<p>Sean De Burca/Getty Images</p>

Most student loans have been put into administrative forbearance during the COVID-19 pandemic, but that doesn’t mean borrowers aren’t taking action on their loans. A small share of borrowers, particularly younger borrowers, appear to have lowered their expected monthly payments, possibly by switching plans or by recertifying their income-driven repayment (IDR) plan to adjust for lower income.

Nearly all federal loan borrowers have opted to take advantage of the student loan pause. Just 300,000 Direct Loan borrowers were making payments on their loans in June 2020, compared with 18.9 million in repayment at the same time last year. But data from the US Department of Education’s Federal Student Aid office also indicate continued new enrollment in IDR during this time, which will likely lower payments due when the pause ends. About 100,000 borrowers were added to the IDR program between March and June 2020, continuing a steady upward trend in the number of IDR borrowers over time.

How we look at monthly payments

The Federal Student Aid numbers indicate new participants in the IDR program but don’t tell us how many borrowers have changed their expected payment during this period (for example, by recertifying their IDR plan at a lower income). To understand which borrowers appear to be actively managing their loans during the payment pause, we use credit bureau data to look at the share of people who have recorded monthly payments that are lower than we would expect under a standard, 10-year repayment plan. This does not mean people are actually making these payments; the monthly payment amount is still recorded and updated in credit bureau data as if it were a regularly scheduled payment (PDF), even if the loans are in administrative forbearance.

We classify borrowers as paying less than expected if their expected monthly payment is less than 80 percent of what they would pay on a standard 10-year repayment plan (estimated with an interest rate of 4.45 percent in February and 0 percent in August). There are several reasons a person could have a recorded monthly payment that is lower than expected. Borrowers could be moving on to an IDR plan, or they could be starting an extended or graduated repayment plan to lower their payments.

Borrowers already on IDR could also recertify their income, obtaining a lower monthly payment if they are getting fewer hours or are laid off. Some states, in partnership with nonprofits, are helping unemployed borrowers access resources, such as IDR, to lower their student loan payments. Because recertification is not required until the end of the student loan pause (currently December 31, 2020), it is also possible those who would recertify to a higher monthly payment (because of a raise or other income increase) are opting to wait until they are required to do so.

Enrollment in IDR conveys an additional advantage during the student loan pause. During the time the administrative forbearance is in effect, these months still count toward the period of IDR repayment, effectively lowering the total amount the borrower will pay back.

The share of borrowers with lower-than-expected payments has increased during the pandemic

We find that 38.2 percent of student loan borrowers making payments in February 2020—before the pause—had an expected monthly payment far below a standard 10-year payment amount. Among the same group of borrowers in August 2020, this share increased to 42.6 percent.

Although we estimate an increase of only about 4 percentage points in the share of borrowers who appear to be paying less than they would under a 10-year plan, we find substantial differences in the types of borrowers who appear to be lowering their payments.

