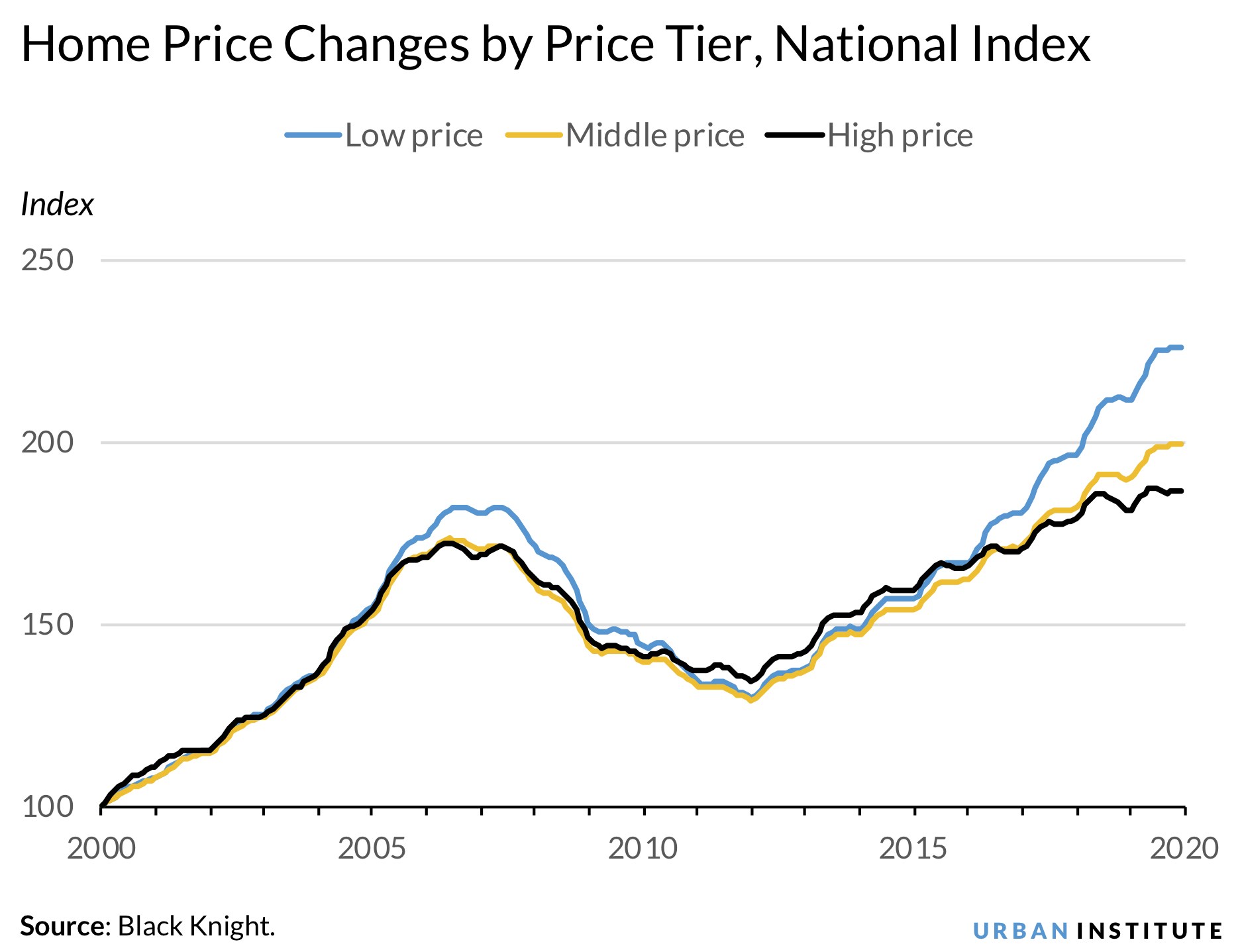

Before the COVID-19 outbreak, the affordability crisis driven by the lack of housing supply was one of the biggest problems facing the US housing market. Our recent report finds that prices for homes in the bottom 20th percentile of the distribution (low-price homes) increased 126 percent between January 2000 and December 2019. This is a substantially larger increase than the 87 percent increase for homes in the top 20th percentile of the distribution (high-price homes).

