<p>Cavan Images/Getty Images</p>

This week, the president signed into law a $900 billion pandemic relief stimulus package that includes supplemental unemployment insurance, another round of direct payments to Americans, and more money for the Paycheck Protection Program. Notably missing from the legislation is an extension of the guaranteed paid sick leave mandate set to expire at the end of the year.

The Families First Coronavirus Response Act (FFCRA) passed in March included the first federal legislation providing paid leave, which covered workers who are ill or quarantining because of the coronavirus or caring for children whose schools and daycares were closed. One study shows the paid leave provision in the FFCRA may have prevented more than 15,000 cases of COVID-19 per day by allowing sick workers to stay home.

Before the FFCRA, paid sick leave in the United States was a patchwork of state and local laws (PDF) and voluntary employer-provided benefits. Research widely suggests paid sick leave has significant benefits (PDF) for workers, public health, employers, and the economy. Many employers provide these benefits voluntarily. However, one concern cited by opponents of national paid sick leave proposals is the cost to small businesses, which are excluded from many state and local policies. These exclusions are more likely to affect women, essential workers, workers of color, and lower-wage workers.

In our new brief, we explore a national policy option that would use a modified version of the FFCRA reimbursement system to allow employers to anticipate paid sick leave costs and access federal reimbursement more quickly. For purposes of this blog post, we define paid sick leave as a benefit that allows workers to take time off from work to care for their own health or the health of a family member, including preventive care, such as vaccinations or cancer screenings.

How a modified FFCRA reimbursement system could work

The FFCRA mandates two weeks of paid sick leave for workers recovering from illness, quarantining because of exposure to the coronavirus, or caring for someone for reasons related to COVID-19. It also provides an additional 10 weeks of paid leave for child care necessitated by school or daycare closures. However, the law excluded workers for companies with 500 or more workers, businesses with fewer than 50 employees, and health providers and emergency responders whose employers choose not to include them. This excluded potentially tens of millions of workers.

