<p>Natalia Mendez goes over mortgage terms with Raul J. Alvarez, Senior Loan Officer for Paramount Residential Mortgage Group. Photo by Joe Raedle/Getty Images.</p>

Mortgage servicers perform a critical role in supporting a healthy housing market, a role that has become increasingly complex and important over the past decade. But servicing mortgages today, particularly when borrowers run into trouble paying their mortgage, is expensive and complicated because of regulations put in place in response to the housing crisis. Our research is clear: we need to update mortgage servicing to make it easier for creditworthy borrowers to obtain a mortgage.

The shifting role of mortgage servicing

Mortgage servicers have historically been “behind-the-scenes” players in the housing market, performing routine but critical administrative work that begins after a borrower takes out a mortgage: sending monthly statements; collecting and remitting monthly payments to investors, insurance companies, and tax authorities; and working with borrowers who have delinquent loans or are facing foreclosure. After the 2008 housing crisis, servicers were thrust into the spotlight as an unprecedented number of borrowers started having trouble paying their mortgages and entered foreclosure.

In response to the crisis, Federal agencies created new regulations designed to help servicers quickly resolve and minimize homeowner losses. While many of these measures were helpful during the crisis, stabilizing mounting losses and establishing needed standards, they remain on the books today, even while delinquency and foreclosure rates have stabilized from crisis levels. Many of these regulatory requirements have added significant cost and complexity to the process, making it too hard for those with less-than-perfect credit to get a mortgage.

And despite this significant regulatory evolution, the fundamentals of mortgage servicing remain largely unchanged, including the way servicers are compensated.

Mortgage servicing providers have evolved with the regulatory landscape. In recent years, we have witnessed the rapid growth of nonbank servicers, which manage more than half the nation’s mortgage loans and have introduced new regulatory, risk, and capital questions that have not been fully addressed. New servicing business models have also emerged, with subservicing and specialized servicers entering the market and many traditional servicers exiting the market.

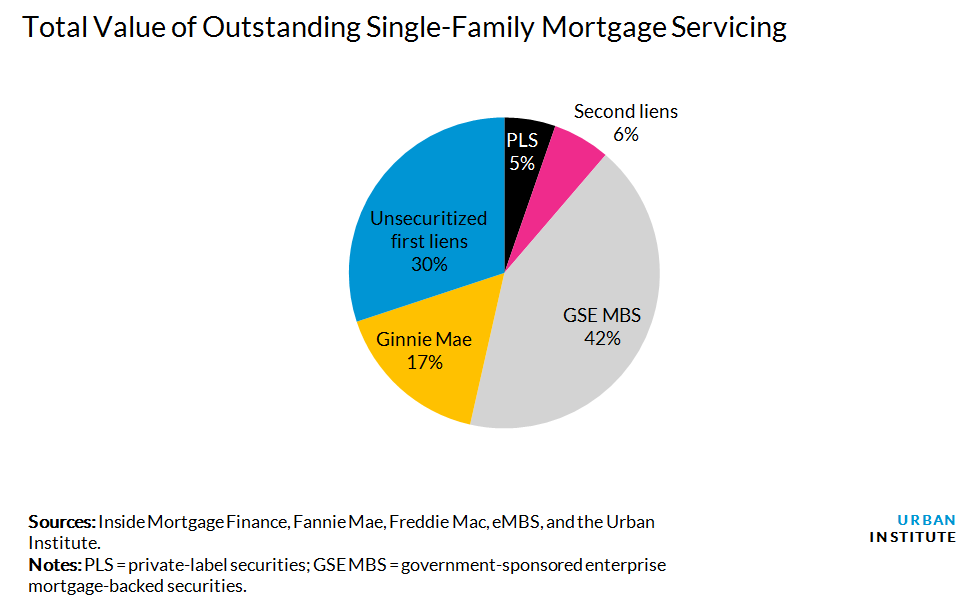

The financial crisis revealed the housing finance system’s vulnerability, as well as the centrality and general underappreciation of the role of mortgage servicers, who manage over $10.2 trillion in single-family mortgage servicing outstanding nationally. The viability, liquidity, and stability of servicing over the long term are critical and must be part of the conversation about how we comprehensively reform our housing finance system. Now is the time to address the unfinished business in mortgage servicing.

A new approach: The Mortgage Servicing Collaborative

To improve access to mortgages, the Urban Institute’s Housing Finance Policy Center (HFPC) is launching the Mortgage Servicing Collaborative. The Collaborative will bring together lenders, servicers, consumer groups, civil rights leaders, academic researchers, and policymakers to develop evidence and analysis that will support solutions and deliver recommendations for mortgage servicing reforms.

The Collaborative will also increase awareness of the role and importance of mortgage servicing to the US housing finance system. The collaborative will draw upon existing research on mortgage servicing, including HFPC’s work assessing the industry since the crisis, and will bring deeper data and new research to the conversation.

The Collaborative will

- identify the costs of servicing various loan types under the current regulatory framework and how those costs affect consumer access;

- foster debate and analysis on pricing strategies, including alternative compensation models, viable options for lowering costs, and tools to better mitigate risk; and

- produce and disseminate research findings and policy recommendations, including those by collaborative members, or a collection of policy options that can clarify and advance the debate.

To follow the Collaborative’s work, visit the Mortgage Servicing Collaborative and sign up to receive HFPC’s bimonthly newsletter with links to all related work and publications.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.