<p>Photo by Suzanne Tucker via Shutterstock.</p>

Today, the $29.1 trillion value of the US housing market (in nominal terms) is at a historic high. Before the 2008 crisis, the market’s value peaked at $24.1 trillion.

But there’s a significant difference in today’s housing market: the mortgage debt level of US homeowners has remained relatively stable for more than a decade, while housing equity has been increasing continually since 2012.

Before the housing crisis, homeowners watching their home equity grow decided to cash in, tapping into their higher home values with home equity lines of credit (HELOCs) and cash-out refinances. We’ve shown that a spike in sloppily underwritten cash-out refinances was a major contributor to the housing crisis.

The low level of cash-out refinancing and HELOC debt today suggests that both banks and consumers are remembering the lessons from the past, contributing to a stable and secure housing market overall, and offering the housing market a substantial cushion in the event of a recession or an economic downturn.

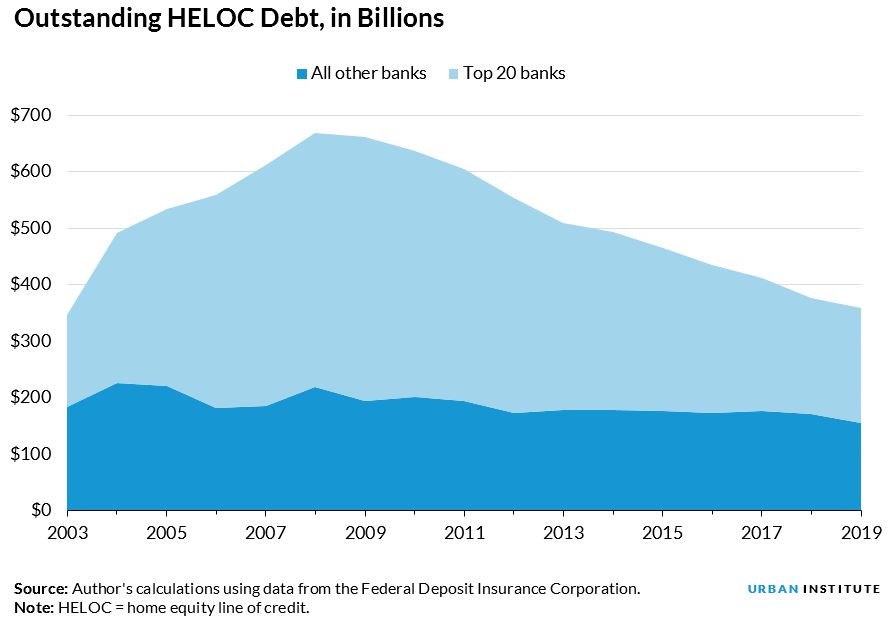

Although there is more outstanding mortgage debt than ever before at $9.4 trillion, the outstanding HELOC debt continues to shrink. In the second quarter of 2019, outstanding HELOC debt was less than $400 billion for the first time since 2004, according to the Federal Reserve Bank of New York. This is down from a peak of $714 billion in 2009. The decline in HELOCs reveals high risk aversion among lenders and consumer cautiousness.

HELOCs are mostly originated by banks to remain on their balance sheets. The 20 largest banks by assets have accounted for more than half of the total HELOC volume since 2003, and a closer look reveals that the big variations in HELOC volume at these banks over the past 15 years have altered the HELOC landscape.

The rapid HELOC expansion during the housing boom and the steep decline in the years following were mostly concentrated among these large banks.

HELOC losses have made big banks wary of HELOC lending

The recent decline largely reflects tighter lending standards at the big banks. The July 2019 Senior Loan Officer Opinion Survey on Bank Lending Practices asked respondents to describe the current level of lending standards relative to the range of their bank’s standards between 2005 and the present using the tightest and easiest points as reference points.

These questions are meant to ascertain whether standards are “tight” or “easy.” The figure below shows that the majority of large banks indicate that lending standards on HELOC loans remain tight, while the majority of other banks believe that standards are about average.

The two figures above reveal why the bigger banks have tighter lending standards today than the smaller banks: they are more risk averse thanks to the greater losses they suffered from HELOCs between 2009 and 2013. In 2008, the 3.4 percent net charge-off rate for the 20 largest banks was double the 1.7 percent rate all other banks experienced. Since then, however, the net charge-off rates for all banks have slowly converged to near zero.

Consumers also show less demand for HELOCs

A 2018 study by the Mortgage Bankers Association found lower borrower interest in HELOCs because of worries about overleveraging home equity and confusion about the tax advantages.

In addition, thanks to today’s low-rate environment, homeowners often use cash-out refinances instead of HELOCs to obtain funds for home improvements because the refinance delivers the funds needed in addition to locking in a lower fixed-mortgage rate. A cash-out refinancing raises the outstanding mortgage debt and leaves HELOC debt unchanged.

Refinancing volume is also down

Between 2003 and 2007, the total volume of cash-out refinances averaged $223 billion per year, ranging from $111 billion in 2002 to $320 billion in 2006.

In the years since 2008, cash-out refinance volume has averaged $52 billion per year, ranging from $25 billion in 2014 to $96 billion in 2008. In 2018, cash-out refinance volume reached $87 billion, but it’s on a slower pace over the first three quarters of 2019. (See page 10 of our October chartbook.)

With aggregate home values at a record high and mortgage debt remaining steady, partly due to low levels of HELOC activity and cash-out refinancing, homeowners’ equity as a share of total home values sits at 64 percent, its highest level since 2002, before the excesses of the housing boom and the resulting housing crisis.

Housing debt itself amounts to 36 percent of total home values, making for a more stable housing market in aggregate and offering the housing market overall greater protection against the next economic downturn.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.