<p>A restaurant on 2nd Avenue is boarded up as US cities continue to shelter-in-place during the coronavirus pandemic on April 16, 2020 in New York City. (Photo by John Lamparski/Getty Images)</p>

<div> </div>

The Senate and the House are expected to shortly approve, and the president is expected to sign, a second coronavirus relief package (PDF), including an additional $310 billion to the Paycheck Protection Program (PPP), which offers low-interest loans to small businesses and nonprofits, forgiven if the borrower maintains or restores its full-time employment and salary levels. By April 16, 20 days after enacted, the program had disbursed the $349 billion initially allocated, leaving many struggling applicants without cash assistance.

As we have written previously, additional PPP funds are important as large-scale layoffs continue. But with this latest round of legislation, we lost a key opportunity to improve the program and ensure it supports the businesses most in need. Adding money to a program with well-understood shortcomings risks deploying federal resources in a way that could even worsen economic inequality.

Early evidence from Small Business Administration (SBA) data (PDF) on PPP loans approved between March 30 and April 13 suggests that dollars from the first round of the PPP may not be flowing to the sectors hardest hit by this crisis.

The accommodations and food industry received only 9 percent of PPP funds, despite accounting for nearly two-thirds of all jobs lost by PPP-lent sectors in March. Conversely, the professional, scientific, and technical services sector, which actually gained 7,500 jobs in March, received the second-most PPP dollars.

Other sectors, such as construction (14 percent of PPP dollars) and manufacturing (12 percent of PPP dollars), experienced proportionately less job loss in March.

