Note: This post was corrected to reflect that 48 percent, not 49 percent, of all 2018 borrowers were high-income households (corrected 6/24/20).

<p>From left to right, Arthur Davis, his wife, Deloris and their daughter Audrey, stand outside their home that has been in their family since 1954. Their next door neighbor Joseph "Tex" Gathings stands behind them on the porch. The Davis family has received several letters from real estate agents trying to get them to sell their home, in Highland Beach, Maryland, a historically Black beach community where Frederick Douglass spent his summers. July 22, 2017. (Photo by Cheriss May for The Washington Post via Getty Images)</p>

Gentrification is a hotly debated subject, with conversations centering around what happens to neighborhoods’ income and racial mix as new buyers move in and how that affects current residents. Although the impacts of gentrification are still being studied and debated, it’s important to understand what increases the pace of gentrification, which we define for this analysis as how fast high-income homebuyers move into low-income neighborhoods.

We combined two datasets to examine the movement of high-income borrowers into low-income areas and the varying pace of this movement across different metropolitan statistical areas (MSAs). Our analysis focuses only on income because homebuyers’ race or ethnicity was not available at comparable levels of granularity in the two datasets.

Our examination reveals that, in many MSAs, high housing costs—resulting from a lack of available housing—cause affluent buyers to look for homes in low- and moderate-income (LMI) neighborhoods. That means cities’ housing supply can determine how fast gentrification may occur. Boosting the supply of housing can slow the pace of new buyers moving into lower-income neighborhoods.

Nationally, high-income homebuyers purchase in LMI neighborhoods at the same rate they already live in these neighborhoods