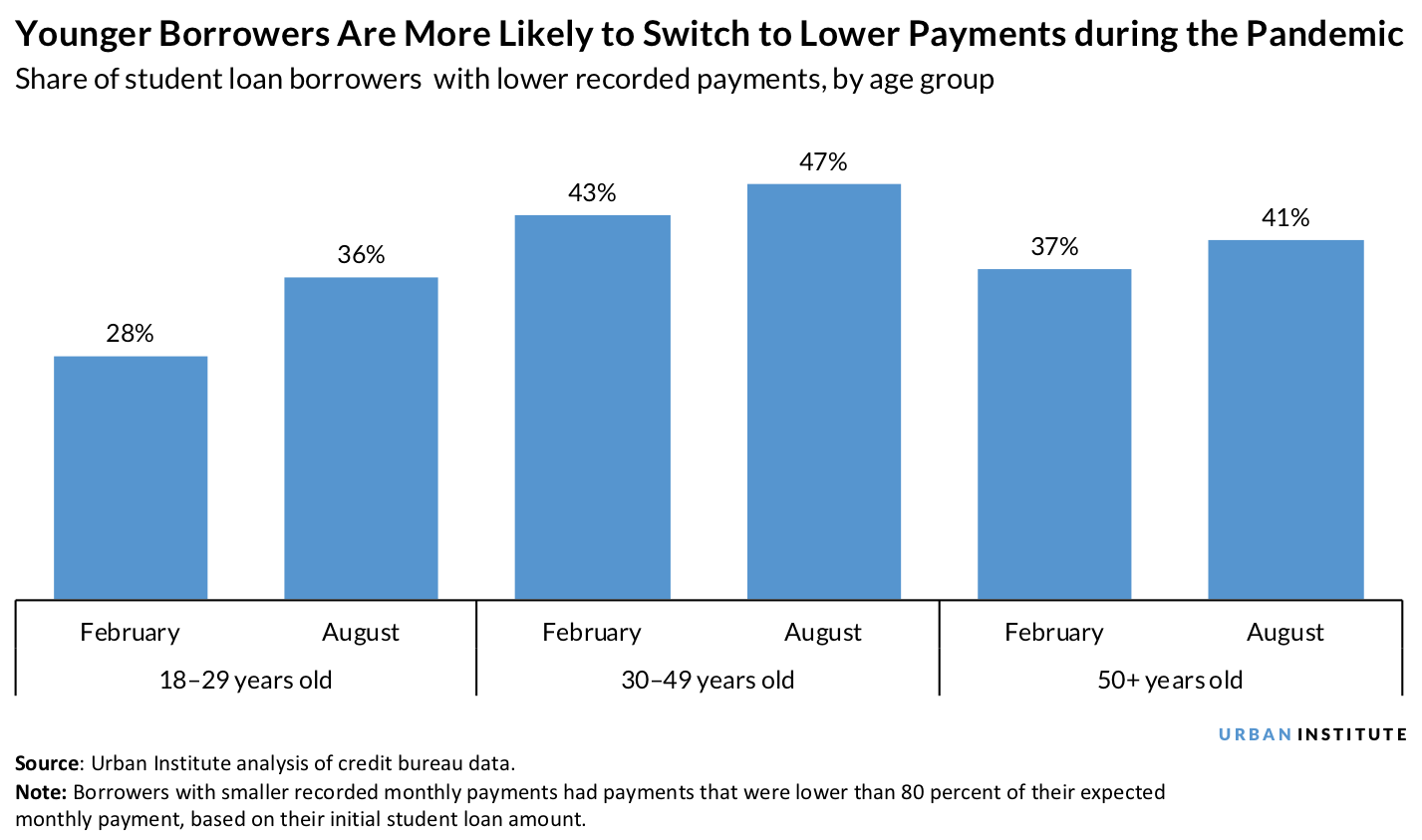

Younger borrowers were more likely switch to lower payments during the pandemic

Borrowers ages 18 to 29 were most likely to have lower payments in August 2020, relative to their student loan amount, compared with the payments that were recorded in February 2020. The share of borrowers in this age group who appear to have lower payments increased by about 8 percentage points between February and August. Increases in those making lower payments among borrowers ages 30 to 49 and 50 or older were smaller (4 percent). However, borrowers in these age groups were already more likely to be paying less than they would under a standard 10-year plan.

Younger adults experienced the highest level of unemployment during the early months of the pandemic, which may have pushed them to enroll in IDR or to recertify at a lower repayment amount. Younger borrowers may also be more likely to have access to more recent, more generous IDR options. Borrowers with older loans, or those with Parent PLUS loans, tend to have access to less generous IDR plans, and may have to take additional steps to enroll, such as loan consolidation.

Borrowers in communities of color appear more likely to move to lower payments

Our credit data don’t report race and ethnicity, but we are able to match borrowers to the demographics of their neighborhood, as estimated in the 2017 five-year American Community Survey, using their zip code and age category.

Results from this analysis suggest that borrowers who live in communities of color (less than 40 percent non-Hispanic white population in their age cohort) were more likely to move to lower payments during the pandemic than white communities (more than 60 percent non-Hispanic white).

The share of borrowers living in communities of color with lower payments increased by roughly 5 percentage points, compared with 3 percent in white communities. This increase in communities of color was primarily among borrowers older than 30.

Student loan debt disproportionately burdens borrowers of color, particularly Black borrowers. These results suggest a small gain in lowering payments for borrowers of color, but this result should be interpreted with caution. We can only look at results for those in repayment in February, so our findings exclude those in default or who were in deferment because of economic hardship. And, of course, these results only serve as a proxy for race and ethnicity.

What’s next for the pause?

It is unlikely that the disruption caused by the COVID-19 pandemic will end at the end of December, but the student loan pause is scheduled to. These results suggest that some borrowers are taking steps to manage their payment amounts before the pause ends. As policymakers consider whether to extend the pause into 2021, they should press for more detailed information about which borrowers appear ready to resume payments and which do not.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.