<p>Photo by Bounce/Getty Images.</p>

Leaving school in a recession is tough. Researchers have shown that graduating in a bad economy has long-term negative consequences on employment and earnings. Student borrowers who graduate or leave school during a recession might have trouble earning enough to repay their student debt, increasing the likelihood that their loan balances keep growing, or they default.

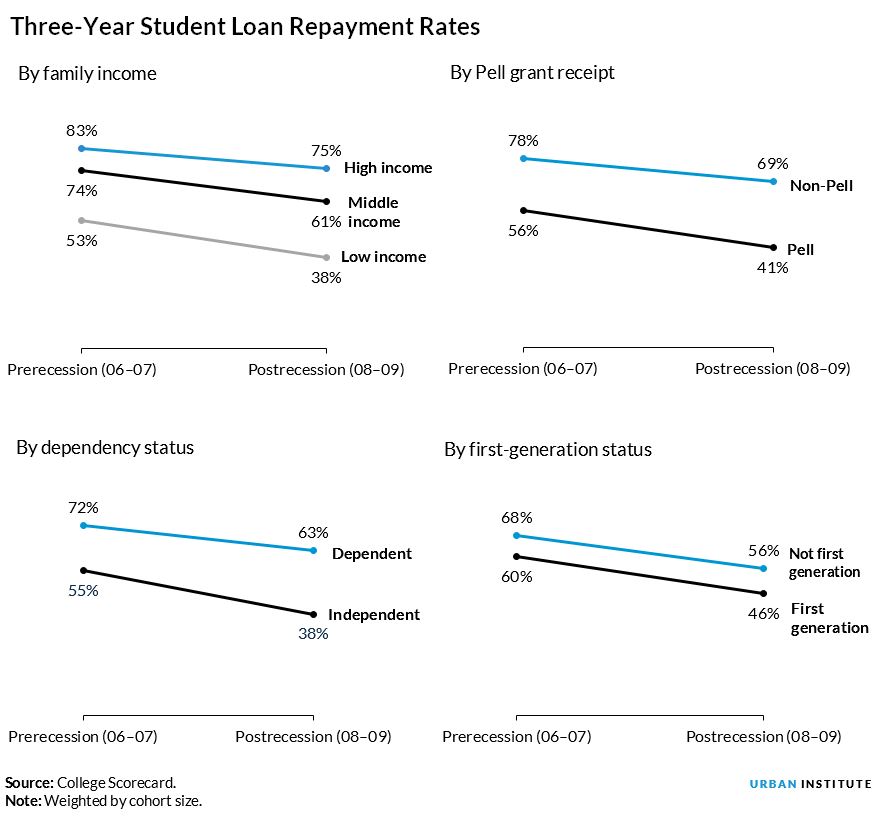

Ten years after the Great Recession, we look back at the impact of the recession on student loan repayment rates. We find that student loan repayment rates were lower for students who left school during the recession relative to those who left one or two years earlier. Postrecession repayment rates declined the most for students from low-income backgrounds and students who are independent of their parents for financial aid consideration (typically those older than 23).

Previous research indicates that overall student loan default rates rose in the 2008 recession. An increase in the share of nontraditional borrowers and declining labor market opportunities (because of the home price collapse) are both correlated with this change.

In this analysis, we rely on data from the College Scorecard, weighting each college by the number of student borrowers. The College Scorecard repayment rate reflects the fraction of borrowers who are not in default and have paid down at least $1 on their initial loan balance at different points after leaving school.

One-year student loan repayment rates dropped 14 percentage points between cohorts who entered repayment in fiscal years (FY) 2006–07 (October 2005 through September 2007) and those who entered repayment in FY 2008–09. This drop-off continues for later borrower cohorts (FY 2010–11 and FY 2012–13) but is less steep. Three years out from entering repayment, the steepest drop in repayment rates, 13 percentage points, is between the immediate pre- and postrecession cohorts.

When comparing the FY 2006–07 prerecession cohort with the FY 2008–09 postrecession cohort, we find that students from low-income families, Pell recipients, and independent students were more likely to experience a substantial drop in repayment rates. Three-year repayment rates declined nearly twice as fast for independent students and those from low-income backgrounds as for others. Although first-generation students have low average loan repayment rates, the rate of decline in repayment across the pre- and postrecession periods was similar for both first-generation and non-first-generation students.

We cannot attribute all the decline in student loan repayment rates directly to the Great Recession. Two-year cohort default rates, another measure of students’ ability to repay their loans, had been rising before the recession. And a more generous income-driven repayment option was introduced in 2009, which might have allowed more borrowers to remain current on their loans without paying down their initial balance.

In addition, college going tends to increase during recessions. It is possible that people who chose college over work because of the economy struggled to repay their loans after leaving school. Yet, we don’t observe meaningful differences in freshman-year retention rates across the pre- and postrecession cohorts, which we might expect if the recession increased the likelihood that students stopped out for economic or academic reasons.

We might also expect that students induced into school by the recession are more likely to attend two-year schools. But the trends for students from four-year schools mirror overall trends, with a steep decline in repayment rates among independent students and those from low-income backgrounds.

That student loan repayment rates drop in a recession is not surprising. Actual and proposed accountability measures based on student loan repayment status vary as to whether they account for economic conditions in setting benchmarks. For example, the “positive repayment status” repayment threshold outlined in the House Republicans’ proposal for reauthorizing the Higher Education Act does not account for economic conditions, save for a provision that allows individual borrowers to prove economic hardship. Other measures have proposed accountability schemes that account for local economic conditions as part of an overall benchmark adjustment. Our results demonstrate the complexity of developing an economic adjustment for student loan repayment because students with different backgrounds have different repayment responses to an economic downturn.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.