A closer look at 285 metropolitan statistical areas (MSAs) suggests that rapid employment growth combined with increased supply constraints from zoning and other regulations contributed to this disproportionate price growth for low-price homes. If left unaddressed, these same supply constraints will hamper the ability of low-income households to prosper as we emerge from the crisis and will exacerbate income inequality.

Supply constraints are associated with faster price appreciation for low-price homes

Home price appreciation varies significantly across MSAs. For example, the prices of low-price homes in Los Angeles increased 313 percent between 2000 and 2019 but declined 5 percent in Detroit. Prices for high-price homes showed the greatest increase in San Francisco (190 percent), while Saginaw, Michigan, showed the smallest increase (42 percent). We examined the factors associated with higher appreciation for low-price homes relative to high-price homes and found the following:

- MSAs with greater supply constraints—measured using the Wharton Residential Land Use Regulatory Index, the Saiz Land Unavailable Index (which measures the share of land unavailable for development), and changes in the number of housing units—experienced higher price growth for low-price homes relative to high-price homes.

- MSAs with a larger number of employed people in 2000 and higher employment growth, two variables that reflect housing demand, experienced a greater increase in low-price home prices than in high-price home prices.

Faster appreciation for low-price homes has exacerbated income inequality

The faster rise in low-price home prices hits low-income homeowners and renters the hardest, specifically those in the bottom quartile of the income distribution. As low-price home prices rise, would-be homebuyers with low incomes have trouble finding affordable homes, so they remain in the rental market, drive up rents, and increase the demand for and price of rental properties. As a result, the cost for both owning and renting has gone up substantially for low-income households, while their income growth has not kept pace with that of high-income households (those in the top quartile of the income distribution).