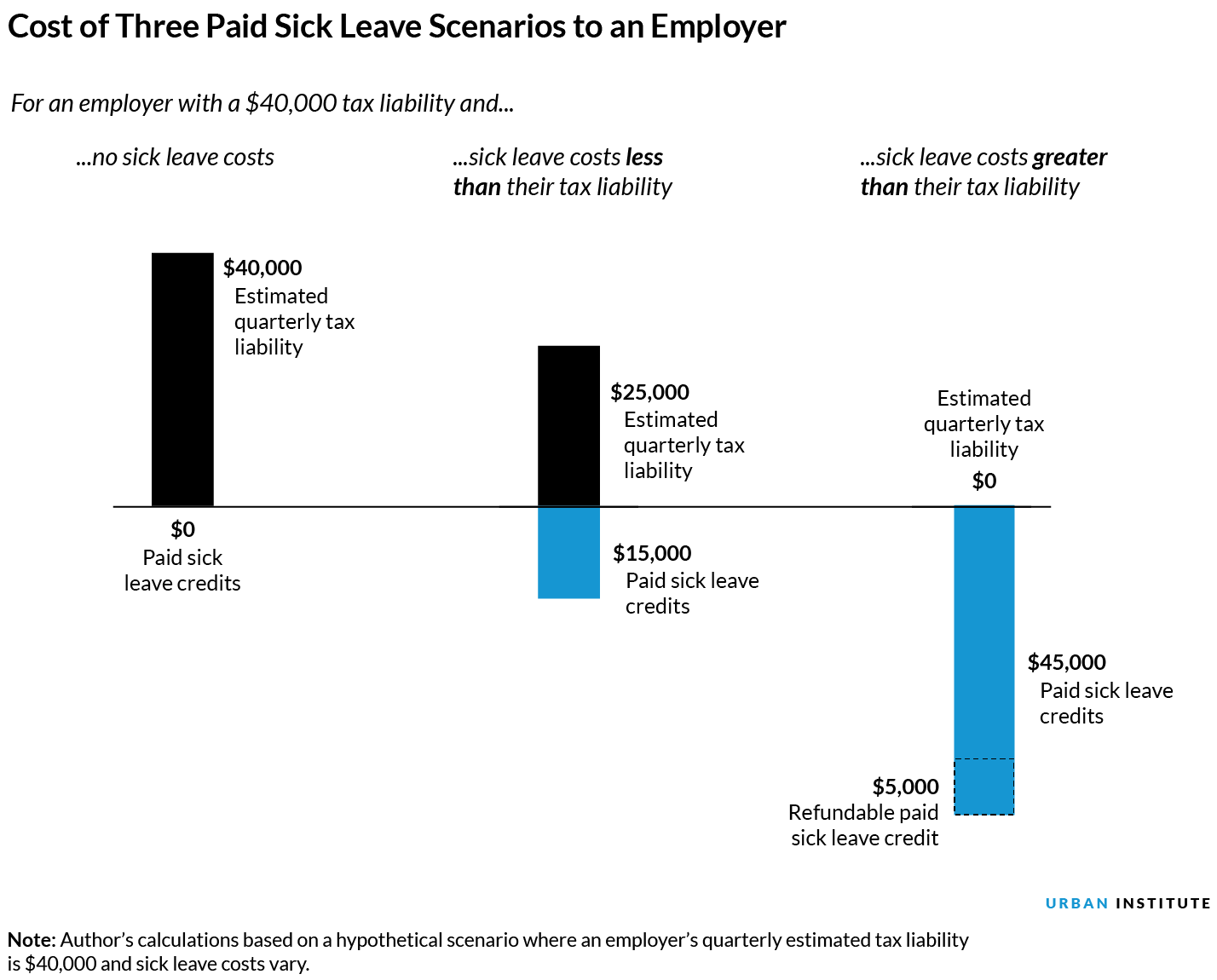

The FFCRA provided for full federal reimbursement of employers’ costs through two mechanisms. First, employers can reduce their federal tax withholdings and report it on their quarterly tax return. Internal Revenue Service (IRS) guidance indicates employers may reduce withholdings of federal income tax, the employee share of Social Security and Medicare taxes, and the employer share of Social Security and Medicare taxes with respect to all employees. The employer must then also file the new Form 7200 with the IRS for payment of an advance refundable credit.

These mechanisms could provide a useful framework for a future permanent policy to reimburse a portion of small employers’ costs of providing paid sick leave. To access the reimbursement, employers could be allowed to reduce their estimated tax withholdings based on projected costs. If their costs exceed their estimated tax liability, they could apply for an advance refundable credit for those excess costs.

To administer the federal reimbursement to some small employers, the US Department of the Treasury could expand and improve on the FFCRA model. Under the FFCRA, employers reduce their withholding of federal employment taxes to cover 100 percent of the costs incurred for providing paid sick leave, with the Treasury reimbursing the affected programs. If their costs exceed their total tax liability, they could apply for an advance refund equal to their excess paid leave costs.

Although this mechanism ensures employers receive full reimbursement for their costs, it can create a delay between when the costs are incurred and payment is received, imposing potential burdens on some employers. To address this concern in a long-term policy, the Treasury could establish a prospective reimbursement system under which employers could retain a portion of their tax withholdings to offset expected sick leave costs.

Addressing employer costs

In addition to cost concerns, employers and organized business groups often argue that small businesses face special difficulties in finding replacements for sick workers. However, businesses must already find ways to fill in for sick workers. And requiring sick employees to work can carry other serious costs to employers, such as higher risk of job-related injuries, and costs to public health.

In a more comprehensive federal paid sick leave policy, reimbursements could be used to offset costs for small employers. For example, the nonrefundable tax credit for some health insurance costs is available to employers with 25 or fewer employees whose average compensation does not exceed $50,000. Other options include limiting federal reimbursement to financially struggling small employers that incur costs above a specified level or limiting reimbursements to sick leave costs in excess of average levels.

Looking ahead

The COVID-19 pandemic has highlighted the vulnerabilities in our system of state, local, and voluntary employer policies, as well as health disparities among workers, much of which stem from long-standing systemic racism that puts lower-income workers and workers of color at higher risk of being exposed to and experiencing adverse consequences from the coronavirus.

The FFCRA provided the first-ever paid leave requirement in the country, and when it ends on December 31, millions of Americans will be faced with the dilemma of losing a paycheck (or their jobs) or going to work while sick, potentially worsening our public health crisis. Women, lower-income workers, and workers of color will be disproportionately affected by the expiration of this mandate.

Lawmakers missed a critical opportunity to help these workers by failing to extend the emergency paid sick and family credits in the FFCRA. Future relief efforts could consider modified options like the one we explored, which take advantage of existing mechanisms and could help employers protect millions of workers during a future crisis.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.