<p>Photo by Michael Berman/Getty Images.</p>

Recently, policy leaders have developed proposals that would allow new parents to trade future Social Security retirement benefits for time off to bond with newborns and newly adopted children.

One such proposal, the New Parents Act, introduced last month by Sen. Marco Rubio (R-FL) and Rep. Ann Wagner (R-MO), builds on similar ideas from the Independent Women’s Forum (PDF) and Sens. Ernst (R-IA) and Lee (R-UT) (PDF) that use Social Security to fund paid parental leave. The New Parents Act would replace nearly half of earnings for middle-class workers receiving the benefit.

But like our analysis of earlier proposals, our analysis of the New Parents Act described in this blog post shows the program could jeopardize the future financial security of parents who take paid leave, especially those who take multiple leaves. Parents who take three three-month leaves, for instance, would lose as much as 12 percent of their Social Security retirement benefits.

How the program would work

Under the New Parents Act, parents could choose to take one, two, or three months of paid leave following the birth or adoption of a child. The program would compute monthly payments using the Social Security disability benefit formula, but the leave program would have less strict work requirements. Payments would depend on past earnings and would replace a larger share of a paycheck lost by a low-wage worker than by a high-wage worker.

Parental leave payments would come out of Social Security trust funds, and Social Security would recoup costs by reducing future Social Security retirement benefits for leave participants. The Social Security actuaries estimate (PDF) that, to fully cover costs, participants would have to forfeit two months of future retirement benefits for each month of parental leave, the same trade-off that Melissa Favreault and I computed last year for a similar proposal.

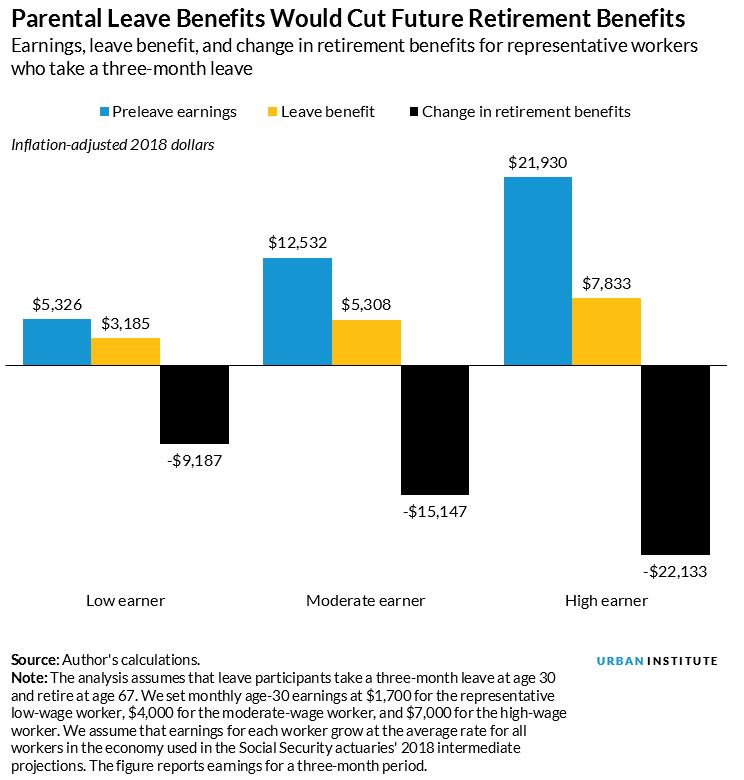

How the program would affect retirement benefits

We looked at how the New Parents Act would work for mothers who would give birth at age 30 in 2022, the program’s first year. If they opt for three months of paid leave, low-wage mothers earning $1,700 per month would receive a three-month leave benefit of $3,180, replacing 62 percent of her three-month earnings. The leave benefit would replace 44 percent of earnings for a moderate-wage mother earning $4,000 per month and 37 percent of earnings for a high-wage mother earning $7,000 per month.

Let’s assume that these mothers return to work once their leave ends and work continuously until age 67, with their earnings growing at the average rate for all workers in the economy as projected by the Social Security actuaries. The leave program would cut their Social Security retirement benefits by nearly three times the inflation-adjusted value of the benefits they received as new mothers.

In exchange for parental leave taken 37 years earlier, a low-wage worker would forfeit $9,200 in retirement benefits (in inflation-adjusted 2018 dollars), a moderate-wage worker would forfeit $15,100, and a high-wage worker would forfeit $22,100.

View the Social Security actuaries’ 2018 intermediate projections here.

If paid-leave takers instead spread their Social Security cuts throughout retirement, they would forfeit between 3.1 and 4 percent of their Social Security benefits each month, depending on when they begin collecting Social Security. Parents who take three three-month leaves would lose as much as 12 percent of their Social Security retirement benefits.

We analyzed a similar bill introduced by Sen. Rubio last year, as well as the plan developed by the Independent Women’s Forum. We found that both plans would erode retirement security and worsen Social Security’s finances. Sens. Ernst (R-IA) and Lee (R-UT) (PDF) have also released a proposal that would allow new parents to trade future Social Security benefits for paid leave.

A strong case can be made for guaranteeing parents paid leave, as all other wealthy nations do. But Social Security may not be the best way to finance those benefits.

Concern about the financial security of future retirees is increasing. The share of workers entering retirement with traditional employer-sponsored pensions will continue to decrease. Growing numbers of retirees are deep in debt, and rising out-of-pocket spending on medical care and long-term services and supports further drains retirees’ resources.

Social Security also faces a long-term financing gap that may lead to future benefit cuts. Workers can increase their retirement incomes by working longer, but job loss and health problems force many to retire earlier than expected. With so much uncertainty, it’s hard to justify programs that divert resources from retirement, no matter how well intentioned.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.