<p>Tetra Images/Getty Images</p>

Congress enacted the 1977 Community Reinvestment Act (CRA) to encourage depository institutions to help meet their communities’ credit needs, including the needs of low- and moderate-income (LMI) neighborhoods. On June 5, 2020, 25 years after the last major update to the regulations, the Office of the Comptroller of the Currency (OCC) issued new regulations that would markedly change the system for evaluating banks’ CRA performance

Even though the banking industry has drastically changed since the CRA was enacted, the current regulations are working reasonably well. Any modernization efforts should be rooted in data, and, as we have written elsewhere, there is no need for change in the middle of a pandemic.

Accurate data that illustrate how the current rules are working can provide a critical foundation for modernization. They can show us where and how CRA credit is being generated and whether and how the CRA is benefiting all communities (including LMI neighborhoods) in which each bank operates.

To build the evidence base, we analyzed 2018 data about the quantity of CRA lending banks engaged in for each of the five major loan categories: single-family mortgages, small business loans, small farm loans, multifamily loans, and community development loans. (Our methodology is described below.) This is an update to an analysis we did using 2016 data. Our results are shown in table 1.

Our analysis revealed three main conclusions:

- Community development and single family lending swapped places in 2018 as contributing the greatest volume of CRA credit, with community development lending moving from second place in 2016 with $96 billion in lending to first place in 2018 with $103 billion.

- Single-family lending volume fell dramatically, from $108 billion in 2016 to $95 billion in 2018, a result of the decrease in refinance volume between the two years.

- Though the order of the other three types of lending remained the same in 2018, the multifamily CRA contribution rose significantly, from $33 billion to $42 billion, and the contribution from small business and small farm loans fell slightly, to $86 billion and $8 billion respectively.

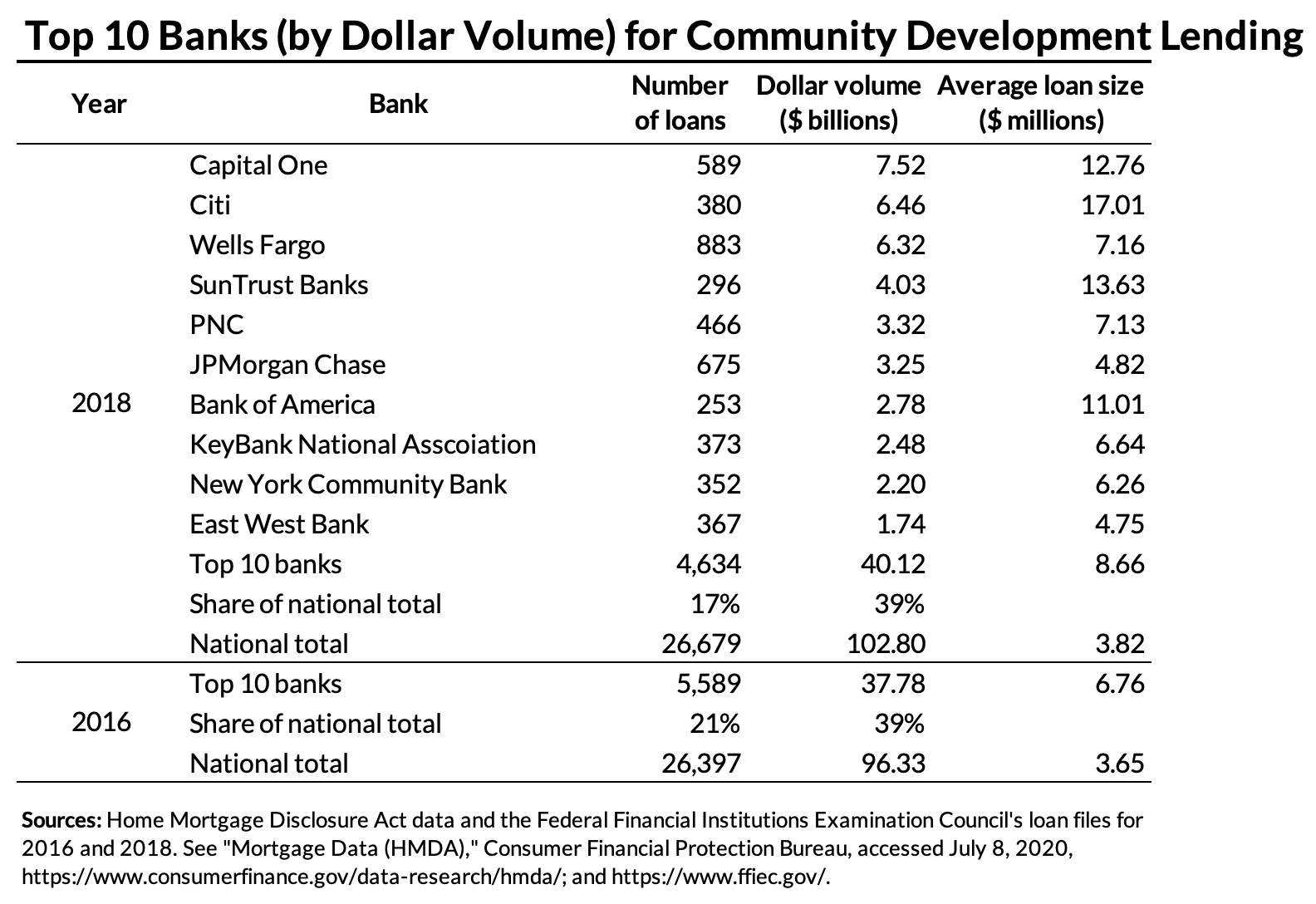

Community development lending in LMI areas increased by $7 billion from 2016 to 2018

