<p>(Sundry Photography/Getty Images)<br />

</p>

Despite robust multifamily construction activity overall, the share of these units built for sale last year was less than 5.4 percent—almost the lowest level in half a century. The rest were rental units. This trend has persisted even though demographic patterns are boosting the need for condos, and the shortage is adding to concerns about the lack of affordability in the homebuying market.

Condos can present a key path to first-time homeownership, but a combination of federal financing issues and local defect laws have contributed to a lack of multifamily units for sale. Although the issues are complex, it is critical to break down these barriers to developing more affordable housing supply and expand homeownership opportunities to more families.

Multifamily for-sale construction is near historic lows

Multifamily construction for sale is historically low, whether measured as a share of all new multifamily units (constructed for sale and for rent) or as a share of all new housing units for sale (single-family plus multifamily units). Multifamily construction built for sale accounted for only 5.4 percent of all multifamily starts and only 2.7 percent of all single-family and multifamily home construction for the first three quarters of 2021.

This is not a pandemic-related phenomenon; multifamily construction for sale has been declining since the Great Recession, and the approval time for new construction means it is unlikely the pandemic significantly affected volume.

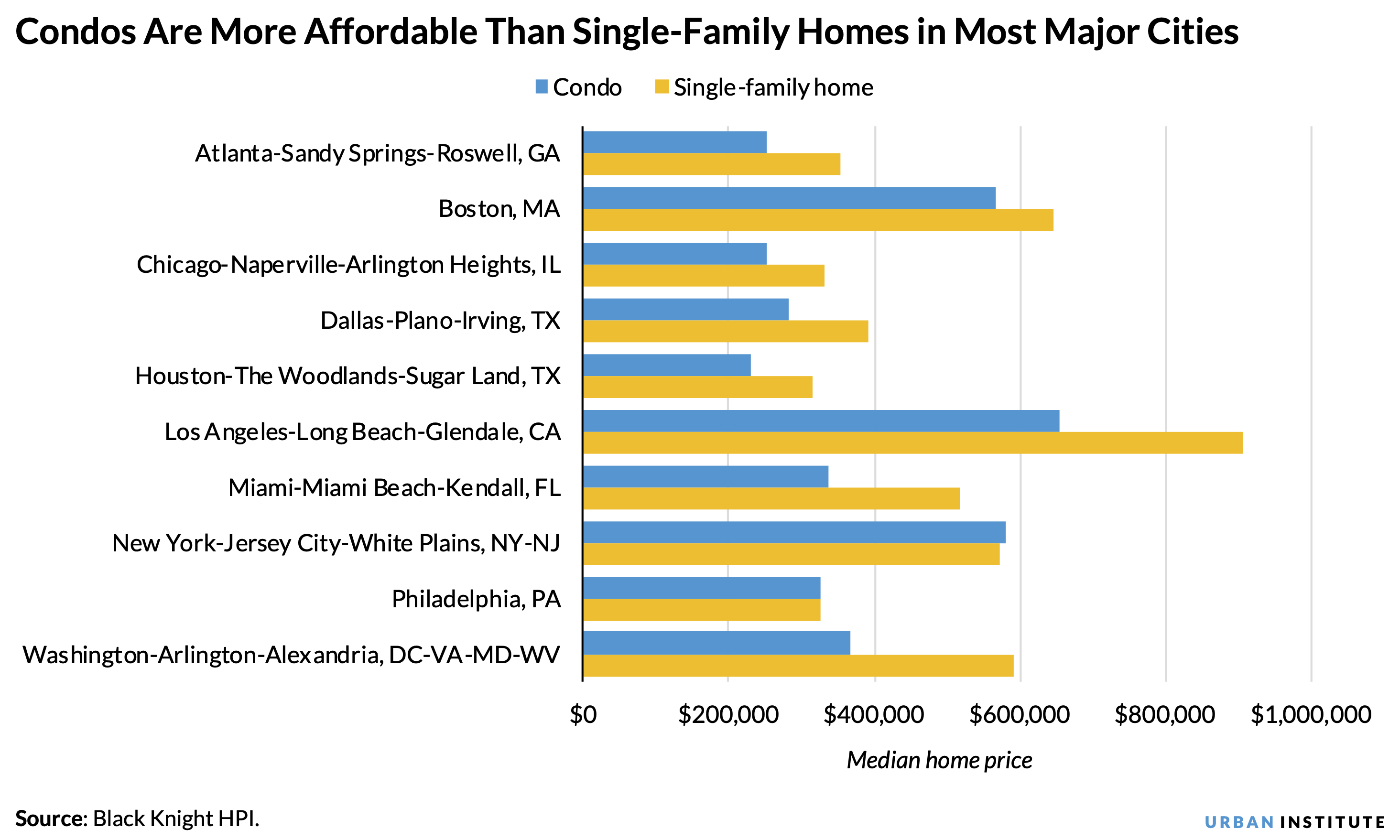

Condos are more affordable than single-family homes

In every major city except New York and Philadelphia, condo and co-op prices are significantly lower than single-family home prices. During the pandemic, the gap between single-family and multifamily home prices has increased as families have traded location for space, leaving condos as the far more affordable choice.

Because condos and co-ops are generally more affordable, they tend to help first-time homebuyers step onto the first rung of the homeownership ladder. These buyers often use the equity on their condo to then purchase a larger single-family home. When we look at government-sponsored enterprise purchases with a mortgage, about 60 percent of condos and co-ops are purchased by first-time homebuyers; for single-family homes, the share is around 40 percent (link corrected February 1, 2022).

Demographic trends favor more robust condo development

Condos and co-ops also tend to better match long-term demographic changes. The share of one-person households has increased from 12 percent of all households in 1960 to 28 percent today. The share of two-person households has increased from 28 percent to 35 percent.

Owner-occupied multifamily units tend to have a disproportionate share of one-person households. Approximately 20 percent of all owner-occupied single-family housing is occupied by a one-person household; that share is 45 percent in owner-occupied multifamily housing. Approximately 35 percent of both owner-occupied single-family and multifamily housing consists of two-person households, while larger households disproportionately live in single-family housing.

The growth in one-person households over the past several decades should have provided the basis for more robust growth in multifamily housing than in single-family housing, but that has not been the case.

Why the disconnect?

