<p>Photo via Rawpixel/Getty Images.</p>

Following the onset of the Great Recession, the household sector’s debt service ratio (DSR) has been steadily declining and is now at its lowest level since the series began in 1980.

The DSR is the ratio of total required household debt payments to total disposable personal income (DPI) across all consumers. It is measured quarterly. Today’s low DSR, when combined with a lower level of housing debt relative to total home values, offers some good news: the housing sector likely poses less of a risk to the financial system than it did in the years leading up to the Great Recession.

The bad news: this does not mean that all households are better off. Although the decline in the DSR partly reflects the ability of many homeowners to reduce their payments amid lower mortgage rates, tight credit availability and a lack of affordable housing supply have kept some households from becoming homeowners. At the same time, total consumer debt payments have trended upward relative to DPI since 2013 and rental prices have been rising steadily.

Total DSR is at a historic low

The DSR peaked at 13.2 percent in 2007 and dropped to 9.7 percent in the second quarter of 2019.

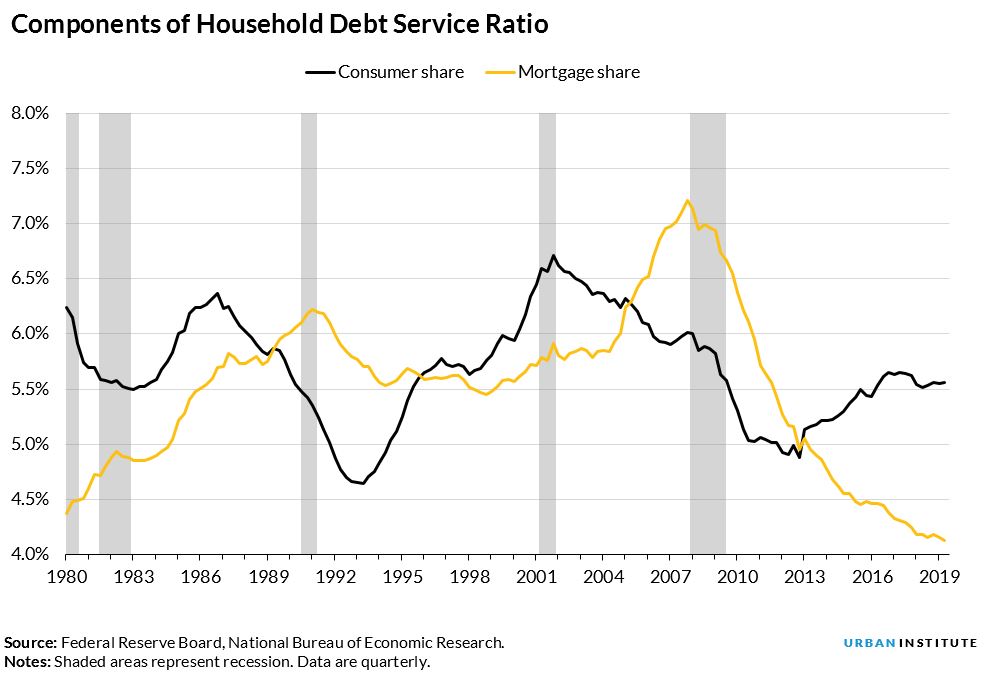

The household DSR is the sum of the consumer and mortgage DSRs. The consumer DSR is the total scheduled payments on revolving debt, such as credit cards, and non-revolving debt, such as automobile and student loans, relative to total disposable income across all households, whether they have the debt or not.

A decline in mortgage DSRs and, to a lesser extent, consumer DSRs, contributed to the drop in the overall household DSR between 2008 and 2013. The decrease in the consumer and mortgage DSRs during this period largely reflects household deleveraging in the wake of the Great Recession, characterized by higher default rates, tighter lending standards, softer aggregate demand, and greater risk aversion.

Another factor was the massive post-recession refinancing wave as mortgage rates fell, allowing homeowners to reduce their monthly mortgage payment and by extension, the mortgage DSR.

Since 2013, the low mortgage DSR has offset an increased consumer DSR

Since 2013, however, the consumer DSR has trended upward. The Federal Reserve Board’s Consumer Credit report, a source for the calculation of the consumer DSR, indicates that an increase in student loan debt was joined by growth in auto loan debt beginning in 2010 and an expansion in revolving debt (largely credit card debt) beginning in 2013.

Despite the upturn in the consumer DSR beginning in 2013, the continued decline in the mortgage DSR—now at its lowest level on record—has reduced the total DSR. In contrast, the increase in the mortgage DSR between 2004 and 2007 boosted the total DSR.

But aggregate trends mask the uneven experiences of individual households

The falling mortgage DSR partly reflects homeowners with a mortgage paying off their debt, but it also reflects the difficulties some would-be homeowners are having qualifying for a mortgage or finding an affordable home to buy. These factors are contributing to a record low mortgage DSR, but they are also limiting homeownership.

For renters, rents have increased steadily. As a result, a sizeable share of households has not benefitted from a reduction in the shelter costs that lower mortgage rates have delivered to homeowners with a mortgage.

Younger renter households in particular, who are at the beginning of their careers and are likely to also be carrying student loan debt, may actually be experiencing a higher debt service ratio.

The decline in total DSR appears to be telling a very specific story. Total mortgage debt payments amount to a much smaller portion of total DPI than ever before. But this partly reflects challenges in the mortgage and broader housing market that are limiting homeownership. Renters are also facing challenges amid rising rents and a lack of affordable inventory. Although total DSR is falling, many households are still struggling to get ahead.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.