<p>University of Maine student Olivia Conrad walks to her car after class in Orono, ME on Thursday, October 9, 2014. Conrad, a sophomore, transferred to the University of Maine after her freshman year at St. Lawrence University, to be closer to family in Yarmouth and save tuition money. Photo by Whitney Hayward/Portland Press Herald via Getty Images.</p>

The new accountability metric outlined in the House Republicans’ proposal for reauthorizing the Higher Education Act might affect more than half of all institutions or no institutions at all.

The bill, known as the PROSPER Act, proposes a substantial change to the way colleges are held accountable for the outcomes of their student borrowers. Because of the act’s other changes to the student loan repayment system, the effect of this new accountability regime is uncertain.

Under current law, colleges are held accountable for their three-year cohort default rate. Institutions with high rates of default three years after borrowers enter repayment (rates greater than 30 percent for three continuous years or greater than 40 percent in one year) are ineligible for providing federal student loans.

Based on data from the most recent cohort, who entered repayment in 2014, 10 schools were subject to loss of eligibility. This metric has been criticized as insufficient for accountability, because students can reduce or delay payments under forbearance, deferral, or income-driven repayment provisions.

The new PROSPER plan

If the PROSPER Act passes, the cohort default rate measure would be replaced with a new measure of loan repayment. A borrower would be considered in “positive repayment status” if her loan is repaid in full, is in deferment (because of military service or enrollment in further education or residency programs), or is less than 90 days delinquent in the second fiscal year of repayment.

This measure would be assessed at the academic program level. Programs that have fewer than 45 percent of their borrowers in positive repayment status for three consecutive cohorts would be ineligible to provide student aid.

To understand the impact of this new accountability regime, we must evaluate it with other loan repayment provisions of the PROSPER Act, which eliminate the possibility of $0 payments for financially stressed borrowers. All borrowers will be required to make monthly payments of at least $25 or payments of $5 if the borrower can demonstrate economic hardship because of unemployment or medical expenses.

Measuring the impact of positive repayment status

Data limitations make it impossible to model the effects on specific programs, but I can approximate how the new rules might play out at the institutional level under different assumptions using available data.

For my analysis, I assume the following:

- Borrowers who pay at least $1 of their postseparation student loan balance within one year (i.e., the one-year repayment threshold reported in the College Scorecard) will pass the new positive repayment status threshold.

- Borrowers who default on their student loans at any point during three-year cohort default measurement period will not pass the new positive repayment status threshold.

- Borrowers who are not in default and who do not meet the one-year repayment threshold have an unknown probability of passing the new positive repayment status threshold.

View the full methodology here.

To assess how many institutions (and thus, at least some programs within them) might be subject to PROSPER’s new accountability regime in a given year, I look at how the share of borrowers in positive repayment status might change when we vary the probability that borrowers in the third group make payments on their loans.

An example of uncertainty

Imagine an institution has a 35 percent loan repayment rate and a 15 percent cohort default rate. The remaining 50 percent of borrowers have not made progress on paying down their loan balance but have not defaulted.

If all these remaining borrowers could make routine $25 monthly payments on their loans under the PROSPER repayment plan, the institution would have an 85 percent positive repayment status. But this assumption could be faulty. These borrowers likely make $0 (or very small) payments under current income-driven repayment, forbearance, or deferment options, which would go away under PROSPER, so a switch to $25 per month might be difficult. If fewer than 20 percent of these borrowers could make these new payments with less than 90 days’ delinquency, the institution would fail the positive repayment metric.

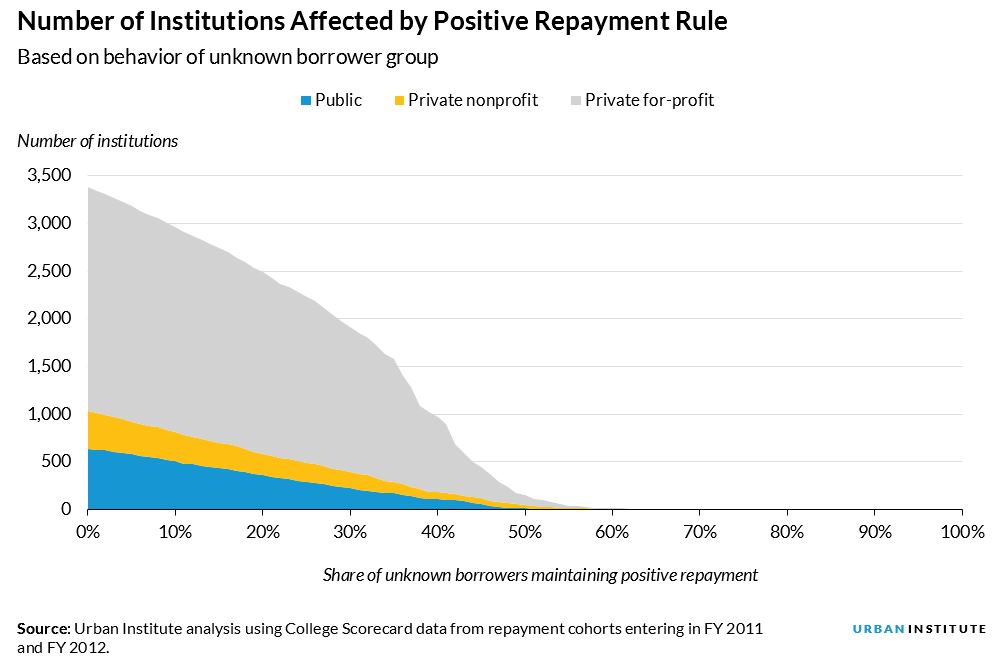

Estimating uncertainty for all Title IV institutions

By shifting our assumptions of what share of these unknown-status borrowers can make payments of at least $25, we can estimate the number of institutions that might fail the new accountability metric. Using College Scorecard data from borrowers entering repayment in fiscal years 2011 and 2012, I estimate the number of institutions that would be affected if a given share of their unknown borrowers do not maintain positive repayment status.

If none of these unknown borrowers would maintain positive repayment in the new system, 3,378 institutions (57 percent of institutions with loan repayment data for these years, serving 35 percent of all undergraduates) would be affected. If 20 percent maintain positive status, as in my example, 2,488 institutions (23 percent of undergraduates) would be affected. At 50 percent, just 149 institutions (1 percent of undergraduates) would be affected.

My best estimate of accountability under this new metric using publicly available data is that the PROSPER positive repayment metric could result in the failure of anywhere from the majority of institutions to no institutions. If student loan outcomes are different across programs, as they tend to be, the variation in potential impact could be even wider.

These results underscore the uncertainty of building a new accountability metric and reshaping the underlying repayment system being measured. Institutions and programs will respond to the incentives the new repayment system creates, which could further change borrower behavior. To expand on an old cliché, it seems that lawmakers are building the plane while holding it accountable for on-time performance, resulting in a murky future for both institutions and borrowers.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.