Condo production has been low for two main reasons. First, financing constraints are an issue for both the sponsor and the builder.

Successful condo development requires that the sponsor be able to sell the units quickly, which requires that potential unit buyers either have cash on hand or can obtain financing. Few owner-occupants, especially in more affordable buildings, will be able to purchase with cash, and with credit tight for first-time homebuyers, this uncertainty is a concern for sponsors.

But sponsors cannot solve that problem by selling to investors, who are more likely to be able to buy with cash. For example, a potential condo buyer cannot get a Federal Housing Administration (FHA) loan or a Fannie Mae or Freddie Mac loan unless (1) at least 50 percent of the condo units are owner-occupied and (2) no more than 15 percent of the units in the complex have association dues that are more than 30 days behind.

In addition, the FHA requires no more than 10 percent of the units in the complex secure existing FHA loans, further limiting access by the low-income borrowers the FHA typically serves. And Fannie Mae and Freddie Mac require that no single entity can own more than 2 units in projects consisting of 5 to 20 units and 20 percent of units in projects consisting of 21 or more units, and that the homeowners’ association is not named in any lawsuits.

In addition, defect litigation can substantially increase the cost of insurance and the riskiness of a condo project.

There is a statute of limitations on construction defect claims, which varies by state and by type of defect. For example, in New York State, construction defects are covered for one year after the warranty date. Plumbing, electrical, heating, cooling, and ventilation systems are covered for two years, and material defects are covered for six years. As a result, the condominium association has an interest in raising defect claims promptly. These claims are common on new buildings, and they have a chilling effect on a sponsor’s willingness to build for owner-occupants. And while this litigation is under way, it is virtually impossible to sell or finance new units in the building.

Because of the higher risk associated with condo development, the builder pays a higher rate to finance the condo construction than would be the case on a rental unit, and the lender demands a higher return for the higher risk.

These federal financing constraints and local defect laws make it far less risky for multifamily developers to build rental housing than for-sale construction and have limited the construction of condos and co-ops. But amid growth in single-person households and affordability concerns in the market, the need to address these challenges and build more of this type of housing has never been greater.

Overcoming these obstacles would require government and government-sponsored agencies at the federal level to ease financing restrictions and would require states and localities to reevaluate defect laws. Although these defect laws provide valuable protection to condo owners, it may be possible to provide this protection in a form that does not discourage new condo production. This challenge reflects another instance where a concerted partnership among all levels of government is needed to overcome barriers to affordable homeownership.

The Urban Institute has the evidence to show what it will take to create a society where everyone has a fair shot at achieving their vision of success.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.