<p>In this Friday, May 27, 2016, photo, Joe Ross works in his office in San Francisco. When Ross graduated from law school in 2007, his debt was more than $160,000. Including his wife's school loans, the couple, who have three children, owed more than $200,000. Photo by Eric Risberg/AP.</p>

The PROSPER Act, the House Republicans’ proposal for reauthorizing the Higher Education Act (HEA), changes to the federal student loan program to simplify repayment options, but will result in longer repayment terms, especially for low-income borrowers.

PROSPER introduces a new income-based repayment plan that would be the only alternate to the standard repayment option for new borrowers, replacing current options, such as PAYE (Pay as You Earn) and REPAYE (Revised Pay as You Earn).

The PROSPER plan requires that borrowers pay 15 percent of their discretionary adjusted gross income (the amount above 150 percent of the federal poverty level) toward their student loans. Borrowers who have no discretionary income must still pay $25 a month toward their loans, though they may request a reduced payment of $5, for up to three years, because of financial hardship.

PAYE and REPAYE, the most recent IBR plans, require that borrowers pay 10 percent of their discretionary income (and nothing if they earn below 150 percent of the federal poverty level). In these plans, the unpaid amount is typically forgiven after 20 or 25 years. But under PROSPER, there would be no debt forgiveness. Borrowers would pay until they pay the amount they would have repaid under a 10-year standard plan.

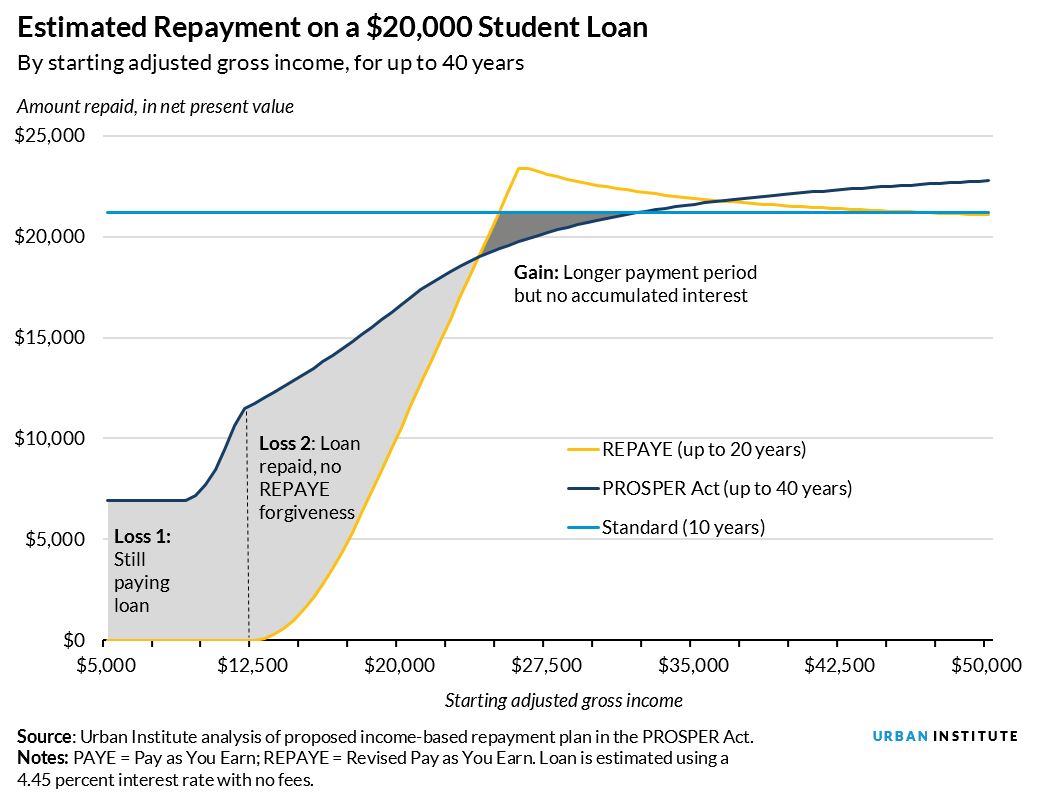

I estimate how much borrowers at different income levels would pay under REPAYE, PROSPER, and the standard plan, reporting all amounts in net present-value dollars, which adjusts for the fact that a dollar is worth more to a person now than in the future. Because payments could be spread over 20, 30, 40, or more years, it is important to consider not just how much borrowers pay but when they make those payments.

Download the methodology here.

When we look at the estimated repayment on a $20,000 undergraduate student loan under each of these plans, the differences become clear. The loss of debt forgiveness increases the payments low-income borrowers make. The mandatory $25 monthly payment under the PROSPER proposal means that all borrowers, even those with very low incomes, must make payments toward their student loan debt.

In this scenario, borrowers who earn less than $12,000 a year after graduation (Loss 1 in the figure) are still paying down their loan after 40 years, though the debt would have been forgiven after 20 years under current plans. Roughly 21 percent of 25-year-olds in 2015 with at least some college fall into this bucket, although we don’t know how many of them hold educational debt or how much. Borrowers with starting incomes of $12,000 to $23,500 (Loss 2; roughly 23 percent of 25-year-olds with some college) will have repaid their loans over 15 to 40 years but would have been eligible for some loan forgiveness under REPAYE.

Borrowers earning $24,000 to $32,000 after graduation (Gain), benefit from having longer to repay without accruing additional interest. Those who earn more than $32,000 would likely not use the plan because they would pay more (in net present-value terms) than under a standard plan.

I limit the repayment window to 40 years, but there are scenarios where low-income borrowers could pay off their debt over more than 40 years. It is unclear whether mandatory $25 payments would continue into a borrower’s retirement, but this is a scenario policymakers must consider. Borrowers with very high debt and modest starting salaries ($20,000–$35,000) may also be at risk for long repayment periods.

The PROSPER plan changes the math for potential student borrowers. Those with very low incomes will still be required to put $300 toward their loans each year. Further, without forgiveness, borrowers face the prospect of paying off their loans for more than 20 or 25 years.

The plethora of income-based repayment plans may call out for simplification, but low-income borrowers are likely to be worse off under the PROSPER plan. Because student loans typically cannot be discharged in bankruptcy, many low-income borrowers might be required to make payments for the rest of their lives. Policymakers need to weigh the benefits to taxpayers of collecting additional loan payments against the burden that repayment without the possibility of forgiveness would place on borrowers.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.