<p>Victor Valenzuela, right, serves an espresso drink inside his ice cream truck on Friday, Sept. 20, 2013, in San Jose, CA. Valenzuela is one of 111 food trucks financed with microloans from the San Jose-based Opportunity Fund. The region leads the country for microlending as a growing echelon of would-be businesspersons who can't qualify for traditional bank loans meets money from cash-rich techies and firms. Photo by Marcio Jose Sanchez/AP.</p>

Politicians often tout owning a business as a way for Americans to advance economically. But a report recently released by the Federal Reserve Banks of Cleveland and Atlanta shows that limited access to credit may be keeping entrepreneurs in less-advantaged communities from achieving that goal. The findings reinforce and add to findings from an Urban Institute study of structural barriers to racial equity in Pittsburgh.

The Federal Reserve study compared responses of minority entrepreneurs with those of whites. By almost every measure, the firms owned by African Americans, Hispanics, and Asians were disadvantaged relative to the white-owned firms when trying to obtain loans to develop or expand their businesses. These findings reveal how hard it is for people to overcome structural racism and advance economically through business ownership. In many cases, treatment was worse for African Americans than for others.

Banks are likely to discourage entrepreneurs of color from even applying for a loan. Forty percent of African Americans reported being discouraged from completing an application, compared with 14 percent of white business owners. If they go through with the application process, entrepreneurs of color are less likely to obtain a loan than whites and, if they do obtain one, are less likely to receive the full amount requested (40 percent versus 68 percent).

Even among firms with over $1 million in revenue, African American–owned firms had more difficulty obtaining funds for expansion and were almost twice as likely to be turned away. This situation brings to mind the statement of an entrepreneur in Pittsburgh who told our research team,

“The second African American male [client of mine] had $2 million in his account, and he has been and probably still is, trying to get a loan from the bank for two or three years just for a working capital loan. It is not happening....The denial was that we like you, but we are not going to give you that money—smile in your face and tell you that, no real explanation as to why. I have seen the banks here give similar small business loans to white males in abundance.”

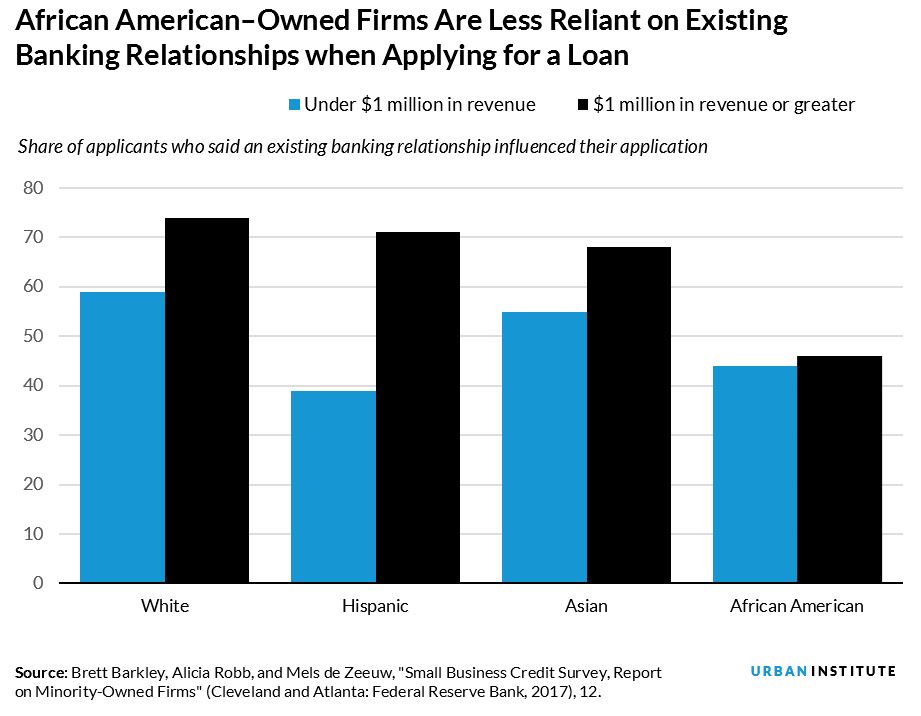

Experts in lending patterns point to the importance of trusted relationships in making loan arrangements work. Here again, firms owned by people of color are disadvantaged because the study shows that an existing relationship is more important (or more likely to be available) for white-owned firms than for firms owned by people of color. Even among African American–owned firms with over $1 million in revenue, less than half rely on an existing relationship when they apply for a loan, compared with nearly three-quarters of white-owned firms of similar size.

When minority-owned firms cannot get bank financing, they must rely on personal funds for working capital or for expansion. Eighty-six percent of the African American entrepreneurs surveyed by the Federal Reserve reported turning to their personal and family savings to help finance their businesses. Because African Americans and Hispanics tend to have lower personal wealth, they are limited in their ability to expand their businesses and pass on an enhanced wealth base to their children and grandchildren.

The Federal Reserve report indicates that one federal policy, the Community Reinvestment Act (CRA), seems to increase opportunity for some firms. This law requires banks to invest funds in communities in which they are located. Firms owned by entrepreneurs of color located in low-to-moderate-income areas have higher approval rates from large banks that are subject to CRA review. The action plan document issued with our report outlines additional public- and private-sector policies that could increase access to capital for minority-owned firms. These include providing additional funding to community development financial institutions that have more flexible lending arrangements than traditional banks and promoting crowdsourcing and crowdfunding.

But financing is not enough to make firms owned by people of color competitive in the marketplace. Other policies and strategies are necessary to overcome the effects of structural and overt racism, including programs to build management skills and grow business relationships that are more readily available to white-owned firms.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.