Photo by Scott Varley/Digital First Media/Torrance Daily Breeze via Getty Images.

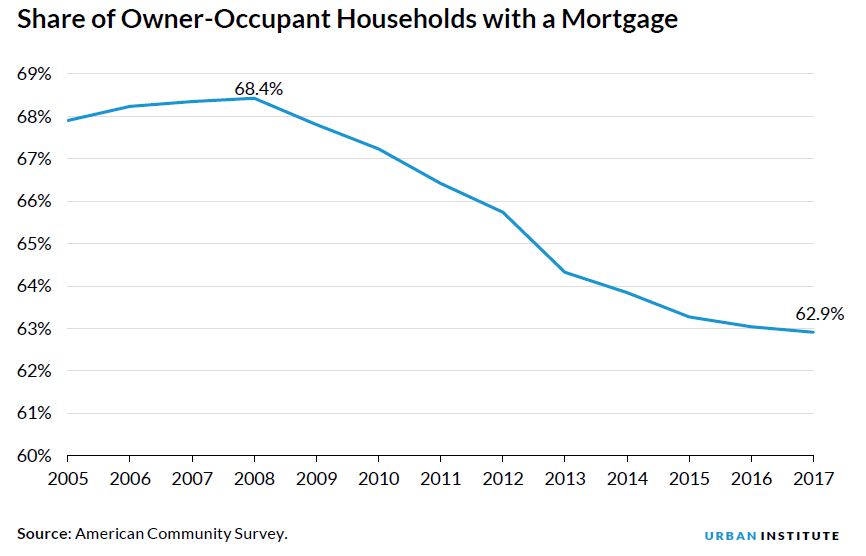

The household-owned value of the US housing market is at an all-time high of $26.12 trillion—significantly higher than the pre-crisis peak of $22.68 trillion in 2006. Housing equity and non-HELOC (home equity line of credit) mortgage debt outstanding are also at historic highs. At the same time, the share of homeowners with a mortgage, at 62.9 percent, is at the lowest level since at least 2005.

Why has this happened? What happens next? And what does it all mean?

That $26.12 trillion in total housing value is composed of two elements: $10.36 trillion in outstanding mortgage debt (including home equity lines of credit) and $15.76 trillion in home equity (the difference between household-owned real estate and mortgage debt).

Though outstanding mortgage debt has expanded in recent years, the faster and stronger recovery in aggregate home values has lowered the mortgage debt–to–home value ratio (for residential real estate) from a peak of 63.3 percent in 2009 to 39.6 percent in the first quarter of 2019.

In contrast, housing equity as a share of aggregate home values has grown from 36.7 percent to 60.4 percent over this same period.

What explains the lower mortgage debt relative to real estate values? First, home equity lines of credit are less prevalent than in years past. The volume of home equity lines of credit fell from $714 billion in 2009 to $399 billion in the second quarter of 2019, according to the Federal Reserve Bank of New York.

Although the outstanding amount of mortgages excluding home equity lines of credit surpassed its pre-recession peak in the second quarter of 2019, relative to home values, it sat at approximately 35.4 percent in the first quarter of 2019, well below its 2009 high of an estimated 54.7 percent.

Another key reason is that a declining proportion of homeowners have a mortgage. The share of homeowners with a mortgage declined steadily between 2008 and 2017, from 68.4 to 62.9 percent—the lowest level since at least 2005. Conversely, the share of owner-occupied households with no mortgage has climbed to 37.1 percent over the same nine-year period.

Why this happened:

An aging population, tighter credit, and more cash sales have resulted in fewer mortgages.

The shifting composition of owner-occupied households with and without a mortgage owes to several reasons, including the surge in all-cash sales in the years immediately following the recession, households’ focus on debt reduction, and mortgage credit conditions that remain tight.

This shift also reflects intergenerational dynamics. Older households are much more likely than younger households to have paid off their mortgage. Though the share of elderly people with a mortgage has increased gradually over time (figure 2), to 38 percent in 2017 for those ages 65 and older, this share is well below 80 percent for those ages 35 to 54.

As baby boomers age, the number of owner-occupied households without a mortgage is increasing.

What happens next:

Shifting demographic and economic forces will shape the market.

Whether the share of owner-occupied households with a mortgage continues to decrease will depend on the interplay between the following factors:

-

the pace at which young, first-time homebuyers purchase homes (which depends on the other items in this list)

-

housing affordability

-

credit availability

-

the strength of the economy including the job market

To a lesser extent, it will also depend on how many elderly households have a mortgage.

What it all means:

Younger borrowers become more important.

As the baby boomer generation ages, younger households will become more important to lenders. If new and younger purchasers increasingly use cash instead of mortgages to buy their homes, competition among lenders will increase, which, in turn, may help ease the restrictive credit standards in place today.

However, the potential relief from still-tight credit standards may have a small impact on homeownership given the limited supply of inventory for sale in much of country.

In addition, the reduced share of homeowners with a mortgage further proves that a shrinking portion of this group is cost burdened. By increasingly paying off their mortgages and converting their entire home value into equity, existing homeowners create a cushion for emergencies and retirement. However, the growth in the share of homeowners ages 65 and older with a mortgage bears watching as it may represent an emerging risk to the mortgage market.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.