<p>(saintho/Getty Images)<br />

</p>

Refinancing is one of the most effective ways to reduce homeownership costs and has been a powerful wealth-building tool throughout time. Lowering mortgage payments—the largest home expense for most households—enables many to reinvest in their home through home improvements or to make other wealth-generating investments. Some households may reduce the term on their mortgage, helping them build housing wealth more quickly.

But not everyone can reap the benefits of refinancing. In fact, the least affluent borrowers—especially manufactured home (MH) borrowers—face the greatest obstacles to refinancing. This exacerbates homeownership inequities, but it doesn’t have to be this way. Federal policymakers and the housing industry could mitigate these trends.

Manufactured versus site-built home borrowers

2020 Home Mortgage Disclosure Act (HMDA) data indicate that the median income of a site-built home borrower is $91,000 but is only $53,000 for an MH borrower whose loan is secured by the land (a real estate loan) and $51,000 for chattel borrowers (loans secured by the home only). In addition, real estate loans usually require the home be permanently installed on an approved foundation, but chattel loans do not.

MH homeowners with mortgages secured by both the home and the land are less likely to refinance than borrowers whose loans are secured with site-built homes, despite evidence that manufactured homes secured by real estate loans appreciate as well as site-built homes. And MH homeowners with chattel loans rarely refinance because they have fewer options to do so.

This means MH borrowers, who have lower incomes than site-built housing borrowers, cannot take advantage of the lowest mortgage interest rates in several generations. More research is needed to better understand the reasons for this.

MH chattel loans are rarely refinanced

Lenders don’t need to reduce the chattel loan interest rate because competitive pressures in the market are minimal; the industry has only a few lenders who specialize in MH, and they dominate the business. This means chattel loans are rarely refinanced, and when they are, it is usually to reextend the term or because the borrowers’ credit has improved.

Moreover, a different lender may be reluctant to lend for the initial amount because the unit depreciates when it is driven off the lot. The US Department of Housing and Urban Development’s Title 1 permits the refinancing of chattel loans without an appraisal, but activity in this channel is low, with few lenders participating. The cap on the maximum loan amount is $69,678, too low to be useful for most borrowers. The average price of new MH in 2020 is $87,000, excluding transportation or installation costs. Even so, the relatively few chattel refinances are disproportionately Title 1.

Several websites urge chattel borrowers to consider retitling their MH as real property so they can take advantage of MH mortgages. But this requires that the borrower own the land and be willing and able to encumber it and that the home be permanently affixed to the property, criteria with which many chattel loan borrowers cannot comply.

MH real estate loans also refinance less than their site-built counterparts

These barriers don’t exist for real estate MH loans. In fact, MH loans have similar profiles to mortgages on site-built homes in a couple key ways: both normally have 30-year terms, and their decline in mortgage interest rates between 2019 and 2020 was roughly similar. This means the raw refinancing incentive doesn’t account for the differences between them.

The two main reasons loans on MH real estate are less likely to refinance than their site-built counterparts—smaller loans and bigger fees—produce less of a cost savings.

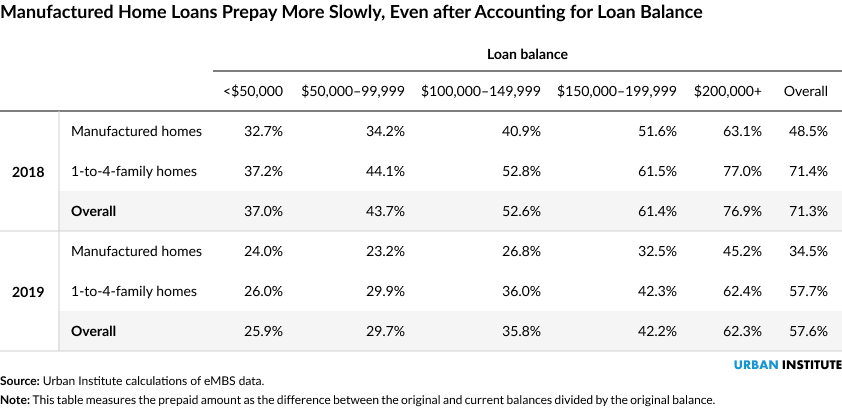

As one study noted, the smaller loan amount is a large part of the explanation for the more limited refinancing but is not the whole story. Small site-built homes are also less like to prepay than their larger counterparts, but even after holding loan size constant, data still show MH is less likely to refinance. This is most evident when comparing the amount of 2018 and 2019 Fannie Mae origination that has been paid off for manufactured housing mortgages versus their site-built counterparts.

Though the paydowns reflect both movers prepaying their mortgage and schedule amortization and curtailments, the overwhelming majority are because of refinancing.

What explains this difference? First, the extra up-front costs from refinancing MH rather than a site-built property are significant. The government-sponsored enterprises (GSEs) impose a 50 basis-point up-front fee in the form of a loan-level price adjustment on all MH purchase and refinance mortgages.

In addition, borrowers with lower credit scores pay additional fees. Loan-level price adjustments requires borrowers with a loan-to-value ratio of more than 75 percent but not over 80 percent and a credit score of 680 to 700 to face a 175 basis-point up-front fee, whereas borrowers with a credit score at or above 740 in the same loan-to-value range would face a 50 basis-point fee.

This disadvantages MH borrowers, who have lower credit scores than their site-built counterparts. A Consumer Financial Protection Bureau analysis of 2019 HMDA data indicates that site-built purchase loans have a median credit score of 739, versus 691 for MH mortgage loans and 676 for chattel loans. Thus, a typical MH borrower would need to pay up-front charges of 225 basis points (175 + 50) to cover the two loan-level price adjustments; this is an extra charge of roughly 45 basis points a year.

As a result of the smaller loan size and the extra fees, MH borrowers see fewer savings from refinancing.

Policy implications

Today’s historically low interest rates could help more vulnerable MH owners gain financial breathing room. The federal government and housing industry can take several actions to ensure MH borrowers can take advantage of refinancing opportunities:

- The GSEs could drop loan-level price adjustment fees for financially vulnerable borrowers and even consider dropping them for all refinancing, because the borrower already paid these charges when they took out the original purchase loan.

- The housing industry can make MH homebuyers more aware of the lack of refinancing opportunities in chattel before taking out a loan. MH owners who own both the structure and the land often take out a chattel loan because the probability of denial is lower, the closing time is shorter, or they don’t want to encumber the land. When a borrower who can take out either a chattel or mortgage loan chooses a chattel loan, they are essentially giving up a valuable option to refinance in the future, an often-overlooked consideration in the original financing decision.

Inequitable refinancing opportunities are deepening homeownership gaps and economic divides. This period of low interest rates offers a chance to reverse this trend.

The Urban Institute has the evidence to show what it will take to create a society where everyone has a fair shot at achieving their vision of success.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.