Photo by Lindasj22/Shutterstock.

Manufactured housing is 35 to 47 percent cheaper per square foot than site-built housing, yet the number of manufactured homes shipped each year has decreased from averaging 242,000 a year between 1977 and 1993 to just 92,500 units in 2017.

Restrictive or unavailable financing, restrictive zoning, and the view that manufactured homes do not appreciate as much as site-built homes have limited this type of housing. A recent government report, however, reveals that manufactured homes may actually appreciate at levels similar to site-built homes.

The Federal Housing Finance Agency (FHFA), the conservator that oversees the government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac, recently published its extensive quarterly report on US house prices and included data on manufactured housing (MH) for the first time.

The FHFA’s new MH index, still in the experimental stage, indicates that the prices of the MH purchased by the GSEs perform similarly to those of site-built properties. Although there are limits to what the data can tell us, the index suggests a need to reevaluate the presumption that manufactured homes do not appreciate at the same rate as site-built homes.

A closer look at the FHFA index

The FHFA calculates its price indexes using a repeat sales methodology, which notes the change in prices between repeat sales of the same property. The indexes are constructed on the state level and weighted to roll up to the national index. State-level indexes were not constructed for the MH indexes, as there are fewer transactions (the sample is limited to MH loans titled as real property and guaranteed by the GSEs); the national-level indexes were formed by pooling all transactions together.

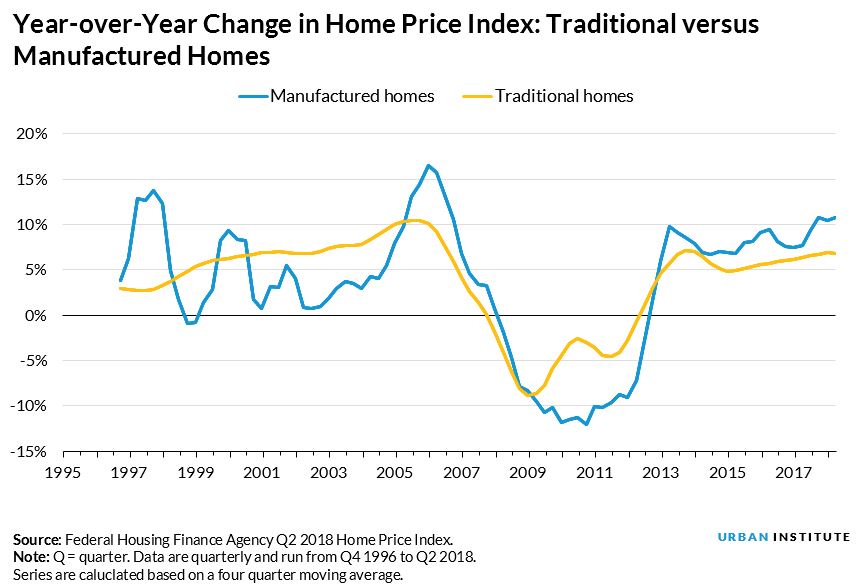

The figure above compares the FHFA’s national purchase index through time with the new MH index. Clearly, MH is more volatile than the national index for site-built homes—declining more between 2005 and 2012 and increasing more since then. And the MH index is usually slightly lower than the site-built index.

The figure above shows the two indexes expressed as year-over-year home price changes, which show the higher volatility of the MH index. Although the more limited number of MH observations could explain part of this, we have eliminated quarterly fluctuations and are looking at year-over-year changes.

More importantly, if we look at the average change over the entire period that the FHFA tracks both indexes, the national index has an average annual growth rate of 3.8 percent versus the MH index at 3.4 percent. These results are not that different, although the manufactured homes, again, seem to appreciate more slowly.

How geography can understate the strength of the manufactured housing market

The MH market is underrepresented in some states with robust home price appreciation.

California is close to 18 percent of the housing market but accounts for only 4 percent of the MH market in terms of units shipped. And since 2012, the average annual appreciation in California has been 9.43 percent compared with a national average of 5.87 percent.

In comparison, the top five MH states—Alabama, Florida, Louisiana, North Carolina, and Texas—which have accounted for 41 percent of the MH market since 2011, have average price appreciation below the national level, according to the FHFA indexes.

MH is also underrepresented in center cities, which have experienced the most rapid home price appreciation, and overrepresented in outer suburbs and nonmetropolitan areas. There are few manufactured homes in downtown San Francisco or Manhattan.

Accordingly, our comparison disadvantages MH versus a measure in which we compare properties in the same area.

Given that the appreciation rates for MH were only marginally lower than the rates for site-built homes, and given the tendency for geographic differences to understate MH performance, we believe the appreciation of MH and site-built homes are actually similar after adjusting for geographic differences.

Is the manufactured housing sector performing like the site-built sector?

One must approach that question carefully.

The GSEs underwrite mortgage loans on MH only when both the structure and the land are financed. Much of the financing in the MH market, on the order of 80 percent, is done on the structure only, through chattel lending.

We would not expect the same rate of home price appreciation on structures alone, as land generally appreciates more than structures. Data from the Lincoln Institute of Land Policy indicates a total appreciation rate of 204 percent on land and 87 percent on structures from 1995 to 2016.

The GSEs underwrite a small share of MH originations, and their production is mostly high-end. From 2013 to 2017, the GSEs underwrote just 8 to 13.5 percent of the MH market by loan count compared with 45 to 49 percent of site-built originations.

And in 2017, the average GSE MH purchase loan was $130,000 versus $95,000 for all purchase originations captured by Home Mortgage Disclosure Act data. A likely explanation for most of the differential is that land is included with the structure in GSE loans.

The perception that MH is a deteriorating, not appreciating asset, makes it harder to obtain financing for manufactured homes. The FHFA’s important new MH index suggests that manufactured homes that include the land may actually appreciate at rates similar to site-built properties.

But the geographic concentration of the MH sector and the small GSE MH footprint make it difficult to apply the FHFA’s MH index to the entire market.

This index is a huge step forward in increasing our knowledge of the MH market. We hope it will be produced regularly and enhanced over time. In particular, it would be useful to include state-level indexes for states with a significant MH presence.

Given the limited observations, a hedonic analysis that estimates the value of different housing characteristics would be extremely useful.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.