<p>Photo by Jeffrey Greenberg/UIG via Getty Images.</p>

Correction: The mortgage amount for the buyer of a $1.2 million home was incorrectly listed as $9,600,000 in the table below. The correct amount is $960,000.

The recently passed Tax Cuts and Jobs Act represents the most sweeping change in tax legislation since the Tax Reform Act of 1986. We examined what these changes mean for the housing market and concluded that while most taxpayers will pay lower taxes, allowing them to save for a home more easily if they choose, the increased standard deduction means fewer taxpayers will itemize. The reduction in tax rates also suggests less of a benefit for those who do itemize.

The net result is that renting will look more attractive than homeownership to many Americans in 2018 and beyond.

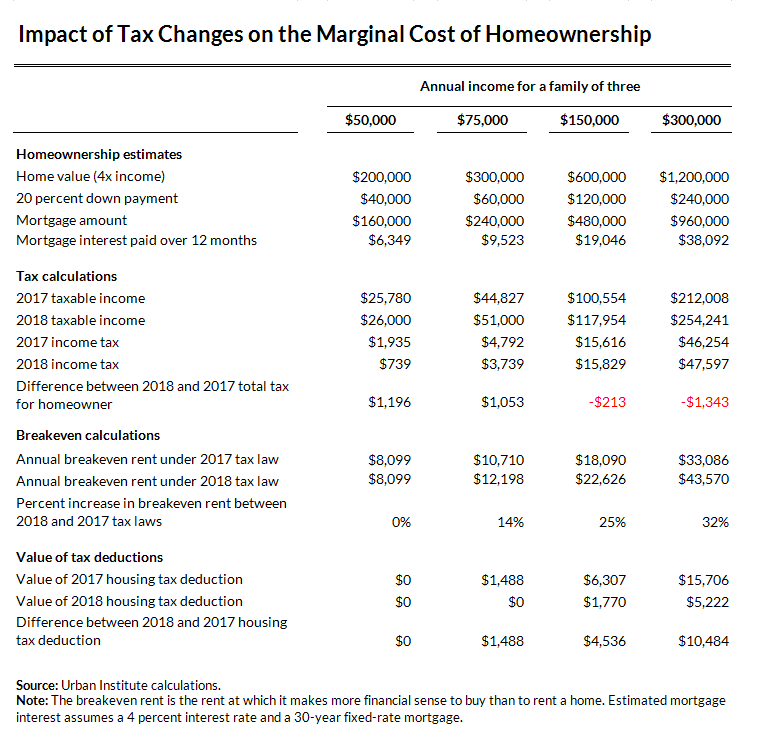

To illustrate our conclusion, we provide an example of four families who earn $50,000, $75,000, $150,000, and $300,000 a year. We make the following assumptions for each family:

- All are families of three, buying a home valued at four times their income

- Each family puts down 20 percent and takes out a mortgage for the balance

- The mortgage interest rate is 4 percent (close to the rates prevailing as we write this)

- Property taxes are 1.5 percent of home value

- Homeowners insurance is 0.375 percent of home value

- Repairs and maintenance are 1.5 percent of home value

- Expected appreciation is 3 percent of home value

- Families who rent must have rental insurance

Next, we look at the total tax bill under the old (2017) and new (2018) laws (assuming state income taxes are 5 percent on all amounts over $25,000 and charitable giving is 2 percent of income), as well as the difference in the tax advantages to owner-occupied housing in the 2017 plan versus the 2018 plan.

We then compute the rent that results in the same all-in cost of housing. In effect, we are computing the user cost of owner-occupied single-family housing.

The following outcomes emerge.

A family with $50,000 annual income

This family takes advantage of the standard deduction under both tax plans. Its taxable income is not very different ($25,780 versus $26,000) under the 2018 plan, because, even though the standard deduction is higher ($24,000 versus $12,700), the family loses the $4,050-per-person standard deduction.

The total tax bill is $1,196 lower, as the effective tax rate is lower and, most importantly for this family, the child credit is increased from $1,000 to $2,000. Because the family was using the standard deduction, there is no impact on a homeownership-versus-rental decision.

A family with $75,000 annual income

This family would have itemized under the 2017 tax code but would not itemize under the 2018 tax code with the increase in the standard deduction. Even though the new taxable amount is slightly higher ($51,000 versus $44,827) under the 2018 law (because of the loss of the personal exemption), the tax bill is $1,053 lower because of the cut in the marginal tax rates and the increase in the child credit.

Although these funds could be put toward a down payment on a home, the savings from homeownership have been reduced by $1,488 for the year ($124 per month), as the family is not itemizing, so no tax savings arise from the mortgage or from property taxes.

Under the 2017 tax code, when the annual rent hits $10,710 ($892 per month) or above, the family should prefer to own. Under the 2018 law, this family would prefer to own only when rents hit $12,198 ($1,017 per month). This is a 14 percent increase in the breakeven rent.

A family with $150,000 annual income

This family would itemize under both the 2017 and 2018 laws. The new taxable amount is much larger ($117,954 versus $100,554) because of the cap on the deductibility of state and local taxes and the loss of the personal exemption. But the total tax bill is very similar ($213 higher), as the higher taxable amount is largely offset by the reduction in the tax rates and the increase in the child credit.

There is, however, a big difference in the rent-versus-buy decision. The tax savings from homeownership are much smaller, or $4,536 less savings per year, or $378 less savings per month. This reduction in savings is because of the rise in the standard deduction, the cap on state and local taxes, and the cuts in the marginal tax rates.

Under the 2017 tax code, this family would prefer to own once rents are at $18,090 per year ($1,507 per month) or more. But under the 2018 code, this family would stay renters until rents hit $22,626 per year ($1,885 per month) or more, or a 25 percent increase in the breakeven rent.

A family with $300,000 annual income

Similarly, this family would have a much higher taxable income in 2018 ($254,241 versus $212,008), primarily because of the cap on the deductibility of state and local taxes and secondarily because of the loss of the personal exemption. The family pays somewhat more in taxes ($1,343) because the reduction in the marginal tax rates and the benefit from the child tax credit do not completely offset the effect of the higher taxable income. (The family income is too high under the 2017 code to qualify for the child tax credit, but it is not too high under the 2018 code.)

But the savings from homeownership is slashed dramatically—by $10,484 per year, or $874 per month. Under the 2017 tax code, the family would choose to own once rents hit $33,086 per year ($2,757 per month) or more. The breakeven point in 2018, however, will now be at $43,570 per year ($3,631 per month), a 32 percent increase.

Do we expect people not to buy because of these changes? At the margin, yes. But because homeownership is generally more affordable than renting, and there are other benefits to homeownership (stability, an inflation hedge, more and different choices in size and location of houses), the impact on homeownership rates will likely be small.

Nevertheless, the effect of these changes may increase, possibly resulting in a slightly lower homeownership rate as more households choose to rent.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.