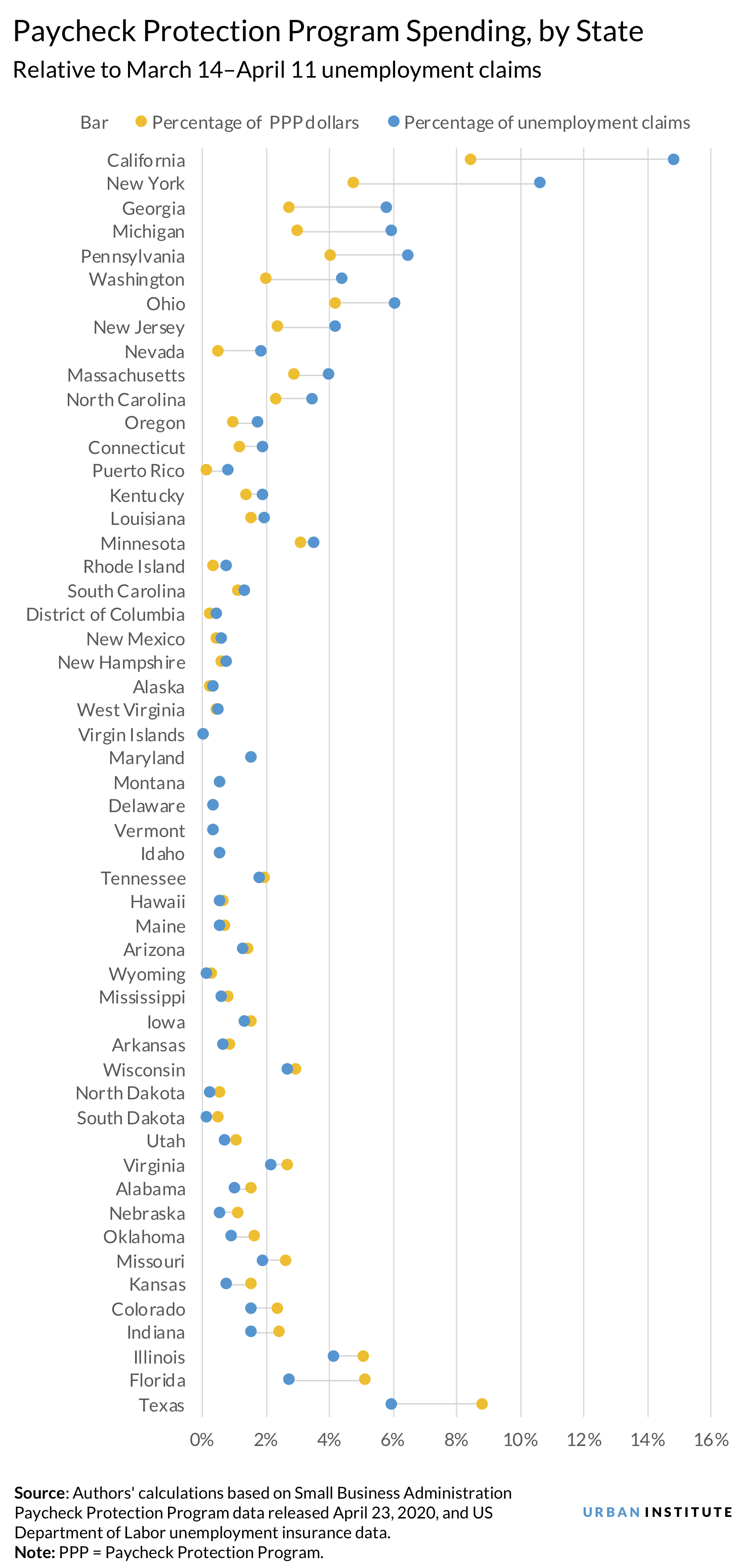

The state distribution of PPP dollars also does not align with the areas of the country hardest hit by the pandemic’s economic fallout.

Most strikingly, the two states with the highest number of unemployment claims between March 15 and April 11 received a proportionately lesser amount of PPP dollars. California experienced 14.8 percent of the nation’s unemployment claims but only 8.4 percent of PPP lending. New York saw 10.6 percent of unemployment claims but only 4.7 percent of PPP lending.

Although Texas received the greatest share of PPP funds, at 8.8 percent, it experienced only 5.9 percent of unemployment claims. Florida also received a disproportionate share, with 5.1 percent of PPP lending but only 2.7 percent of unemployment claims. (But, as Florida processes unemployment claims at the slowest rate in the nation, it is possible the state will catch up.)

Because PPP funds are limited and are distributed using a first-come, first-serve approach, many businesses may be preemptively applying for funds, regardless of whether they will effectively need them.

What we do know is that the program’s design lacks targeting based on need. Organizations experiencing no repercussions from COVID-19 can apply and get their loans approved, which could effectively turn into grants when forgiven.

Some reports reveal that almost 100 companies that received PPP loans were publicly traded. The PPP loan application form (PDF) only requires the applicant to certify that “current economic uncertainty makes this loan request necessary to support the ongoing operations of the Applicant.” But there is no prioritization around revenue shortfalls and no vetting requirements. The SBA has attempted to tamp down publicly traded firms from accessing the program, but the approach fails to truly target need.

Arguably, the PPP is prioritizing speed and scale over need. But other countries have found solutions to better target their relief while maintaining quick dispersal. In Canada, businesses must verify a 30 percent decline in revenue to qualify for the federal government’s 75 percent wage subsidies. In their applications, businesses submit year-over-year earnings to verify this loss of revenue (with exceptions for start-ups and new firms). The Netherlands and Denmark have taken a similar approach, requesting applicants supply financial information.

Access to PPP loans may not be distributed equally across other dimensions, either, though data to assess this are currently lacking. Lenders distributing PPP funds prioritized their own customers and those with lines of credit (in part because of the lack of clarity in the rules the US Department of the Treasury initially provided). Reports claim banks prioritized larger loan sizes first, resulting in class-action lawsuits.

Even before the pandemic, disparity in small business lending was widespread. Businesses with established relationships with large financial institutions are more likely to be white-owned and in high-income areas. The PPP fails to provide effective guidance and guardrails to disable this bias.

To address concerns, the new bill set aside $30 billion (less than 10 percent of the additional PPP funds) for community development financial institutions (CDFIs) and minority depository institutions, which are well positioned to support underserved small businesses and nonprofits. But this set-aside also includes banks with assets under $10 billion, despite the fact that 97 percent of all banks fall below this threshold. Community-based financial institutions will have to compete with thousands of banks to receive loans.

We may never know the extent of the PPP’s equity issues. The SBA elected not to collect (PDF) the demographic metrics they do on other guaranteed loans. The Borrower Information Form (PDF) for all SBA 7(a) programs collects information on the owners’ veteran status, gender, race, and ethnicity. Neither the PPP’s Lender Application Form (PDF) nor the Borrower Application Form (PDF) request this information, and neither the SBA nor the Treasury has signaled whether the new iteration of the program will fix this.

The PPP is a critical policy tool for an unprecedented economic collapse. The addition of funds is certainly needed, as is their quick distribution. But speed does not have to be at odds with efficiency. Absent a process that vets need, targets assistance to the hardest-hit firms and nonprofits, adds guidelines to counter bias and self-interest in lending institutions, and collects data about recipients to allow us to assess who gets funded and who doesn’t, the program will fail to adequately use the enormous funds devoted to it and may even worsen inequality in the long run.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.