Community development lending increased from $96 billion to $102.8 billion between 2016 and 2018, while loan size remained roughly constant. We attribute a large part of the increase in community development loans to the huge growth in multifamily lending. Lending for affordable multifamily properties within a bank’s assessment areas can “double count” toward CRA requirements, earning both multifamily and community development lending credit.

Year-over-year comparisons at the bank level are difficult, as regulators do not fully disclose the resubmission and data correction process. Accordingly, we cannot explore the reasons for the substantial increase in community development lending. Table 2 shows the share of share of community development loans held by the 10 banks with the largest dollar volume of CD lending; assuming none of these banks resubmitted their data, the share of community development lending by these banks, as measured by dollar volume, held constant at about 39 percent. We urge regulators to disclose or give some other indication when a resubmission of data results in bank-level or aggregated updates.

Single-family lending dropped to second place among CRA lending contributors between 2016 and 2018

Single-family lending lost its standing as the largest contributor toward CRA credit in 2018 thanks to a reduction in the overall number of single-family loans.

From 2016 to 2018, interest rates rose, leading fewer people to refinance their mortgages. Between 2016 and 2018, the average 10-year Treasury rate rose from 1.84 percent to 2.91 percent, and the average primary mortgage rate rose from 3.65 percent to 4.54 percent.

In the same period, the volume of single-family mortgage originations by banks dropped by $171 billion, and the number of originations dropped by 520,000 loans. And while the share of CRA-eligible single-family loan dollars increased marginally from 12 to 13 percent, total CRA-eligible single-family loan dollars dropped from $108 billion to $95 billion between 2016 and 2018.

Multifamily lending in LMI areas increased by $11 billion between 2016 and 2018

In contrast, multifamily lending—measured by the number of loans and their total volume—increased sizably. The dollar volume of multifamily loans increased by $31 billion, including $11 billion in increased LMI lending between 2016 and 2018.

In addition, the amount of LMI multifamily lending within banks’ assessment areas, which also qualifies as CRA lending, increased by $9 billion. (We may over- or underrepresent the amount of multifamily lending that earns CRA credit because we count all multifamily lending in an LMI tract as LMI lending, Because of data limitations, we are unable to exclude high-end properties that may not obtain CRA credit, or include affordable multifamily lending that is not in LMI tracts.)

This increase in multifamily lending is mirrored by an increase in construction activity. Census data indicate that the number of multifamily units completed rose from 311,000 to 335,600 in 2018. The Federal Reserve’s flow of funds data also indicate a large increase in multifamily lending over this period.

The bottom line

In our analysis of what counts toward CRA lending in 2018, we find only modest changes from 2016 in the ranking of loan types. Dramatic decreases in interest rates will increase mortgage lending and refinancing activity in 2019 and 2020, which under normal circumstances would be expected to lead to a substantial increase in single-family CRA activity. However, we are concerned that the increases in CRA activity in 2020 will be muted, as the pandemic has tightened the credit box appreciably.

A quick look at our methodology

For our analysis, we used Home Mortgage Disclosure Act (HMDA) data and the Federal Financial Institutions Examination Council’s (FFIEC) loan files for 2016 and 2018. Our analysis focused on lending; because of insufficient data, we could not analyze investments, which also count for CRA credit.

For small business and small farm lending, the FFIEC loan files contain, for each CRA reporter, the number and dollar amount of lending, cross-tabulated by census tract, and information about whether the loan is in the reporter’s assessment areas. We defined a CRA-qualifying small business or small farm loan as a loan to a small business (or small farm) or a small loan to a business (or farm) in an LMI census tract within a bank’s assessment area, and calculated accordingly. For community development loans, the FFIEC files contain only the number and dollar volume of loans; we assumed these loans are all CRA eligible.

For mortgage lending, we matched HMDA lending by institution, by tract, with the CRA files created by the FFIEC. Our match rate was high. HMDA data gave us tract-level information on each lender, while the FFIEC data gave us information on assessment areas. We defined a CRA-qualifying single-family mortgage loan as a mortgage to an LMI borrower or in an LMI census tract within a bank’s assessment area. For multifamily mortgages, we counted as CRA-eligible only loans secured by properties in LMI census tracts within a bank’s assessment area. In computing the final results, we grossed up the numbers for our matched institutions to reflect the number and dollar volume of HMDA loans.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.