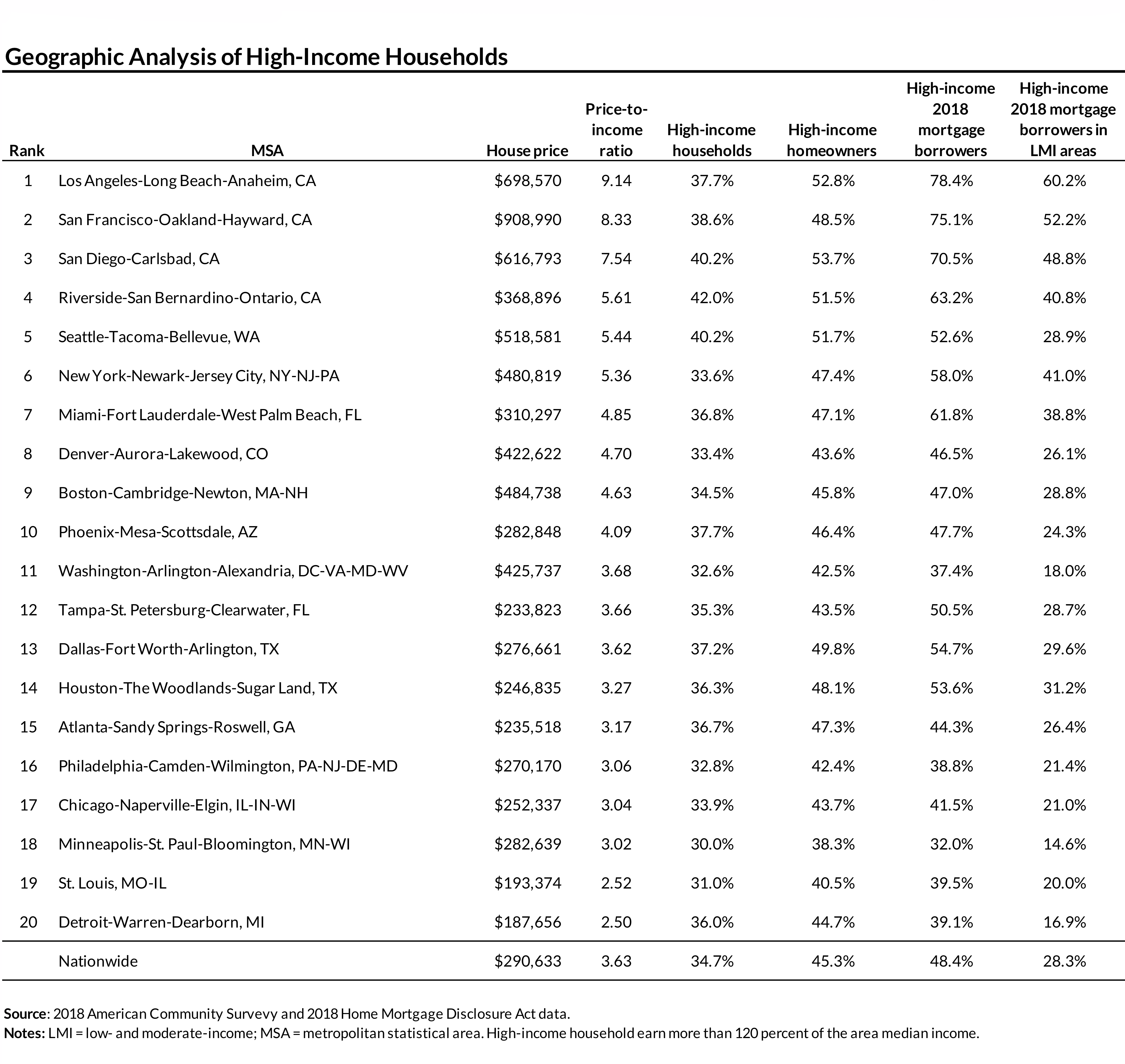

We looked at 2018 Home Mortgage Disclosure Act and 2018 American Community Survey data to determine the prevalence of high-income homebuyers in LMI areas. We then examined the price-to-income ratios (using area median incomes, or AMIs) in the 20 largest US MSAs to get a sense of housing supply challenges. (View and download data on the 74 most populous MSAs.)

At the national level, high-income buyers (those earning above 120 percent of the AMI) take out new mortgages to buy homes in LMI neighborhoods at a slightly higher rate (29 percent) than they already own homes in these neighborhoods (26 percent).

But low-income buyers (earning up to 50 percent of the AMI) are taking out new mortgages to buy homes in LMI neighborhoods at much lower rates (14 percent) than their homeownership rates in these neighborhoods (31 percent).

For households with moderate incomes (earning 50 to 80 percent of the AMI), the share of new mortgages (31 percent) is significantly higher than the share of current homeowners (21 percent), and for middle income households (earning 80 to 120 percent of the AMI), the share of new mortgages is somewhat larger (27 percent) than their rates of already owning homes in the neighborhood (21 percent).

In terms of mortgage borrowing nationally, the biggest difference between new mortgages and current ownership rates is in the share of mortgage borrowers in the low-income group. There are comparatively few new mortgage borrowers with low incomes relative to the share of current homeowners with those incomes. This difference is, in part, the result of a lack of supply of houses for sale and of mortgages at the low end of the housing price spectrum.

In cities with limited housing supply, high-income homebuyers disproportionately look to LMI areas

The income distribution of all homeowners and renters does not vary much across the 20 largest MSAs, but the distribution of new mortgage borrowers in 2018 was different among the MSAs. We estimated the number of current high-income homeowners in LMI neighborhoods for a small number of MSAs, including Los Angeles and Chicago.

Nationally, high-income households represent 45 percent of homeowners, 48 percent of all 2018 borrowers, and 28 percent of 2018 borrowers in LMI areas. But in Los Angeles, the MSA with the highest price-to-income ratio, 53 percent of current homeowners and 78 percent of 2018 borrowers have high incomes.

Most importantly, the rate of gentrification in LMI neighborhoods could be rapid, as the 60 percent purchase rate of high-income borrowers in LMI Los Angeles neighborhoods significantly exceeded their current presence in LMI neighborhoods of 38 percent. A greater share of new borrowers in LMI areas in Los Angeles (60 percent) have higher incomes than do current homeowners across the city (53 percent).

Conversely, in Chicago, a city with more affordable housing (as indicated by a price-to-income ratio in the bottom quartile), the share of high-income 2018 homebuyers in LMI areas is barely half the share of current high-income homeowners in the city. In fact, the share of high-income borrowers in LMI areas is slightly lower than the share of current high-income homeowners in LMI areas.

The figure above shows the relationship between the price-to-income ratio and the share of recent purchases by high-income borrowers in low-income neighborhoods for the 75 largest MSAs. Although not perfect, the correlation is high. This suggests that when housing prices are high in an MSA, as indicated by a high price-to-income ratio, high-income borrowers will look to LMI neighborhoods to buy homes.

An area’s price-to-income ratio is better than home prices at predicting high-income buyers’ interest in LMI neighborhoods

We also find that the price-to-income ratio is a more important determinant than home price of the propensity of high-income people to buy in LMI areas. Most starkly, at $909,000, the median home price in San Francisco far exceeds Los Angeles’s $699,000. But Los Angeles’s 9.14 price-to-income ratio exceeds San Francisco’s 8.33 ratio, and a substantially greater share of high-income households buy in LMI neighborhoods in Los Angeles.

In MSAs with a high price-to-income ratio, even high-income borrowers are stretching to purchase a home, and they are increasingly venturing into LMI areas. Middle- and low-income borrowers are finding it increasingly difficult to buy in LMI areas, as prices for low-price homes have increased faster than prices for more expensive homes. These areas with a high price-to-income ratio tend to have a lower homeownership rate than the national average. This is particularly true in California MSAs, but the New York and Miami areas also show signs of high-income movement in LMI neighborhoods and somewhat depressed overall homeownership rates.

These data show that when even affluent buyers must stretch to become homeowners, they are likely to look to LMI neighborhoods to purchase homes. Boosting the housing supply by easing local land use, building, and zoning restrictions and encouraging alternative forms of housing like manufactured housing and accessory dwelling units would make homes more affordable and allow more buyers at all income levels to find homes, slowing the pace of gentrification.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.