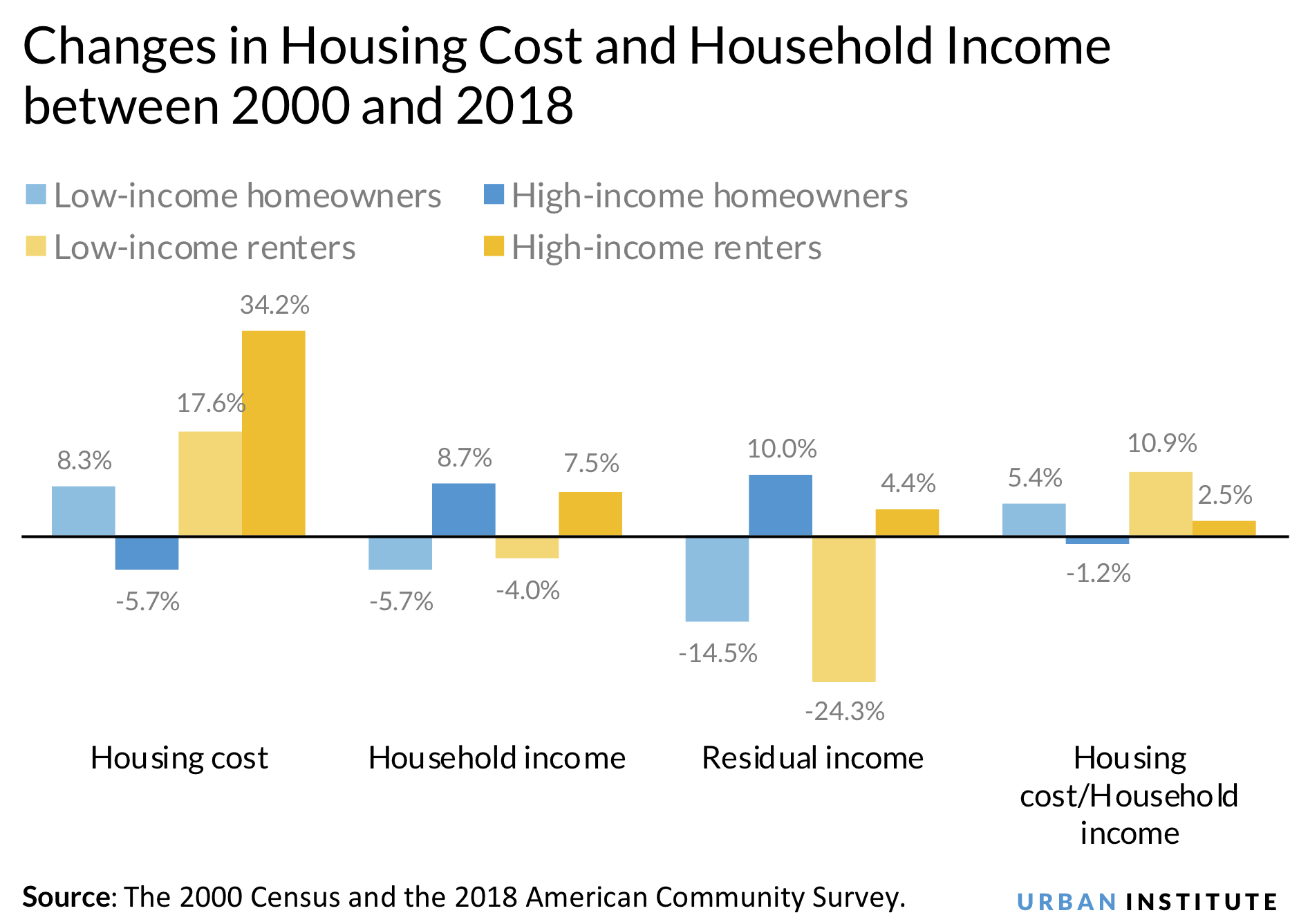

Between 2000 and 2018, housing costs increased for low-income homeowners and low- and high-income renters, while housing costs dropped 5.7 percent for high-income homeowners. These high-income homeowners also experienced the greatest increase in income, which led to a 10 percent increase in their residual income (household income minus housing costs) and a 1.2 percent drop in their housing cost burden (the ratio of housing costs to income).

Meanwhile, the residual income of low-income homeowners and renters dropped 14.5 percent and 24.3 percent, and their housing cost burden increased 5.4 percent and 10.9 percent, respectively. Although housing cost growth was highest for high-income renters, their growth in household income largely compensated for the increase in cost.

Overall, low-income renters and homeowners, whose incomes did not fully recover after the Great Recession, had 24 and 15 percent less residual income, respectively, in 2018 than they did in 2000, while high-income renters and homeowners had 4 and 10 percent more, respectively.

What will happen after the COVID-19 crisis?

Despite the labor market turmoil caused by COVID-19, home prices have largely remained where they were before the pandemic, as demand and supply shrank simultaneously. But with rising unemployment and forbearance, lenders have tightened credit to avoid taking greater risks that may further strain their financial capacity.

Credit was already tight before COVID-19, and because of these even stricter standards, low-income households will likely face greater difficulty accessing homeownership, even for homes within their financial reach. It’s likely that those with high incomes and credit scores will have more opportunities to buy homes and build housing wealth as the economy recovers from the COVID-19 shock.

Additionally, a greater share of low-income homeowners and renters (PDF) are working in industries that are more vulnerable to the COVID-19 shock. Therefore, low-income homeowners may struggle more to sustain homeownership once the forbearance period is over, and many low-income renters are likely to lose the financial ability to become homeowners. At the same time, the home price trajectory is unlikely to change, as all households, both owners and renters, need a place to live. But the homeownership rate is expected to decrease, making it harder for many families to build wealth.

If the supply constraints that existed before the pandemic remain unaddressed, both low-price home and rental prices will continue to increase faster than prices for high-price homes, widening residual income inequality between low- and high-income homeowner and renter households. This could also hurt the ability of low-income households to build financial strength and could make them more vulnerable to future economic shocks.

Addressing the housing supply shortage and tight credit may not seem urgent, but these constraints will not go away with the pandemic, and they will hamper our ability to bring all households out of the crisis and onto the road to a full recovery.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.