<p>Photo by Sawaya Photography/Getty Images.</p>

Traditionally, most homebuyers obtained mortgages from a regulated bank. But the market turbulence of the past decade has spurred a significant restructuring of the mortgage finance industry, thrusting nonbanks—institutions that provide some banking services but are not regulated banks—into a dominant position as mortgage originators.

We’ve added 10 new charts to our monthly chartbook that focus on nonbank mortgage originations, showing the increased reliance on nonbanks by type of mortgage and channel and how nonbanks are helping open the credit box in the agency and government loans market. As nonbanks become a more important part of the evolving mortgage industry, here are five things policymakers should keep in mind:

1. Nonbank originations have surged past bank originations.

Banks used to be the biggest players in the origination space, originating 70 percent of new mortgages in 2013. By 2017, however, nonbanks and banks had nearly flipped, with nonbanks originating 60 percent of new mortgages. The change has been most dramatic for Ginnie Mae loans, with nonbanks originating 36 percent of new mortgages in 2013 and 76 percent in 2017.

2. Nonbanks are even more dominant in the refinance space.

In 2017, 58 percent of purchase mortgages were originated by nonbanks compared with 63 percent of refinance mortgages. For Ginnie Mae loans, 72 percent of purchase mortgages were originated by nonbanks versus 85 percent of refinances.

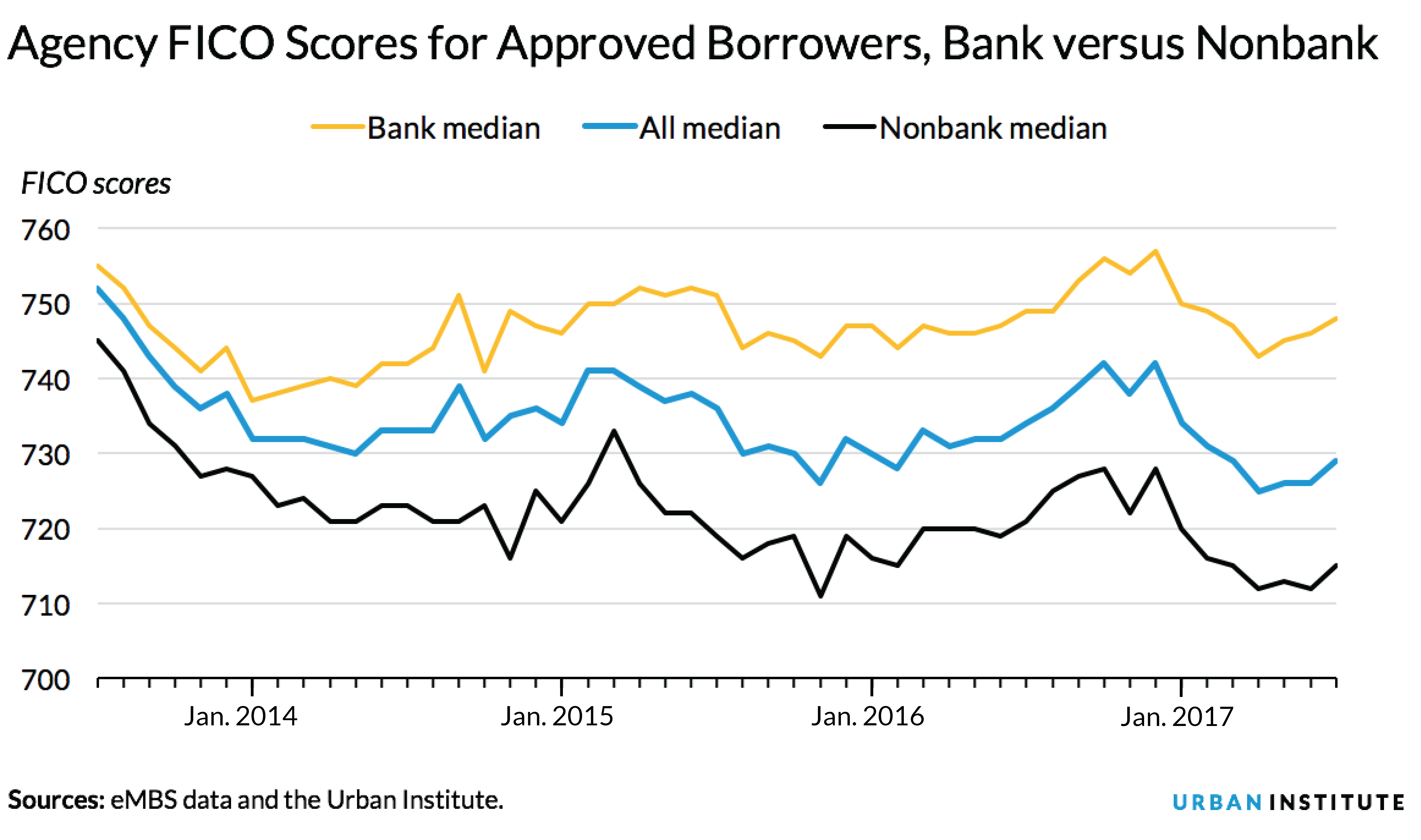

3. Nonbanks are helping borrowers with less-than-pristine credit refinance their mortgages.

The median FICO score for nonbank originations has consistently been less than the median FICO score for bank originations for all three agencies. The nonbank median FICO score has declined 30 points (from 745 to 715) since early 2013, compared with just a 7-point drop (from 755 to 748) in the bank median FICO score. The median FICO score for all agency originations has dropped 23 points from 752 to 729, largely because of nonbank FICO score relaxation. But nearly all the FICO relaxation has occurred in the refinance market, with purchase originations seeing little to no FICO relaxation. Although it has become easier to qualify for a refinance mortgage to reduce monthly payments, obtaining a new mortgage remains difficult.

4. Increased reliance on nonbanks may pose increased risk to the government-sponsored enterprises (GSEs) and the Federal Housing Administration (FHA).

Nonbanks are not as stringently regulated as banks, which may pose greater counterparty risk to the agencies, particularly Ginnie Mae. In addition, many nonbanks taking up the market share left behind by larger banks are thinly capitalized, raising the concern that they may be more open to taking risk.

5. The nonbank surge is a direct result of banks’ wariness to lend.

Banks have pulled back from GSE and FHA lending for three main reasons:

- Lack of clarity about when lenders might be forced to buy back a loan from an investor, and related reputational and litigation risk

- The high cost of servicing delinquent loans

- The uncertain litigation risk from overly aggressive enforcement of the False Claim Act (for Ginnie Mae loans only)

If regulators can address these concerns, banks may be willing to originate mortgages again. Significant progress has been made in this regard, but the FHA has lagged behind the GSEs and their regulator, the Federal Housing Finance Agency, in its efforts to reduce lender uncertainty.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.