<p>Photo via Shutterstock</p>

The overwhelming majority of new homeowners between 2010 and 2030 will be minorities, a group traditionally underserved in the housing market. Minority homeowners today, however, have significantly lower rates of homeownership than white homeowners.

If we want to maintain a healthy housing market, we need to find effective ways to help minority households become sustainable homeowners.

NeighborWorks America, a nonprofit that supports approximately 250 affiliated housing and community development organizations helping families across the country, is working toward that end. In 2015, NeighborWorks America helped 21,700 families become homeowners through their nationwide homeownership education and counseling program.

According to our recent study, the program successfully serves traditionally disadvantaged borrowers and significantly improves their chances of staying current on their mortgage payments and, thus, remaining in their homes.

How effective is the program?

A previous study of the NeighborWorks program found a nearly one-third drop in the likelihood of serious mortgage delinquency when consumers received prepurchase counseling and education. That research was based on mortgages originated from 2007 to 2009, when the housing crisis unfolded and the credit box began to tighten.

Our report examined NeighborWorks loans originated from 2010 to 2012, when the housing market struggled to recover and credit tightened considerably. We wanted to see whether the positive impact of NeighborWorks’s counseling services on mortgage performance was sustained under very different economic conditions.

Our research shows that buyers who received homeownership education and counseling from NeighborWorks achieved significantly better loan performance than comparable buyers without NeighborWorks services, even in a tight-credit, low-default housing market. Holding all other things equal, the delinquency rates of 90 days or more for NeighborWorks loans were 16 percent lower than rates for non-NeighborWorks loans.

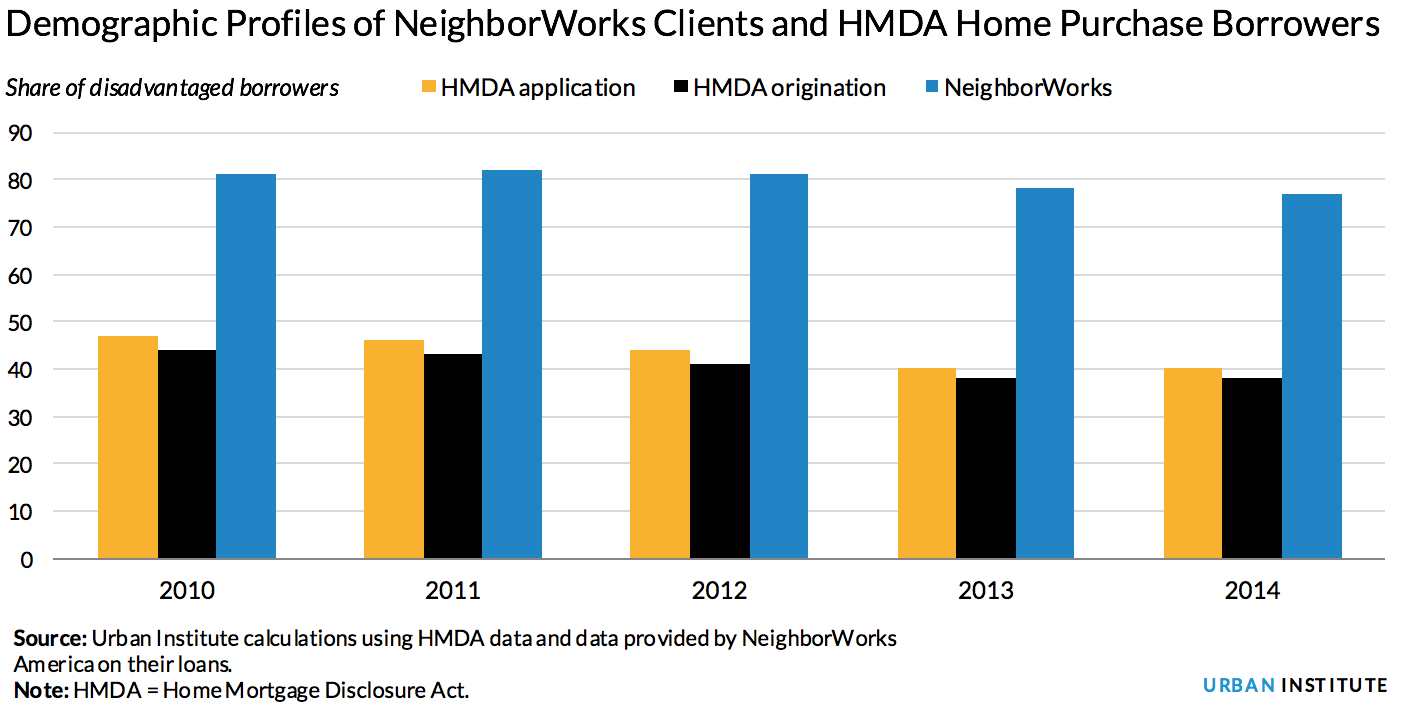

Who is served by the program?

NeighborWorks’s program works even in today’s tight-credit, low-default housing market, but whom does it serve? Our research shows NeighborWorks’s program reached traditionally underserved borrowers, including African Americans, Hispanics, low-income families, and families headed by female borrowers. Among NeighborWorks clients, we found the following:

- The share of African American borrowers was almost three times higher than the share among general mortgage applicants and borrowers. The share of Hispanic borrowers was twice as high.

- The share of very low income borrowers was five times higher than the share among general mortgage applicants and borrowers. The share of low-income borrowers was twice as high.

- The share of female borrowers among NeighborWorks clients was nearly twice as high as the share among general mortgage applicants and borrowers.

In total, the share of traditionally underserved clients in NeighborWorks’s program was almost twice as high as the share among general home purchase mortgage applicants and borrowers.

Where can we maximize these benefits?

We recommend that counselors focus on locations with the most rejected purchase mortgage applicants and the highest real denial rate. Metro areas at the top of the list include Chicago, Miami, and Los Angeles.

Our study confirms that NeighborWorks America’s homeownership counseling and education services can help minority and other disadvantaged households obtain and maintain homeownership. We should target the program to areas with high denial rates, where the housing counseling and education services can be of most help.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.